Breakdown of 2023 AEP Findings Report

Menu

1. General Overview

1.1 Market Overview

1.2 Submarket Overview

1.3 MA Only/MAPD Overview

2. Plan Type Overview

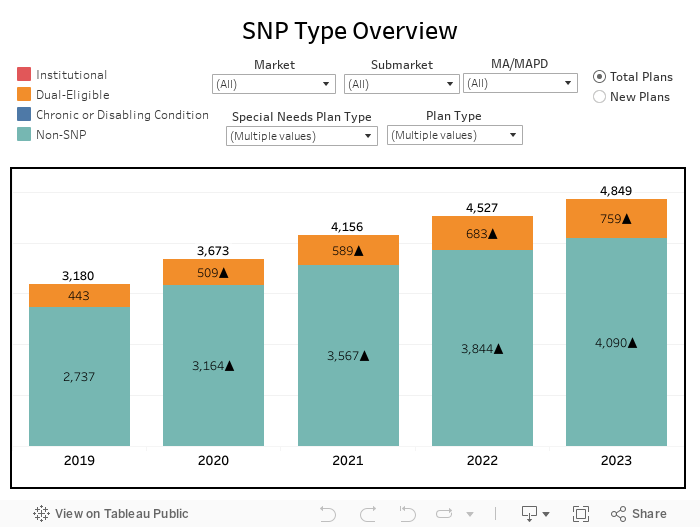

2.1 SNP Type Overview

2.2 Plan Type Overview

3. Premium and Cost Factors

3.1 Premium

3.2 HMO and PPO Deep Dive

3.3 Zero ($0) Premium Expansion

3.4 Drug Deductible

3.5 In Network MOOP

3.6 Part B Give-Back

4. Benefits Overview

4.1 Supplemental Benefits

4.2 Enhanced Benefits

In accordance with the 2023 landscape and plan benefit package (PBP) data released by the CMS in October 2022, this study emphasizes the trends and patterns observed in the various markets and submarkets of CVS Health year-over-year (YoY). The analysis has been segmented into multiple sections, with a note provided in each which details the data included for analysis, including Plan types (Local HMO, Local PPO, Regional PPO, MSA, MMP, Cost, and PFFS), Special Needs Plan type (Non-SNP, D-SNP, I-SNP, and C-SNP), and MA Only/MAPD. Following that, in the visualization – necessary filters are provided to view the data with additional granularity.

1. General Overview

The top markets in terms of both total and new plans are Florida, Great Lakes, South Central, California, and the Gulf States/Georgia. Among these, only California and the Gulf States saw an increase in new plans in 2023 compared to the previous year, at 44.6% and 35.2%, respectively, while the other three markets exhibited a contrast pattern by having a lesser number of plans. MAPD plans grew by 299, a 6.4% YoY increase, while MA Only plans increased by only 39. At the national level, 5,748 plans have been introduced into the Medicare Advantage (MA) market, while CVS Health alone accounts for 10.8% (621) of the total plans and 11% of new plans (97) in 2023.

Note: 1.1 and 1.2 sections include all the SNP types (Non-SNP, D-SNP, I-SNP, and C-SNP), all Plan types (Local HMO, Local PPO, Regional PPO, MSA, MMP, Cost, and PFFS), and MA Only and MAPD plans.

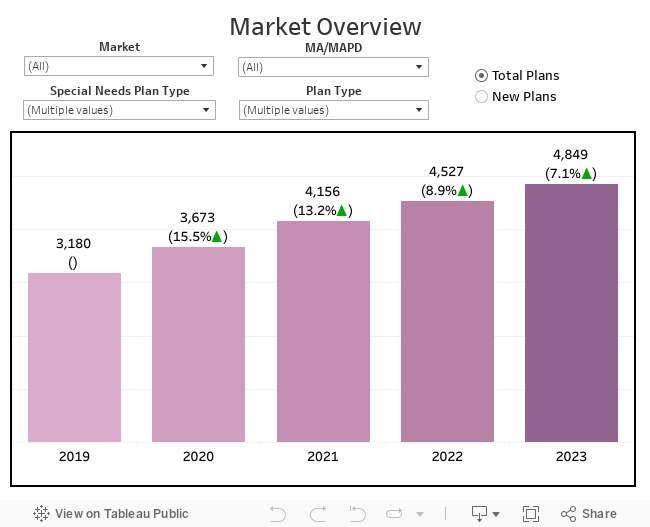

1.1 Market Overview

Great Lakes market has the second position in total plans after Florida, while for new plans it occupies the fifth position.

The total number of plans available in the CVS Health market accounts for about 5,456 with a 6.6 % YoY increase, while overall, there are 5,748 unique total plans and 881 new plans in the country. Although there was a reduction in the introduction of new plans during 2022 (779), an addition of 60 plans will bring the total number of new plans to 839 by 2023. All the markets witnessed a rise in total plans during 2023 except Minnesota and Northwest. However, in contrast to this, the Ohio market saw a drop in total plans last year, but it has increased this year to 304 total plans. Even in terms of new plans, the Northwest market has observed a declining trend since 2020, with only 20 new plans introduced in 2023.

South Central (15.2%), Capitol (13.1%), Keystone (10.8%), Mountain (10.3%), and New Jersey (9.5%) have greater YoY growth for total plans. Northwest has 256 plans against 268 plans in 2022 with a -4.5% decrease, and Minnesota contains 106 total plans, three plans less than 2022 with a -2.8% decrease. The total number of plans remains constant in New York (276) since 2021. The highest YoY increase was noticed in New Jersey, Ohio, Keystone, California, and New York markets for new plans, while there is a reduction among 11 markets. Since 2019, the highest growth for total plans was observed in Mountain (110.5%), South Central (96%), Midlands (88.3%), St. Louis (87.4%), and Arizona (86.9%) markets. The trend from 2020 in new plans has good growth in Keystone (110.7%), Mountain (92.9%), St. Louis (91.7%), New Jersey (46.2%), and Arizona (41.7%).

The following competitors were selected for analysis based on the number of total and new plans in the organization in relation to CVS Health (CVS). They include United Health Group, Inc (UHG), Humana Inc. (Humana), Centene Corporation (Centene), CIGNA, Anthem Inc. (Anthem), and Devoted Health.

At the market level, CVS Health alone accounts for 11.4% of the total plans and 11.6% of new plans in 2023, bagging the third position among other organizations. Gulf States (71), Keystone (56), Great Lakes (48), South Central (48), and Florida (44) have the highest count of total plans for CVS Health while Gulf States (20), California (14), Great Lakes (11), South Central (10), and Northwest (6) are the markets having the highest number of new plans.

UHG occupies the first place with a share of 14.3% (781) of all total plans and 14.9% (125) of all new plans in the market, followed by Humana with 780 total plans and 123 new plans, while Anthem (total plans=400; new plans=28) has the fifth position for total plans after CIGNA (total plans=482; new plans=85).

UHG has more total plans in South Central (92), California (80), and the Great Lakes (75); however, Humana has the highest total plans in Florida (136), Georgia (98), and South Central (83). Similarly, for new plans, California (27), New York (12), and Mid-South (10) markets hold greater numbers for UHG, while Florida (34), South Central (16), and Georgia (11) markets for Humana have the highest new plans.

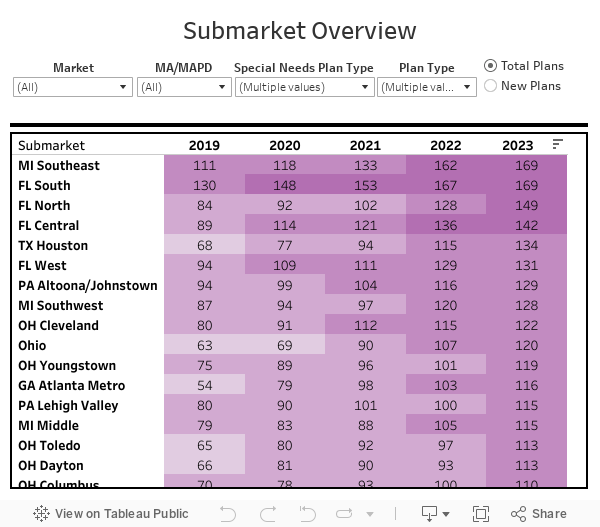

1.2 Submarket Overview

By adding additional plans into the market, GA Atlanta Metro has beaten PA Pittsburgh and PA Altoona/Johnstown, leading in total plans since 2019 (CVS Health specific).

