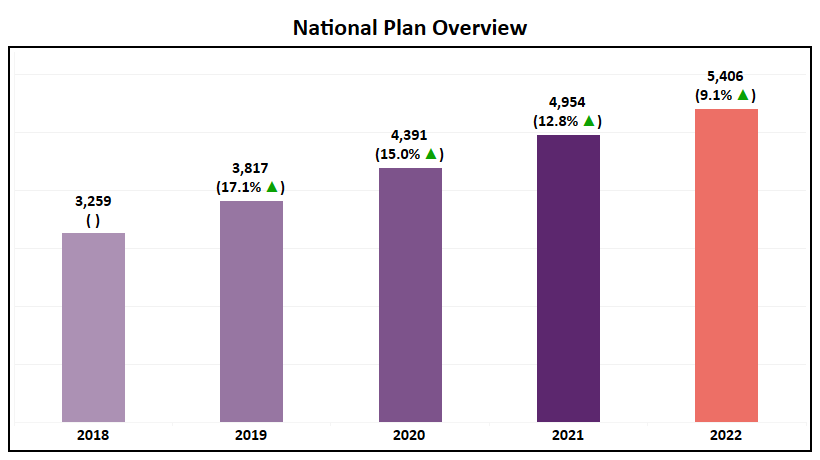

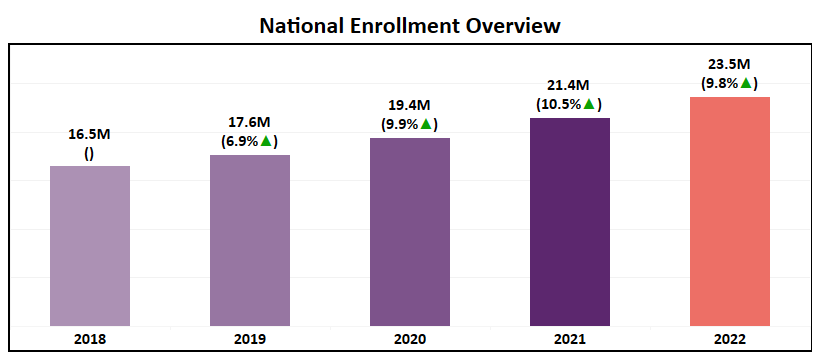

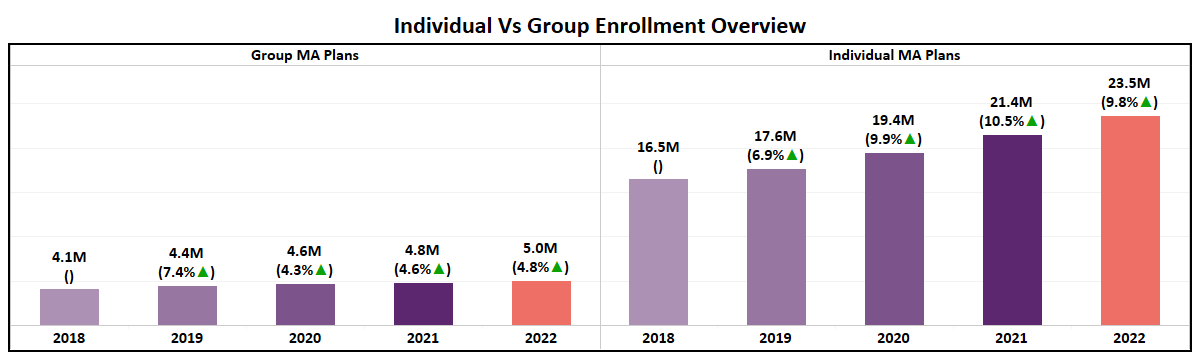