There are 191 submarkets under 19 different markets. Among major shifts, FL South has almost doubled the total plans (107 in 2017 and 212 in 2023) with 98% YoY growth. The average submarket YoY growth for total plans is 13.1% and for new plans is 30.4%. The highest YoY growth was noticed in IL Western (71%), AL Southeast (50%), AL Montgomery Metro (48.9%), AZ Central (40%), and AL Tuscaloosa (40%) while a significant decrease was seen in NY Metro New York (-10.7%), CA Los Angeles (-8.5%), KS Wichita (-7.4%), NY Hudson Valley (-4.8%), WA Puget Sound (-3.2%), MN Minnesota Allina (-2.8%), ME Southern (-2.4%), UT Northern Urban (-2.3%), NH New Hampshire (-2.3%), and IL Chicago (-1.0%).

Multiple submarkets recorded no change in total plans introduced for 2023 in comparison to the previous year, such as KS Topeka (56), CA San Diego (84), ME Northern & Additional Maine (44), MI Upper Peninsula (30), ME Mid Maine (43), and NY Long Island (84).

In 2023, the number of new plans introduced is highest in FL North (34), followed by FL South (27), FL Central (26), OH Cincinnati (26), and GA Atlanta Metro (25). About 33.5% of the submarkets saw a decrease in YoY growth, and more than 9% noticed no introduction of new plans.

Between 2017 and 2022, CVS Health released more total plans in the Pennsylvania submarkets of Pittsburgh and Altoona/Johnstown; however, the GA Atlanta Metro submarket surpassed these two submarkets to take the top spot in 2023 with total plans of 22 and new plans of 12. The plan count in these markets is lower in competitive firms like UHG and Humana. In CVS Health, the introduction of new plans has fluctuated in a downward trend over the years. This is evident from 2020, when the TX Houston submarket introduced the highest number of new plans (8), further in 2021 by NY Metro New York (5), then in 2022 by VA Northern (4), indicating the declining trend. By adding 12 new plans to the submarket GA Atlanta Metro in 2023, the trend of these new plans has shifted in the opposite direction.

In TX Houston, UHG has the greatest total plans with 36 (CVS Health has 13), while Humana has 56 total plans in FL North (CVS Health has 9 plans). Regarding new plans, UHG had nine plans in NY Northern Central Upstate New York, while FL North had fourteen; CVS Health, however, does not have any new plans in these submarkets.

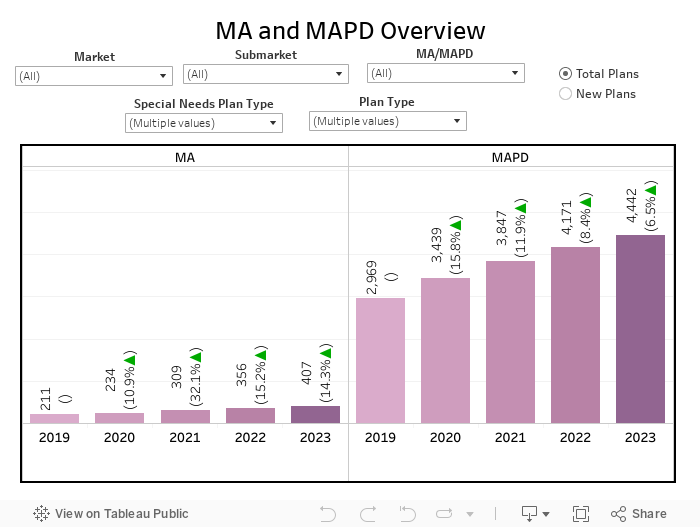

1.3 MA Only/MAPD Overview

2023 will see a more than double the number of MAPD plans from 2017.

Note: Section 1.3 includes all the SNP types (Non-SNP, D-SNP, I-SNP, and C-SNP), all Plan types (Local HMO, Local PPO, Regional PPO, MSA, MMP, Cost, and PFFS). With the mentioned note, MA Only and MAPD plans are discussed briefly.

a) MA Only Section:

Of the total plans in the market, MA Only constitutes 8.5% and has increased by 9.2% annually, accounting for 464 total plans in 2023. There is a slight variation in the number of new MA Only plans, with only a net gain of a single plan. The markets with the highest total MA Only plans are the Great Lakes (61), South Central (59), and Midlands (53). South Central has 18.5% of new MA Only plans, which occupy the first position, followed by Keystone (9) and Midlands (8).

TX Houston submarket bags the number one position for both total (22) and new (5) MA Only Plans. Among the competing organizations, Humana ranks first with a total of 81, followed by UHG (57) and CVS Health (49).

b) MAPD Section:

2023 realized a plan growth of 6.4% YoY with 4,992 total MAPD plans. The absolute number of MAPD plan growth has decreased for the third year in a row (2020 saw a growth of 519 plans; 2021 added 468 plans, and 2022 increased by 393 plans).

Compared to the previous year, the number of new MAPD plans is up 8.3% in 2023 after slowing by 6% last year. Florida (586), the Great Lakes (501), and South Central (478) have held the top three spots for the most total MAPD plans in 2023. However, Florida has 12.7% of new MAPD plans; South Central has 82 new MAPD plans, and California has 79 plans.

Even at the submarket level, Florida submarkets have the most plans, while FL South has the first position with 204 total MAPD plans, while FL North knocks the top place for new MAPD Plans (32). The top three MAPD plan providers among the many competitive firms are UHG (724) which includes 14.5% of the total MAPD plans, followed by Humana (699), and CVS Health (572).

2. Plan Type Overview

Over 77% of all plans available in the market are Non-Special Needs Plans (Non-SNP), followed by Dual Eligible Special Needs Plans (D-SNP) with 13.9%, Chronic Condition Special Needs Plans (C-SNP) with 5.6%, and Institutional Special Needs Plans (I-SNP) with 3.5%. Regarding trends in plan types, HMO and PPO plan counts are still increasing, while the number of plans in Cost, MMP, MSA, and PFFS are gradually decreasing over the years, except Regional PPO, which has plateaued.

2.1 SNP Type Overview

South Central market is leading in Non-SNP MA Only plans, while for Non-SNP MAPD it is bagged by Great Lakes, and D-SNP plans are higher in the Florida market.

From the past four years, there was a net increase in total plans across all categories equaling 4,203 Non-SNP, 759 D-SNP, 304 C-SNP, and 190 I-SNP plans. There were 620 new Non-SNP plans in 2023, D-SNP of 127, C-SNP of 72, and I-SNP of 20.

Note: In the 2.1 section, Non-SNP plans are discussed as subsections with MA Only, and MAPD plans separately, while under D-SNP only MAPD plans are discussed, which includes all Plan Types (Local HMO, Local PPO, Regional PPO, MSA, MMP, Cost, and PFFS).

Non-SNP:

The Non-SNP YoY net growth of only 5.5% is the lowest in six years at an overall level. Non-SNP plans are the only category to exhibit a rise in new plans introduced in 2023 with 620, a growth of 15% over 2022.

Non-SNP MA Only:

All the MA Only plans available in this market belong to the category of Non-SNP type with a total of 464 and 65 new plans. South Central, Keystone, and Midlands markets have a higher number of new MA Only Non-SNP Plans; however, for total plans, Great Lakes has 61 plans, followed by South Central (59) and Midlands (53). Humana (81), UHG (57), and CVS (49) have the greatest number of total MA Only Non-SNP plans, while new plans are from Humana (15), Highmark (8), and CIGNA (8). CVS has the highest count of plans in South Central and Midlands, while the competitors also have more plans in these markets.