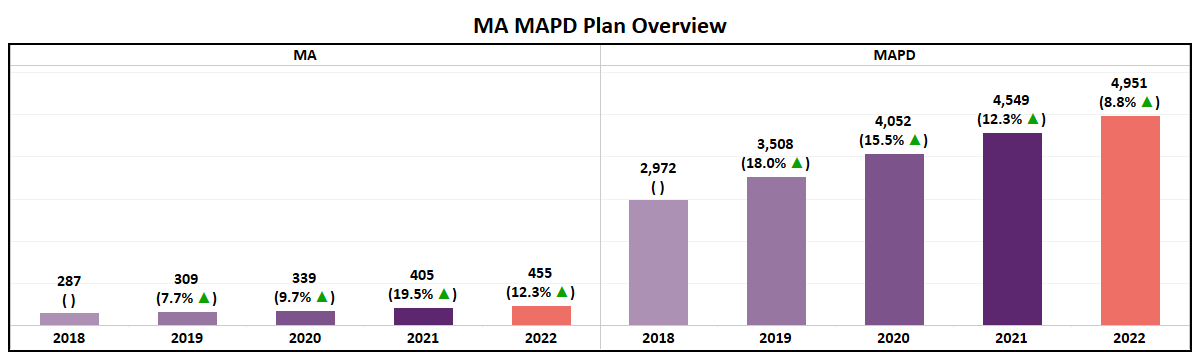

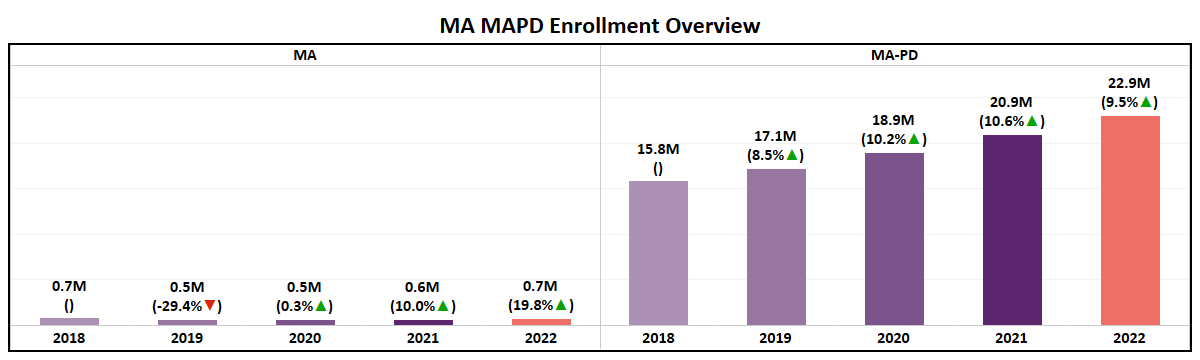

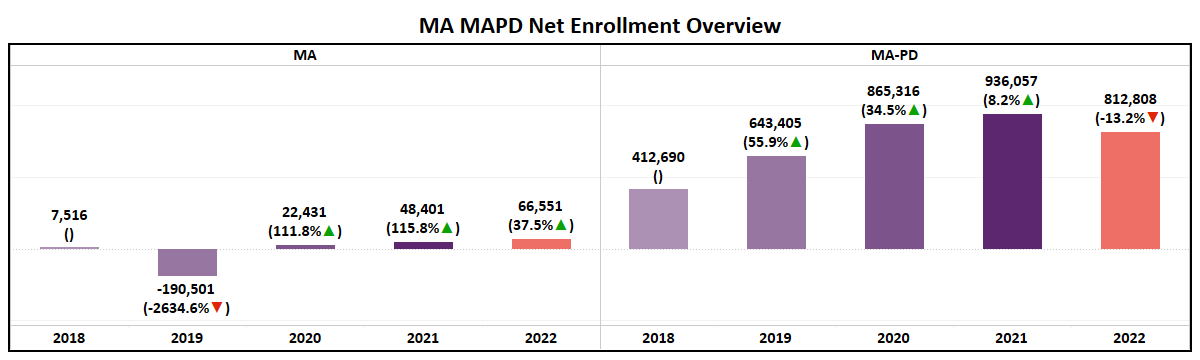

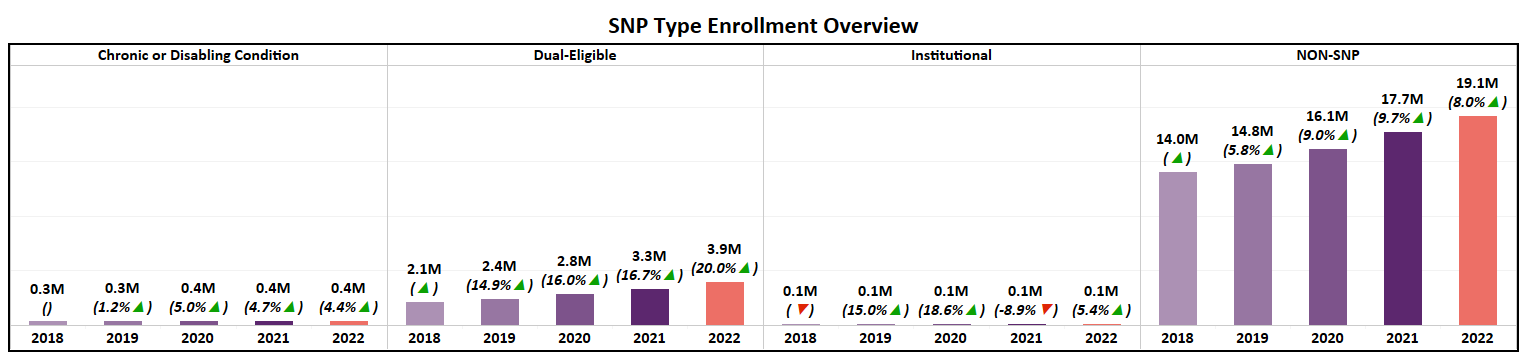

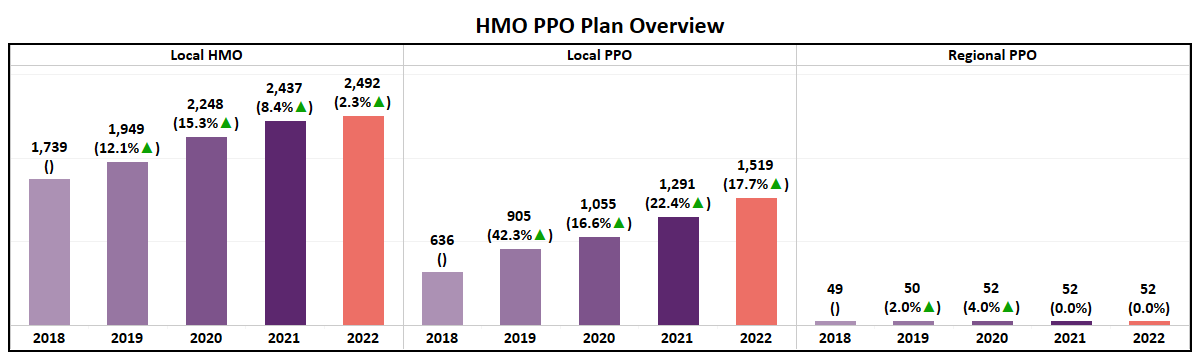