Non-SNP MAPD:

About 3,739 total Non-SNP plans belong to the category of MAPD plans, out of which 555 are new plans. Since 2021 there has been a decrease in new plans introduced in this category, while in 2023, the upward trend is seen with 16.8% YoY growth. Since 2020, Great Lakes, Florida, and California have been leading in the Market with the highest count of plans. In 2018, Keystone had the second highest total Non-SNP plans after Great Lakes. However, the position has been overtaken by other markets over the years, and the Keystone market fell to seventh place in 2023. South Central (64), California (62), and Florida (52) are on the top list for having greater new MAPD Non-SNP plans. Northwest (-8.2%) and Heartland (-0.8%) markets show a YoY decline trend for total MAPD Non-SNP plans, while South Central has 344 plans with the highest YoY gain of 13.5%.

CVS provides the highest total number of MAPD Non-SNP plans in Keystone (47), Georgia (47), and Great Lakes (44), while new plans are from California (12), Great Lakes (11), and Georgia (10). Compared to CVS, UHG has a lesser count of total plans in both the Keystone (25) and Georgia (21) markets while having higher plans in Great Lakes (48). However, Humana noticed lesser plans in Keystone (29) compared to CVS and had more plans in Georgia (67) and Great Lakes (55). Both Humana and UHG have lesser plans in the markets where CVS has a higher introduction of new plans, except UHG in the California market had 20 new MAPD Non-SNP plans.

D-SNP:

There are no MA Only stand-alone plans in other SNP types. Hence all the discussed facts are regarding the MAPD plans. The total number of D-SNP plans has doubled since 2018, with an 11.1% rise in 2023. D-SNP saw a slight decrease in the number of new plans introduced from 135 (2022) to 127 (2023), a drop of 5.9%.

Florida has the highest number of total D-SNP plans, which is less than the previous year (110 in 2023, 119 in 2022), followed by Georgia with 99 total D-SNP plans, and it also has included 26 new D-SNP plans into the market with 73.3% YoY growth. While most markets witnessed a downward shift in introducing new D-SNP plans, the YoY trend reduction for total D-SNP plans was observed in Florida, Arizona, and New York markets. D-SNP new plans have not been included in New Jersey since 2022.

CVS occupies the fifth position in having total D-SNP plans with a share of 10.1% among other competitors, while concerning new D-SNP plans; it stands in the second position with 17 plans added into the market in 2023. The number one place is taken by UHG (16.9%) with 128 total and 37 new D-SNP plans, followed by Centene (13.6%), Humana (13%), and Anthem (10.8%). In 2019, there were 19 plans introduced by CVS; over the years, it has increased four times and accounts for a total of 77 plans this year. In CVS, Georgia had 10 plans in 2022, surpassing Florida (16) this year by introducing 19 total and 9 new D-SNP plans to bag the top position. In the Georgia market, the competitors have lesser plans than CVS, that is Humana (18), UHG (15), Centene (16), and Anthem (6). UHG has the highest total D-SNP plans in South Central (20) and Centene in Georgia markets; however, Ohio has higher new D-SNP plans introduced in the competitor’s market.

Sub-Market Highlights:

| Total Plans | ||||

|---|---|---|---|---|

| Special Plan Type | Submarket | No. of plans | Submarket | YoY growth (%) |

| Non-SNP (MA Only) | TX Houston | 22 | CA North Bay | 300 |

| IL Northern | 20 | WA Inland Empire | 83.3 | |

| MN Minnesota Allina | 19 | CA Bay Area | 66.7 | |

| Non-SNP (MAPD) | MI Southeast | 145 | IL Western | 70.8 |

| FL South | 114 | TX Panhandle | 68.8 | |

| MI Southwest | 109 | AZ Central | 55.3 | |

| D-SNP | FL South | 49 | CA San Diego | 200 |

| NY Metro New York | 37 | OK Tulsa | 125 | |

| FL North | 36 | OK Tulsa | 120 | |

| New Plans | ||||

|---|---|---|---|---|

| Special Plan Type | Submarket | No. of plans | Submarket | YoY growth (%) |

| Non-SNP (MA Only) | TX Dallas/Fort Worth | 5 | PA Altoona/Johnstown | 300 |

| TX Houston | 5 | SD Sioux Falls | 300 | |

| IL Eastern | 4 | OK Oklahoma City | 200 | |

| Non-SNP (MAPD) | OH Cincinnati | 16 | TN Cookeville | 1,000 |

| PA Lehigh Valley | 16 | TX Panhandle | 900 | |

| GA Atlanta Metro | 16 | AR Arkansas | 800 | |

| D-SNP | OH Cleveland | 8 | OH Cincinnati | 700 |

| OH Akron-Canton | 8 | OH Dayton | 700 | |

| OH Cincinnati | 8 | LA Baton Rouge | 600 | |

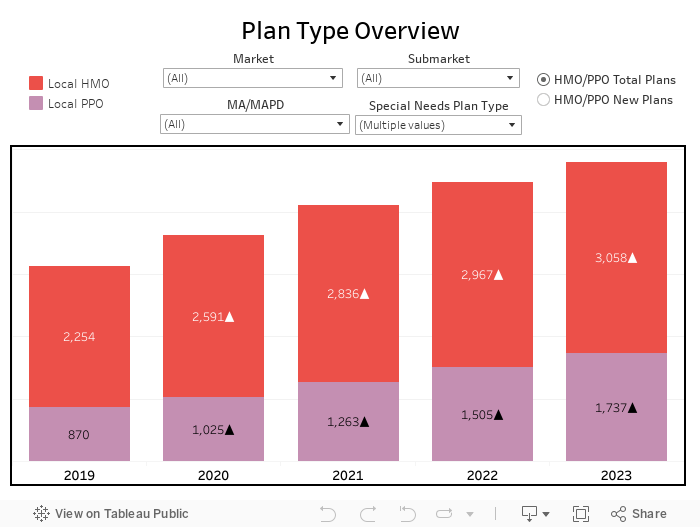

2.2 Plan Type Overview

Total plans have increased in Local HMO and Local PPO with 3,466 and 1,817, respectively, while in other plan types like Cost (51), MMP (27), MSA (3), PFFS (32), and Regional PPO (60) indicating a downward trend. In 2023, 460 new HMO plans, 377 PPO plans, one Regional PPO, and one cost plan will be available in the market.

The total number of D-SNP PPO plans in 2020 is more than 4X in 2023.

Note: In the 2.2 section, Non-SNP plans are discussed as subsections with MA Only and MAPD plans separately, while under D-SNP only MAPD plans are discussed, which includes Plan Types (Local HMO, Local PPO, and Regional PPO).

Non-SNP HMO:

The total number of plans accounts for 2,412, with a YoY growth of 2.5%. However, the new plans in this category are up by 20.9%, with plans increasing by 301 in 2023 against 249 in 2022.

- MA Only: There are 200 MA Only plans present under Non-SNP and HMO plan types, with 17 new plans. Over the years, Great Lakes had a higher number of plans, while South Central overtook Great Lakes in 2023 with 28 total and 5 new plans. CVS stands in 4th position with 14 total plans and no new plans in 2023.

- MAPD: Out of the total Non-SNP HMO plans, 91.7% belong to the MAPD category, with 284 new plans in 2023 and less than 364 plans in 2020. Florida (290), California (286), and Great Lakes (217) have greater counts of MAPD plans under the Non-SNP HMO type, and for new plans, California has the highest with 47 plans. Under this plan type, UHG (262), Humana (254), and Centene (222) are the major competitors for CVS, with 214 total plans. However, Devoted Health provides 34 new plans, followed by CVS with 32 new plans. CVS has the most total plans in the Keystone (26) and California (24) markets and has greater plans than Humana and Centene.

Non-SNP PPO:

About 1,626 total plans with about 13.1% YoY rise were seen in Non-SNP PPO plans, and the addition of new plans 317 is greater than new plans added under the PPO plan type.

- MA Only: Since 2019, the number of plans has increased 3.5 times to 188 total MA Only Non-SNP PPO plans in 2023, compared to 53 in 2019. The new plans under this type in 2021 were 46, but in 2022 it dropped to 37, while in 2023 there are 47 plans. South Central has a greater count of plans with a total of 21 and Keystone is the highest for new plans with 8. Humana (43), CVS (35), and UHG (27) are competing in introducing the MA Only Non-SNP PPO plans. Humana has 10 new plans and bags top position, while CVS in the third position has 6 new plans. CVS provides the highest number of plans in the South Central (8) market, which is higher than its competitor in the same market. Humana’s plans are introduced more in the Midlands, and for UHG, it is the Great Lakes. Humana and Highmark Health introduce more new plans in Midlands and Keystone, respectively.

- MAPD: There are 1,438 total MAPD Non-SNP PPO plans, with 270 new plans up by 9.8%. Great Lakes and South Central markets have a higher number of total plans 186 and 154, respectively, while new plans are higher in South Central (37) and Keystone (33). CVS bags number one position in offering these plans with 274, followed by Humana (252) and UHG (197). Humana (52) provides more new plans than CVS (41). Georgia is the market having a higher total (41) and new plans (10) in CVS. When compared to competitors, the count of plans is greater in CVS.

Non-SNP Regional PPO:

MA Only: Regional PPO plans are reached stagnant from 2021. The total plans under MA Only Non-SNP Regional PPO are 19. Mid-South market has 5 total under this category, the most of any market.

MAPD: There are 33 MAPD plans under Non-SNP Regional PPO, and has only one new plan in 2023. Ohio, with 6 total plans depicted as the top market, Mid-South and Georgia have one new plan in each market. CVS Health has had three MAPD Non-SNP Regional PPO plans since 2019, while Humana has 17 plans and UHG has 10 plans.

D-SNP HMO:

From 2020, D-SNP HMO plans have shown an upward trend with 34.6% YoY growth and with a total of 646 plans in 2023. There is a decrease in the number of new plans introduced compared to 2021 (103) and 2022 (108), while in 2023, under this plan type, 86 plans account for a drop of 20.4% over 2022. Most of the total and new HMO plans with Dual Eligible type are from the Florida market (104 & 20) but less than the previous year, followed by Georgia (77 & 16) and South Central (72 & 9). UHG, Centene, Anthem, and CVS have most of the total D-SNP HMO plans. Similarly, new plans come from UHG, CIGNA, and CVS. CVS was a leading organization with the highest number of new plans in 2020 and 2022, but in 2023 it stands in the third position with 12 new plans and has 72 total plans. In CVS, the Georgia market surpasses Florida to take the lead in the number of D-SNP HMO plans in 2023, and it observed that the number of plans in other competitors is less than CVS in the Georgia market.

D-SNP PPO:

The D-SNP PPO total plans were only 24 during 2020, which will drastically rise to 111 in 2023, with 41 new D-SNP PPO plans being introduced. Georgia, with 22 total and 10 new D-SNP PPO Plans bags first place among other markets. CVS has D-SNP PPO plans from 2023, only one plan in the Midlands market and four plans in Georgia. UHG (6) and Humana (7) has the highest total plans in the Georgia market.

Submarkets Highlights: The top three submarkets under all the SNP types with HMO and PPO plans are tabulated below:

| Total Plans | ||||

|---|---|---|---|---|

| Special Plan Type | Submarket (HMO) | No. of plans | Submarket (PPO) | No. of plans |

| Non-SNP (MA Only) | TX Houston | 13 | WI Central | 9 |

| PA Southeastern | 11 | WI Southeast | 8 | |

| TX San Antonio | 8 | WI Northeast | 8 | |

| Non-SNP (MAPD) | FL South | 93 | MI Southeast | 66 |

| MI Southeast | 72 | PA Altoona/Johnstown | 60 | |

| FL North | 72 | PA Lehigh Valley | 56 | |

| D-SNP | FL South | 45 | GA Atlanta Metro | 10 |

| NY Metro New York | 34 | GA Savannah | 8 | |

| NY Long Island | 32 | GA Augusta | 8 | |

| New Plans | ||||

|---|---|---|---|---|

| Special Plan Type | Submarket (HMO) | No. of plans | Submarket (PPO) | No. of plans |

| Non-SNP (MA Only) | TX Houston | 2 | PA Altoona/Johnstown | 4 |

| TX Dallas/Fort Worth | 2 | IL Eastern | 4 | |

| FL North | 2 | WI Southeast | 3 | |

| Non-SNP (MAPD) | CA Bay Area | 12 | PA Lehigh Valley | 13 |

| OH Cincinnati | 11 | GA Atlanta Metro | 12 | |

| FL South | 11 | NJ South | 11 | |

| D-SNP | OH Youngstown | 6 | OK Tulsa | 3 |

| OH Dayton | 6 | OK Rural | 3 | |

| OH Cleveland | 6 | OK Oklahoma City | 3 | |

3. Premium And Cost Factors

Note: In the 3rd section, Non-SNP plans are discussed with MA Only and MAPD plans separately, while under D-SNP, only MAPD plans are discussed, which includes Plan Types (Local HMO, Local PPO, and Regional PPO).

The data in the premium and cost factor section briefs about the average YoY and maximum yearly change in premium, drug deductible, and In-Network MOOP. All this has been done while comparing the performance of CVS Health versus that of the others in their markets.

The national average for the premium has been decreasing YoY, with the 2023 average premium being $23.3. However, Florida ($8.4) and Mountain ($8.9) markets have the lowest average premium, while Minnesota has the highest ($49.7). The average premium of the plans in Heartland ($10.3) and Midlands ($10.5) are also quite low.

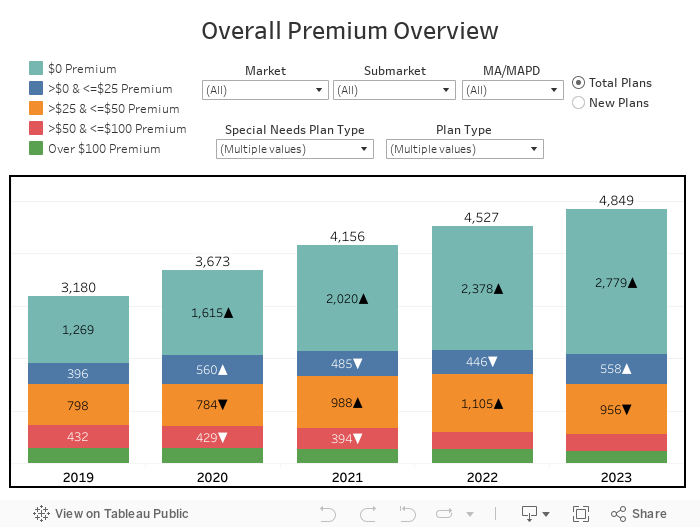

About 67.7% (2,771 total) of the Non-SNP plans in 2023 are $0 premiums which have been increased from 2022 by 61.7% (2,372 total). CVS Health has managed to provide 404 plans out of these 2,771, forming about 75% of CVS Health’s total plans. In D-SNP, a large part of the plans is from $0-$25 and $25-$50 premium segments. While the average deductibles for D-SNP types increased over time, those for Non-SNP types decreased. The average deductible for Non-SNP plans has gone down to $124 in 2023 compared to $138 in 2022. The Maximum Out-Of-Pocket (MOOP) fluctuates every year, which has increased from $5,660 in 2022 while it is $6,010 in 2023.

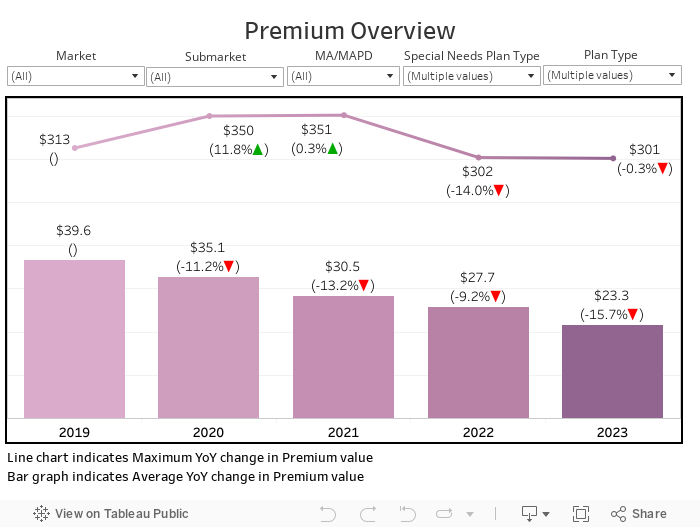

3.1 Premium

Average premiums have gone down from $27.7 to $23.3

The increase in $0 plans has led to the fall of the average premium over consecutive years, with the YoY decrease in the premium being around 15.7%. The Non-SNP MAPD plans have an average premium of $26.2, while Non-SNP MA Only has a premium of $1.9 in 2023. The average D-SNP premium has slightly increased from 2021 ($29.3), with an average premium of $31.1 in 2022 and a slight drop of 30.7 in 2023. There hasn’t been much change in the maximum premium value for Non-SNP MAPD plans, as they have dropped from $302 to $301. For D-SNP, the maximum premium increased from $117 in 2022 to $125 in 2023.