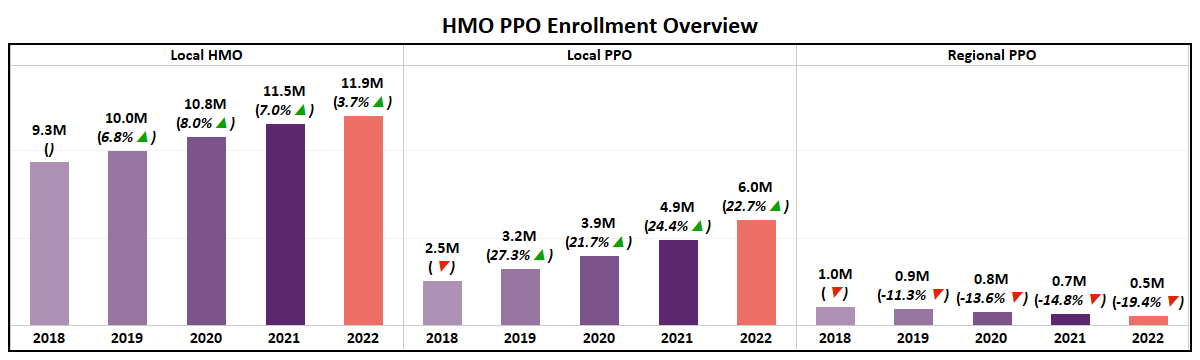

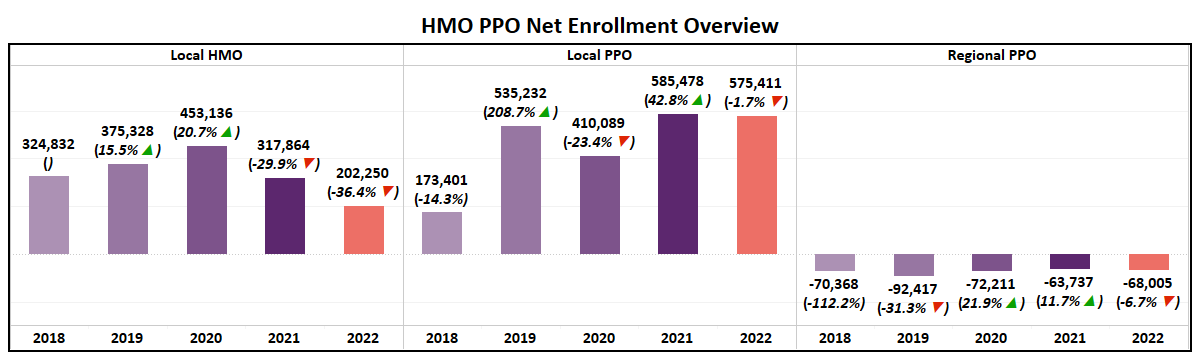