The average Non-SNP MAPD premium is $18, while the maximum is $198 for CVS Health. While for other competitors, the average premium is $10 for Centene, $16 for UHG, $19 for Anthem, and $28 for Humana. The D-SNP MAPD plans have an average premium of $20, while the maximum is $37. However, it is $22 for CIGNA, $27 for Centene, $28 for Anthem, and $34 for UHG and Humana.

The average monthly premiums of Non-SNP MAPD are $12 for HMO plans and $15 for PPO plans for CVS Health. The maximums are $187 for HMO and PPO for the same organization. The D-SNP MAPD monthly average premium comes to $21 for HMOs and $19 for PPOs, while the maximum is $37 for HMOs and $20 for PPOs.

| Plan Type | Premium | $0 Premium Plans | ||

|---|---|---|---|---|

| Average ($) | Maximum ($) | Total Plans | New Plans | |

| Non-SNP MA Only HMO | 5.3 | 199 | 164 | 17 |

| Non-SNP MAPD HMO | 20.6 | 296 | 1,554 | 235 |

| Non-SNP MA Only PPO | 0.7 | 177 | 182 | 47 |

| Non-SNP MAPD PPO | 26.2 | 301 | 850 | 199 |

| D-SNP PPO | 32.4 | 43 | - | - |

| D-SNP HMO | 30.1 | 125 | 8 | - |

| Non-SNP MAPD RPPO | 67.6 | 198 | 2 | 1 |

| Non-SNP MA Only RPPO | 0 | 0 | 19 | - |

| D-SNP RPPO | 27.7 | 36 | - | - |

The non-SNP category has a higher percentage of plans with a $0 premium (67%), while the D-SNP has a larger number of plans with premium ranging from $25 to $50.

There is an increase of 335 (16% from 2022) plans in the total Non-SNP MAPD category for the $0 premium plans in 2023. For Non-SNP MA Only, 64 plans have a $0 plan, and the total count is 365. Apart from the $0 plans, only the less than $25 premium plans have shown an increase in total Non-SNP MAPD count, with all the other plans showing a decrease, while Non-SNP MA Only plans saw an increase only in $0 premium plans. Florida has the highest number of $0 plans in the Non-SNP MAPD category (344 plans), South Central has the highest number of $0 plans in the Non-SNP MA Only (48 plans) category. FL South, FL North, FL Central, and FL West submarkets have the highest number of $0 premium plans in the Non-SNP MAPD category, while TX Houston has a higher count for MA Only Non-SNP plans.

In the new plans, there is a decrease in the $25-$50 and greater than $100 categories in the Non-SNP MAPD category. Out of total Non-SNP MAPD plans with a $0 premium, 18% are formed by new plans. In Non-SNP MA Only, there are only $0 premium plans with a rise of 7 plans total, coming to 64 plans. South Central has the highest number of new plans in the Non-SNP MA Only and MAPD categories in the $0 category. FL North has a higher number of new plans for Non-SNP MAPD plans, while for MA Only plans, it is the TX Houston submarket.

D-SNP plans premium segment ranges from $0-$50, where there are 510 total plans belonging to the $25-$50 section, which is less compared to the previous year (535), and there are 240 plans in $0-$25 premium section which saw a rise. The highest number of total plans in the $25-$50 section can be seen in Florida (80) and Georgia (68) in the D-SNP category. South Central market had 45 total D-SNP plans in 2022, which saw a major decrease in plans accounting for 12 in 2023. While talking about the new plans in this category, there is an increase in the $0-$25 premium section and a decrease in the $25-$50 section.

In Non-SNP MAPD, CVS Health ranks number one in the introduction of $0 premium plans with 355 total plans, followed by 339 for Humana and 295 for UHG. In the Non-SNP MA Only plan type, CVS Health (49 plans), Humana (75 plans), and UHG (56 plans) are leading the race. Humana bags first in introducing the new plans for both MA Only and MAPD Non-SNP plans, however, CVS Health stands in the third position by introducing 52 new Non-SNP MAPD plans in 2023, and there are six new MA Only Non-SNP $0 premium plans. In CVS Health, the South Central market has the highest total Non-SNP MA Only, and Georgia has a greater count for Non-SNP MAPD plans. While for new Non-SNP MAPD plans, California had the highest, and for Non-SNP MA Only, it is South Central.

For both total and new D-SNP plans, CVS Health ranks number one in the $0-$25 premium section (63 total plans and 17 new plans), followed by Centene (56 plans). In the $25-$50 plans, UHG has 108 total plans and 34 new plans, while CVS has only 14 plans and ranks seventh in the entire nation.

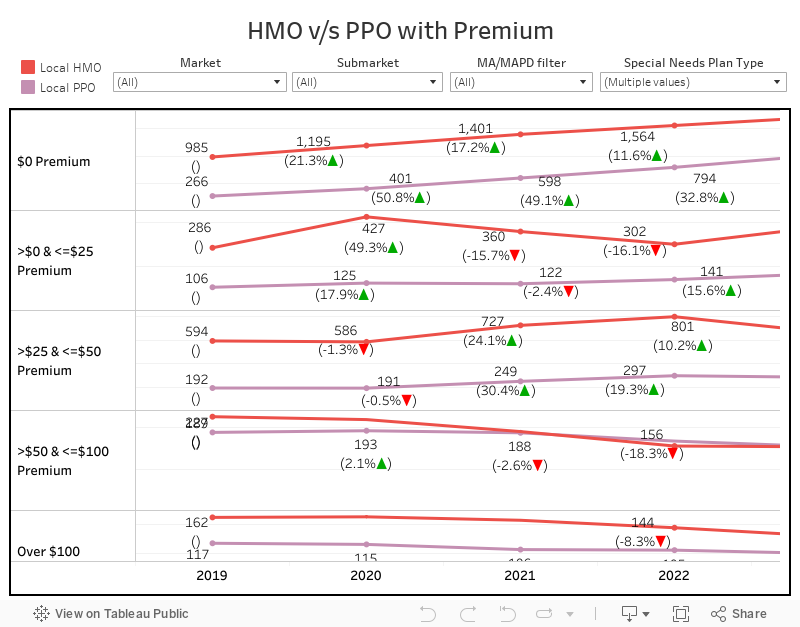

3.2 HMO and PPO Deep Dive

The rise in HMO and PPO plans was seen in the $0 and $0-$25 sections.

The total number of Local HMO and Local PPO plans have seen an increase of 2.5% and 11%, respectively, but this is primarily in the $0 segment, as the other segments have shown a decrease in the trends of the Non-SNP MAPD category. The $0 plan has grown by 10% in HMO and 29% in PPO in the Non-SNP MAPD category and also noticed an increase in the $0 to $25 section, but saw a decrease for the other premium plans. The greater than $25 but less than $50 has the largest drop in plans for both HMO and PPO, with a 26% drop in HMO (226) and a 20% drop in PPO (196) in Non-SNP MAPD. For Non-SNP MA Only, the number of plans rose to 200 (2.6%) for HMO but by 32% for PPO. This was again due to the $0 plans, which rose by 11.6% in the case of HMO and about 34.8% in the case of PPO. Florida (270) and California (203) have the highest number of plans for the Non-SNP MAPD $0 premium section with HMO plan type, while for PPO, it is South Central (114) and Georgia (95). The South Central market has higher plans for MA Only Non-SNP HMO and PPO plans in the $0 premium category.

For D-SNP MAPD, the number of HMO plans rose to 646 (5.4%), and the number of PPO plans rose to 111 (65.6%) increase. For HMO, the rise is primarily due to the $0-$25 plans, which have gone up by about 70% to 214, but for PPO, this rise is due to the number of plans in both $0-$25 and $25-50 segments.

Further, in the Non-SNP MAPD category, the HMO plans by CVS Health have increased only in the $0 and >$25-$100 plans. However, PPO increased from $0 to $25 and $50 to $100. All the remaining sections show a gradual decrease, and the same observation can be noticed for all the other companies as well.

3.3 Zero ($0) Premium Expansion

In 2023 there is a presence of $0 premium plans in all the CVS Health markets.

In 2023, $0 premium plans will be available in all counties where the CVS Health market is operating, including $0 premium plans for the first time in a few counties. Four counties make up the California market under the CA Bay Area submarket; all the counties had $0 premium plans in 2022, apart from Santa Cruz, which received $0 premium plans for the first time in 2023. Similarly, the Midlands market under IA Council Bluffs submarket County Taylor and Richardson County in NE Nebraska submarket saw the introduction of $0 premium plans in 2023.

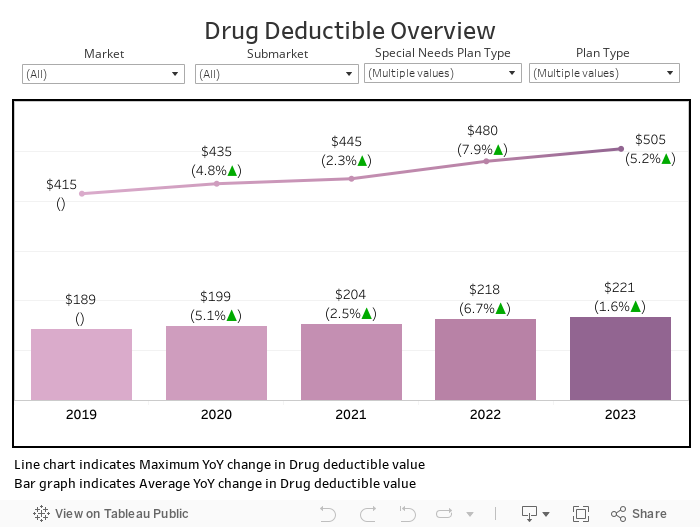

3.4 Drug Deductible

The average Drug deductible was higher in D-SNP plans than in Non-SNP plans

The average and maximum drug deductible continue to vary nationally from past years. This increase could be due to the rise in inflation, and the cost of medicines may go up further as the year progresses. The overall average drug deductible for Non-SNP MAPD plans was found to decrease to $124 from $138 from the previous year, while for D-SNP plans, the average deductible is increasing YoY by $502 in 2023. Almost in all the categories, the maximum drug deductible was $505. New Jersey market has the highest average drug deductible of $247 for Non-SNP MAPD plans, while Keystone had least by $48. However, for D-SNP plans, New Jersey had a higher average of $505, and the least was noticed in the Northwest ($458).

In Non-SNP MAPD, the average has gone down by $14 to become $124 for all organizations. For CVS Health, this has gone up by $1 to $85, but this has gone down to $70 from $125 for UHG, and for Humana, it is $180. For D-SNP MAPD plans, the average has gone up to $505 from $426 for CVS Health, and the average happens to be the same for UHG and Humana at $505.

| Plan Type | Drug Deductible | $0 Drug deductible plans | ||

|---|---|---|---|---|

| Average ($) | Maximum ($) | Total Plans | New Plans | |

| Non-SNP MAPD HMO | 103 | 505 | 1,660 | 212 |

| Non-SNP MAPD PPO | 125 | 505 | 810 | 143 |

| D-SNP PPO | 501 | 505 | - | - |

| D-SNP HMO | 502 | 505 | 2 | - |

| Non-SNP MAPD RPPO | 275 | 505 | 5 | - |

| D-SNP RPPO | 505 | 505 | - | - |

Out of Non-SNP and D-SNP MAPD plans about 56% belong to the $0 drug deductible range..

The total number of plans is rising only in the $0 drug deductible section, and the new plans have been increased in $0 and >$100 deductible segments. Non-SNP MAPD total plans with $0 drug deductibles have a YoY rise of 22.7%, whereas in 2023 there will be 355 new plans with a YoY growth of 30.5%. Most of the D-SNP plans belong to the >$100 deductible segment, with 757 total plans (11.3% YoY growth) and 127 new plans, which is lesser than in 2022 (134).

Great Lakes has a higher total count with 306 Non-SNP MAPD $0 deductible plans, with California as the lead for new plans (54). For above $100, Non-SNP MAPD plans are high in South Central, with 137 total plans and 29 new plans. For D-SNP plans in >$100, Florida ranks first with 109 total plans, followed by Georgia (99). At the same time, Georgia has the highest number of new plans in D-SNP plans with 26.

For CVS Health, the deductible is present in $0 and from $50 to >$100 segments. In Non-SNP MAPD with $0 deductible, the total plan is 324, and there are 44 new plans, while for >100 deductible, the total plan is 162 with 29 new plans. In the D-SNP category, with a >$100 deductible, there were 77 total plans and 17 new plans.

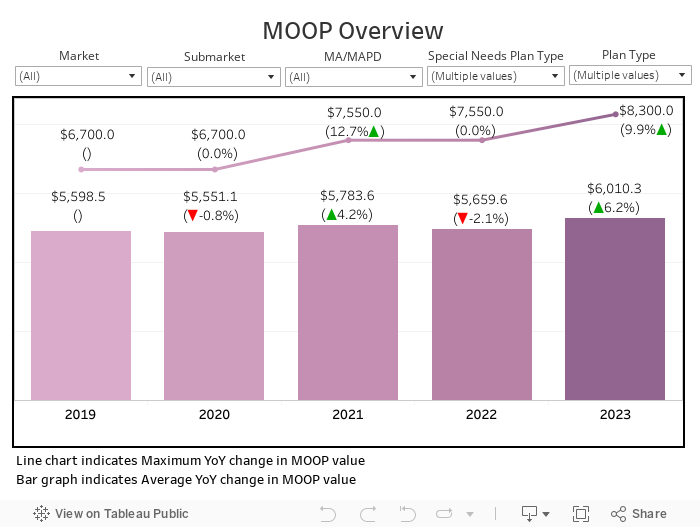

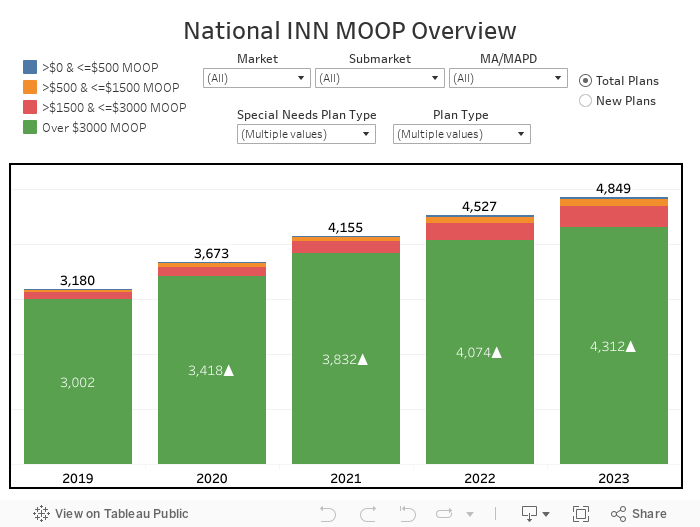

3.5 In-Network Maximum Out-of-Pocket (MOOP)

The D-SNP plans have more average MOOP than Non-SNP plans

The value for the MOOP has been varying consistently over the last 5 years. For Non-SNP MAPD plans, the average MOOP decreased to $5,567.8 from $5,608.5 from the past year, while for Non-SNP MA Only plans, it is $5,499.8. The average MOOP for D-SNP plans increased by 24.5% YoY, from $5,920.7 to $7,667. The average MOOP varied from plan to plan. However, the maximum MOOP did not alter for most of the plans, remaining at $8,300 except for Non-SNP Regional PPO, which was $7,550.