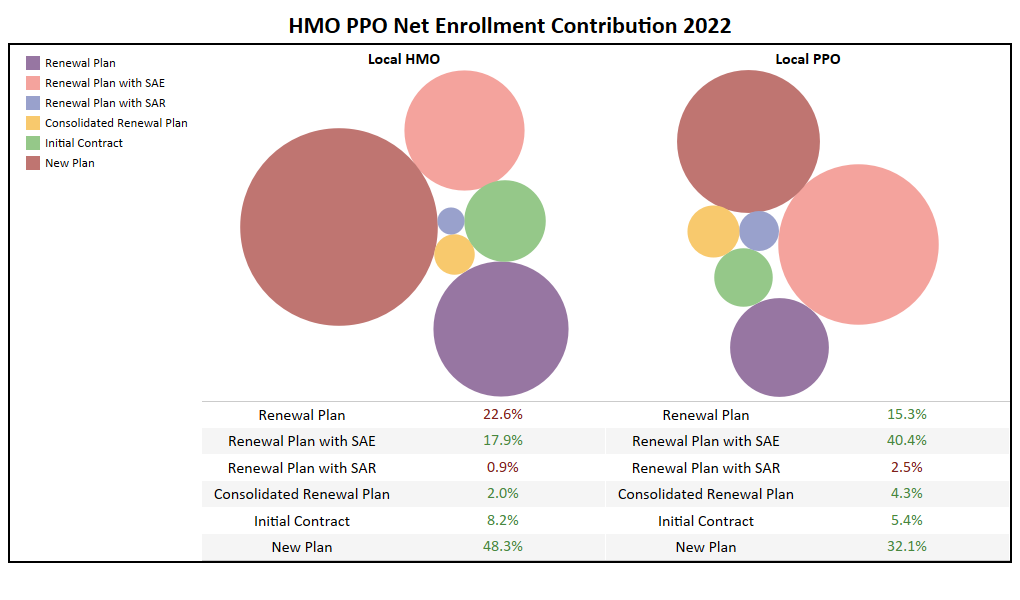

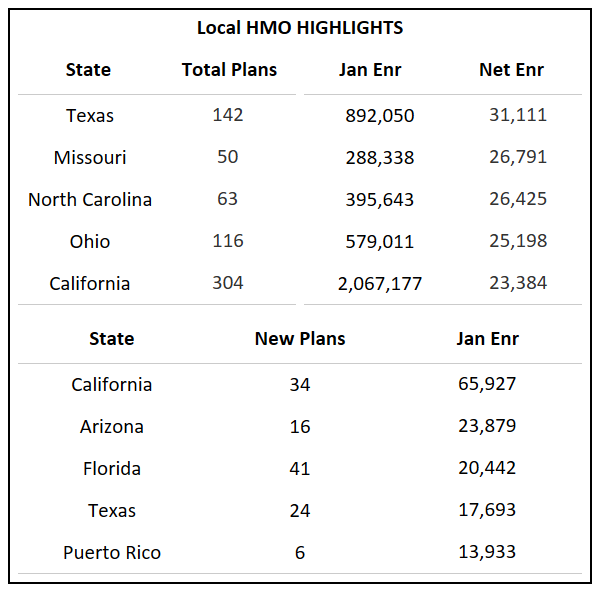

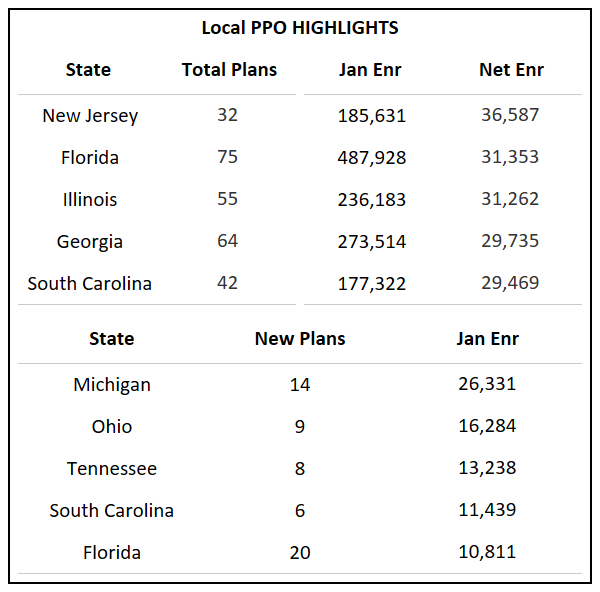