New Jersey market had the highest average drug deductible of $7,514 for MAPD ($6,584 for MA Only), and the least was seen in California ($3,736 -MAPD, $4,496-MA Only) for Non-SNP plans. Capitol had the highest average MOOP of $8,300, and Florida ranks least with $4,261 for D-SNP plans. CVS Health had a $5,953 average and $8,300 maximum MOOP for Non-SNP MAPD plans, while the competitor Humana had an average greater than CVS Health of $6,048. The MOOP has gone down for a second consecutive year for both CVS Health and the others, but this drop is higher in the case of CVS Health ($150) compared to the others ($24). The MOOP value has dropped by a higher margin because the MOOP for CVS Health has previously been a lot higher in the Non-SNP MAPD category. Anthem ($6,533) had a higher average for Non-SNP MA Only plans compared to CVS Health ($5,883), while the maximum for Anthem remains $8,300, but for CVS Health, it is $7,550. In the D-SNP category, Centene ($8,237) is a competitor with a much higher average MOOP than other organizations, and CVS Health ($8,198) with a rise of about 11%.

| Plan Type | MOOP | >$3000 MOOP plans | ||

|---|---|---|---|---|

| Average ($) | Maximum ($) | Total Plans | New Plans | |

| Non-SNP MA Only HMO | 4,999 | 8,300 | 191 | 15 |

| Non-SNP MAPD HMO | 5,154 | 8,300 | 1,783 | 231 |

| Non-SNP MA Only PPO | 5,660 | 8,300 | 186 | 47 |

| Non-SNP MAPD PPO | 5,796 | 8,300 | 1,390 | 259 |

| D-SNP PPO | 8,016 | 8,300 | 111 | 41 |

| D-SNP HMO | 7,550 | 8,300 | 597 | 80 |

| Non-SNP MA Only RPPO | 5,823 | 7,550 | 19 | - |

| Non-SNP MAPD RPPO | 6,771 | 7,550 | 33 | 1 |

| D-SNP RPPO | 8,300 | 8,300 | 2 | - |

About 89% of the plans are having MOOP greater than $3,000

Overall, the market saw that the number of plans is increasing in all the MOOP segments except for $0 to $500. Most of the plans have a MOOP of >$3,000, which is about 89% (4,312 out of 4,849). The Non-SNP MAPD category had risen in all MOOP segments in total plans, but for new plans, there was a rise only in >$3,000 and >$500 to <$1,000. On the other hand, there will be an increase in plan counts for both total and new plans in 2023 for Non-SNP MA Only plans, which range in MOOP value from >$500 to >$3000. D-SNP plans saw a rise in >$3,000 and >$500 to <$1,500 MOOP segments for total plans and a rise for new plans only with MOOP above $3,000. South Central market had the highest Non-SNP MA Only of 48 total and 11 new plans, with MOOP costing more than $3,000. While for Non-SNP MAPD, the total number of plans is greater in Great Lakes and new plans are higher in South Central. For D-SNP plans, Georgia had the highest count for both the total plans of 97 and 26 new plans. NY Metro New York (D-SNP), MI South East (Non-SNP MAPD), and TX Houston (Non-SNP MA Only) submarkets have a higher number of total plans in the >$3,000 MOOP segment, while for new plans, it is OH Youngstown (D-SNP), PA Lehigh Valley (Non-SNP MAPD), and TX Houston (Non-SNP MA Only)

CVS Health has plans with MOOP ranging from $500 to >$3,000, among which the number of plans is greatly distributed in the >$3,000 MOOP segment. In the Non-SNP category, there are 459 total and 64 new MAPD plans; 49 total and 6 new MA Only plans in the >$3,000 MOOP segment. CVS Health bags first in Non-SNP MAPD total plans for MOOP with above $3,000, followed by Humana (456), while for new plans, Humana (65) is first by one plan extra than CVS Health (64).

Humana is a competitor even in Non-SNP MA Only plans for CVS Health, with 75 plans and 15 new plans. D-SNP plans only have MOOP above $3,000 with 77 total and 17 new plans. The number of plans higher in the D-SNP category for above $3,000 is UHG which ranks first with 126 total plans and 36 new plans.

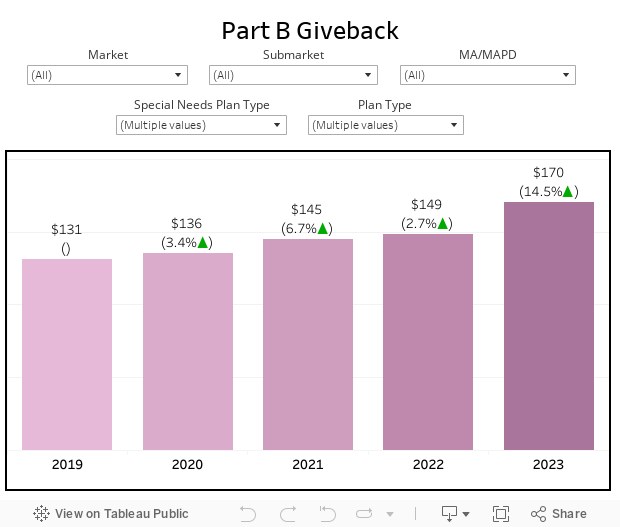

3.6 Part B Give-back

The highest give-back in 2023 is $170 by Humana

Though most plans do not have any givebacks, plan counts consistently increase. Every year since 2019, the maximum value of givebacks has risen only as evident from the graph.

The maximum giveback has increased from $131 (UHG and WellCare) in 2019 to $170 (Humana) in 2023. The maximum giveback by CVS Health is $125, UHG at $109, and $170 for Humana.

Though this is the highest, if you are to look at them as a distribution, you would note an entirely different picture. For CVS Health, the distribution mode is $40, but it is $50 for UHG and $100 for Humana. SCAN Health has a maximum of $125 giveback in 2022, which has declined to $110 during 2023.

For D-SNP, though CVS Health and UHG are not offering any givebacks, Humana has promised $170 as the maximum for a plan.

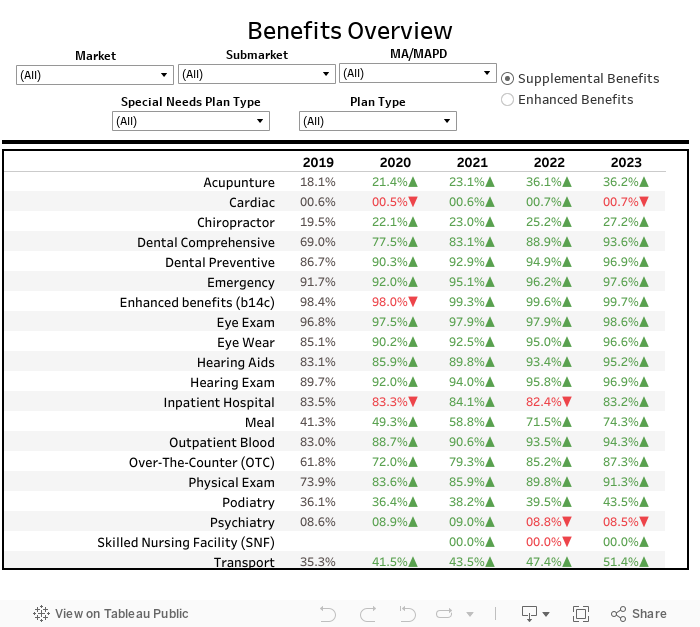

4. Benefit Overview

Fitness Benefit and Remote Access Technologies were covered in a higher number of plans in competitor Organizations as well as CVS Health

Payors are actively expanding the supplemental benefit coverage in 2023. Almost every supplemental benefit saw slight growth, except Psychiatry which noticed a decline in share, and cardiac remained the same as in 2022. Comprehensive Dental and Over-The-Counter (OTC) noticed greater gains, while Transportation, Meals, Hearing Aids, Eye Exams, and Podiatry saw a moderate gain in 2023. Several Enhanced Benefits had a decrease in 2023 as compared to earlier years, with Additional Sessions of Smoking and Tobacco Cessation Counselling benefit being the most significant loss. The Personal Emergency Response Systems (PERS) and Alternative Therapies had the biggest growth of any Enhanced Benefit for 2023 after experiencing modest gains in previous years.

Note: In the 4th section, Non-SNP plans are discussed with MA Only, and MAPD plans separately, while under D-SNP only MAPD plans are discussed, which includes Plan Types (Local HMO, Local PPO, and Regional PPO).

4.1 Supplemental Benefits

Non-SNP MAPD: Acupuncture was included in over 13% in 2019, which has increased to 27.3% in 2022 but observed a very slight decline and accounts for 26.7% in 2023. Similarly, a slight drop was noticed in Physical Exams (72.1% in 2022, 71.7% in 2023), Outpatient Blood (73.6% in 2022, 73.1% in 2023), and Psychiatry (7.7% in 2022, 7.4% in 2023). Inpatient hospital is gradually declining from 2020 (70.8%), while in 2023, the coverage is about 67.4%; similarly, Enhanced Benefits are also dropping in coverage since 2020 (79%) and in 2023 (75.9%). OTC (66.2%), Transport (33.5%), Dental Comprehensive (70.8%), and Meal (54.1%) saw a modest gain in coverage of benefits. Florida market and FL South submarket offered higher inclusion of Supplemental Benefits in Non-SNP MAPD plans. Humana, UHG, and CVS are leading organizations in the inclusion of benefits. OTC offered by Humana accounts for 93%, while CVS Health included over 86% of Non-SNP MAPD. Acupuncture is offered in all the plans Humana offers; CVS Health offers 15%, and UHG offers 13%.

Non-SNP MA Only: This category’s coverage of benefits is low. Apart from Cardiac and Psychiatry, which remained unchanged, all the other Supplemental Benefits showed a gain. Acupuncture benefits are included in over 3.4% of Non-SNP MA Only plans, Dental Comprehensive (7.9%), Enhanced Benefits (b14c) (8.4%), transportation (3.8%), OTC (7.7%) and Meal (6.5%). Supplemental Benefits coverage in Non-SNP MA Only plans was greater in the South Central market and TX Houston submarket. CVS Health offers all the benefits in every Non-SNP MA Only plan except for the benefits such as Acupuncture, Chiropractor, Podiatry, and transportation which have a smaller share. The same trend is noticed in UHG, while Humana follows a similar pattern, except Acupuncture is covered in all Non-SNP MA Only plans.

D-SNP: OTC has also gained a larger share since 2019 (9.4%) in including benefits under D-SNP plans, but in 2023 it is the only benefit observed reduction in coverage of plans accounting for 13.4% against 14.9% in 2022. Acupuncture (6.2%), Dental Comprehensive (14.8%), Enhanced Benefits (15.4%), Eye Wear (15.2%), Meal (13.8%), and transportation (14.1%) are the benefits showing good growth. A higher percentage of Supplemental Benefits were included in DSNP plans in the Florida and FL South submarket. CVS Health offers all D-SNP plans with benefits like Emergency, Enhanced Benefits, Meal, OTC, Outpatient, and Physical Exam. Acupuncture (42%), Chiropractor (38%), Podiatry (89%), and transportation (92%) are benefits of having coverage in CVS Health. And the remaining benefits are covered at 99% as for D-SNP plans. Psychiatry benefit is not covered in any of the D-SNPs offered by CVS Health. More than 90% of the plans are covered with key supplemental benefits offered by Humana and UHG, but the share of Humana coverage for OTC is very low, constituting only 5%. Similarly, coverage for Acupuncture (28%) and Chiropractor (49%) by UHG is relatively low compared to other benefits.

4.2 Enhanced Benefits

Non-SNP MAPD: Unlike D-SNP and Non-SNP MA Only plans, the highly included Fitness benefit showed a reduction in coverage since 2021 for the Non-SNP MAPD plan type, which accounts for 75.1%. Remote Access Technologies have seen a gain in the inclusion of plans over 58% against 56.4% in 2022. Personal Emergency Response System (PERS) has also increased its coverage to 23% in 2023 from 14.5% in the previous year. Nutritional/Dietary Benefits (21.5%), In-Home Support Services (14.9%), Alternative Therapies (6.4%), Chemotherapy-related benefits (6%), and Bathroom safety services (9%) have seen moderate gain. A major decline was noticed in the Medical Nutrition Therapy of 7.3% of Non-SNP MAPD plans in 2023 against 9.1% in 2022. There were a larger inclusion of Enhanced Benefits in Non-SNP MAPD plans in the Florida market and FL South submarket. All the Non-SNP MAPD plans offered by CVS Health will have Fitness Benefits, and even in Humana and UHG, the coverage is more for Fitness and Remote Access Technologies Benefits. CVS Health is included in over 95% of Remote Access Technologies Benefits.

Non-SNP MA Only: Fitness has increased its coverage from 7.8% in 2022 to 8.4% in 2023, followed by Remote Access Technologies (6.4%), PERS (2.5%), Nutritional/Dietary Benefits (2.3%), and In-Home Support Services (1.6%). All other enhanced benefits fall under less than one percent coverage. In Non-SNP MA Only plans, the South Central market, and TX Houston submarket had greater coverage of Enhanced Benefits. UHG is the main competitor for CVS Health in covering enhanced benefits, while Humana includes only Remote Access Technologies and Fitness benefits in its plans. CVS Health covers all the Non-SNP MA Only plans with Fitness benefits, and 91% inclusion is seen in PERS, Remote Access Technologies, Additional Sessions of Smoking and Tobacco Cessation Counseling, and Nutritional/Dietary Benefits.

D-SNP: Unlike the Supplemental Benefits, Enhanced Benefits under D-SNP have a lesser offering ratio except for some key benefits. Fitness continues to be highly offered, increasing YoY slightly to 14.8% inclusion among D-SNP plans. Remote Access Technologies, the second most offered Enhanced Benefit, also recorded slight growth, now provided in 12.2% of plans. All other benefits fall below 5% inclusion. PERS had seen a noticeable decline in offerings, with the latter falling from 9.7% in 2022 to 4.7% in 2023. DSNP plans had a higher proportion of Enhanced Benefits covered in the Florida market and FL South submarket. UHG (Fitness = 96%, Remote Access Technologies = 90%), Centene (98%, 72%), Humana (97%, 87%), Anthem (98%, 67%), and CVS Health (100%, 92%) are having more coverage in Fitness and Remote Access Technologies. Enhanced benefits continue to be overlooked when in comparison to the supplemental benefits. Better fitness benefits are catching up as they have increased for CVS Health and others. Apart from Fitness, Bathroom Safety Devices, Counseling Services, Home-Based Palliative Care, In-Home Safety Assessment, Nutritional/Dietary Benefits, PERS, Re-Admission Prevention, Post-Discharge In-Home Medication Reconciliation, Telemonitoring Services, Therapeutic Massage, And Weight Training Programs have all seen a higher increase in CVS Health compared to others.

Summary

As the MA market continues to grow, so does the number of plans available for consumers. The average total number of plans in each CVS Health market rose to 306 in 2023 compared to 286 in the previous year, up 7% YoY. Within the new plans segment, the average has risen to 46 from 42 plans per market. At a slightly more granular level, the average total number of plans in each submarket also saw YoY growth to 13.1%, and for new plans, 30.4%.

Within the SNP category, Non-SNP plans are the only category to exhibit a rise in new plans introduced with 15% YoY and had a bigger proportion of plans with no premium, indicating the importance of growth for $0 premium plans. The total number of D-SNP plans has doubled since 2018, but new plans saw a drop of 5.9%. Regarding primary plan factors, the national average for the premium and deductible has been decreasing YoY, while the MOOP and maximum Part-B giveback saw a rise in 2023. Transportation, Meals, Hearing Aids, Eye Exams, and Podiatry have shown a minor increase in 2023 compared to Comprehensive Dental and OTC, which experienced greater gains at the market level.

As for the primary competitors, CVS Health takes the third position in the market for introducing new plans after UHG and Humana. The Gulf States market and the GA Atlanta submarket will have more plans than others in 2023. With a share of 10.1% among its opponents, CVS has the fifth spot in total D-SNP plans, but it holds second place in terms of new D-SNP plans, and it has surpassed other competitors in the introduction of $0 premium plans in the Non-SNP MAPD type. The number of plans was higher with a $0 deductible and having >$3,000 MOOP segments implying the significance of growth noticed in lower premiums and deductibles with higher MOOP value. Key supplemental benefits like Dental Comprehensive and OTC have greater coverage. Humana leads in covering Acupuncture benefits but has very low coverage in D-SNP plans for OTC benefits.