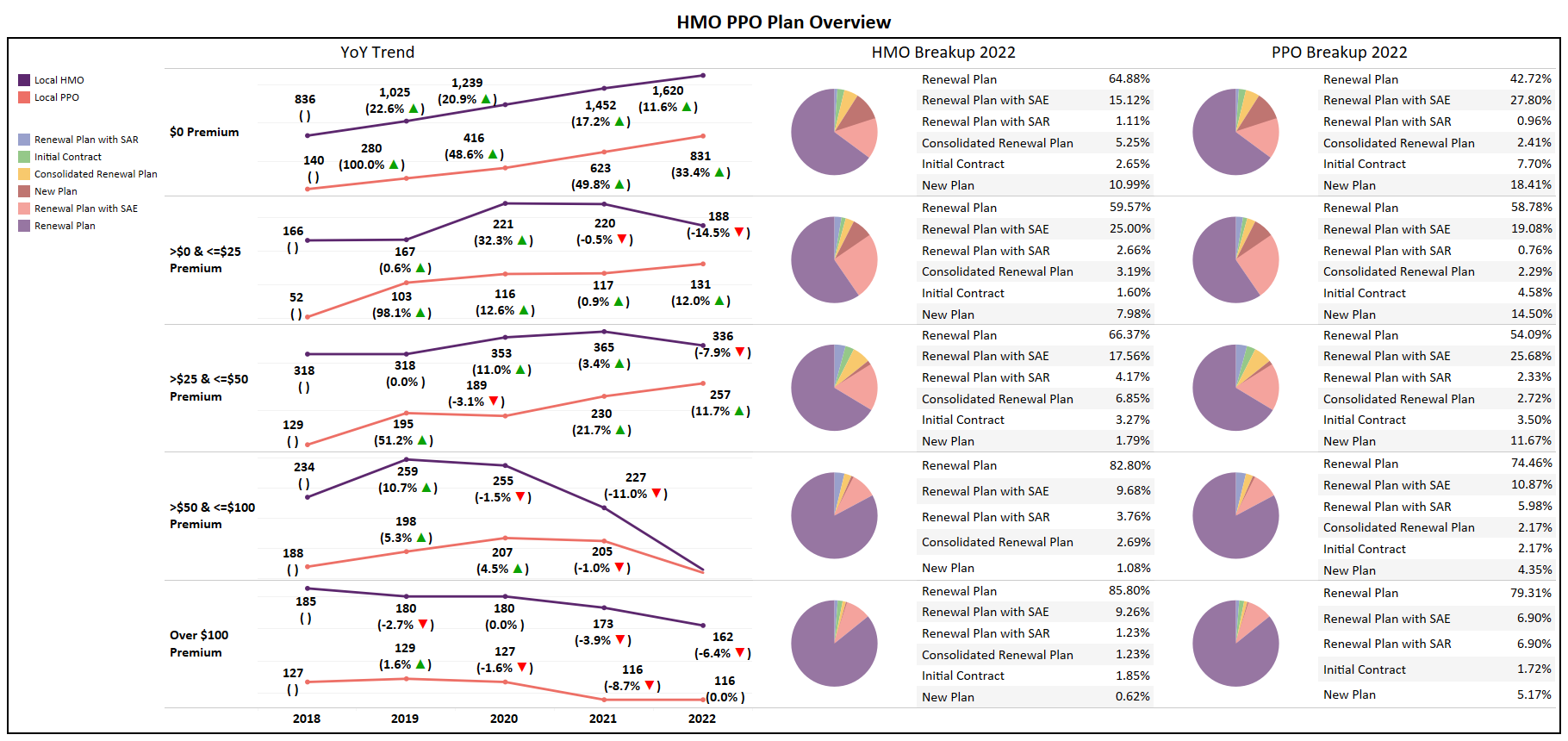

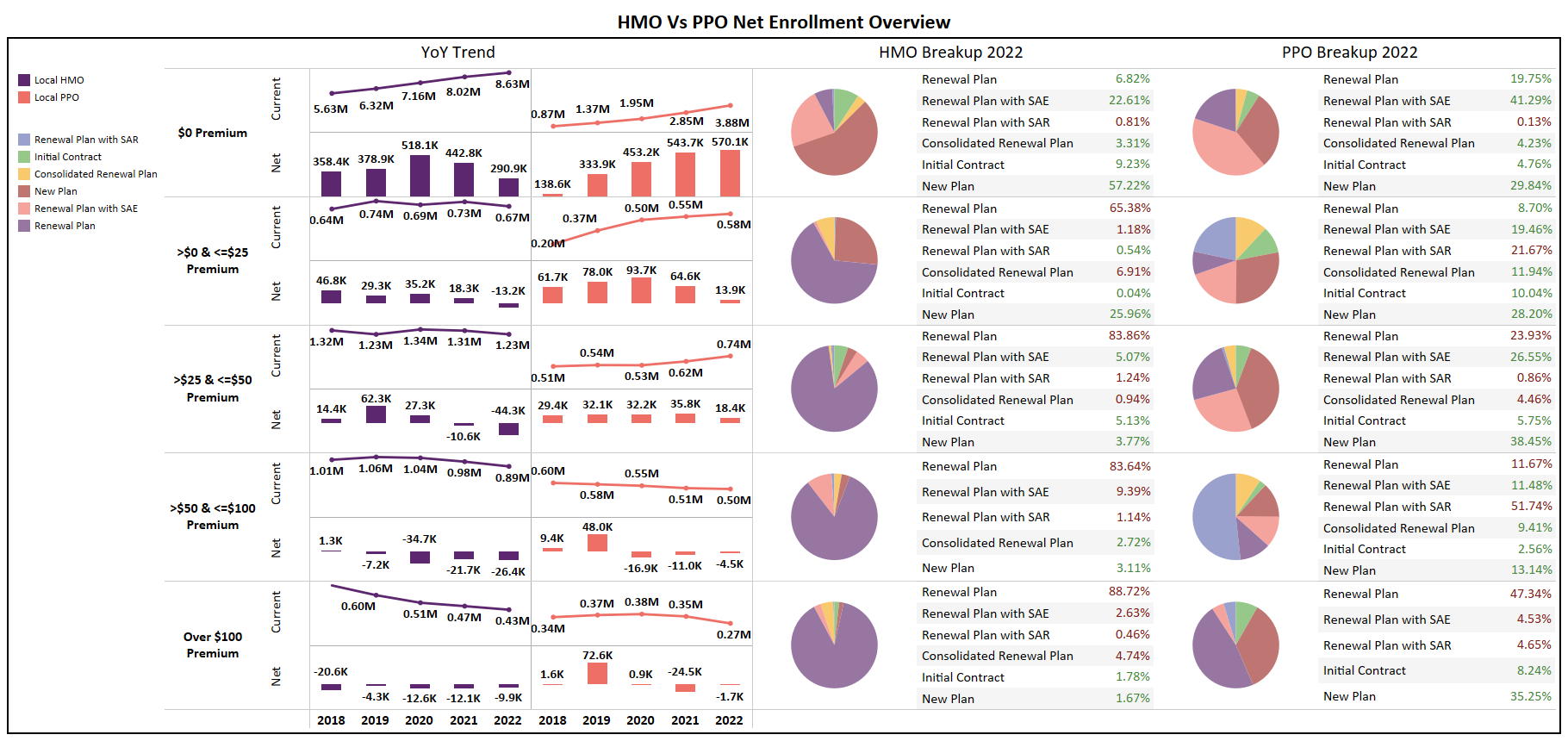

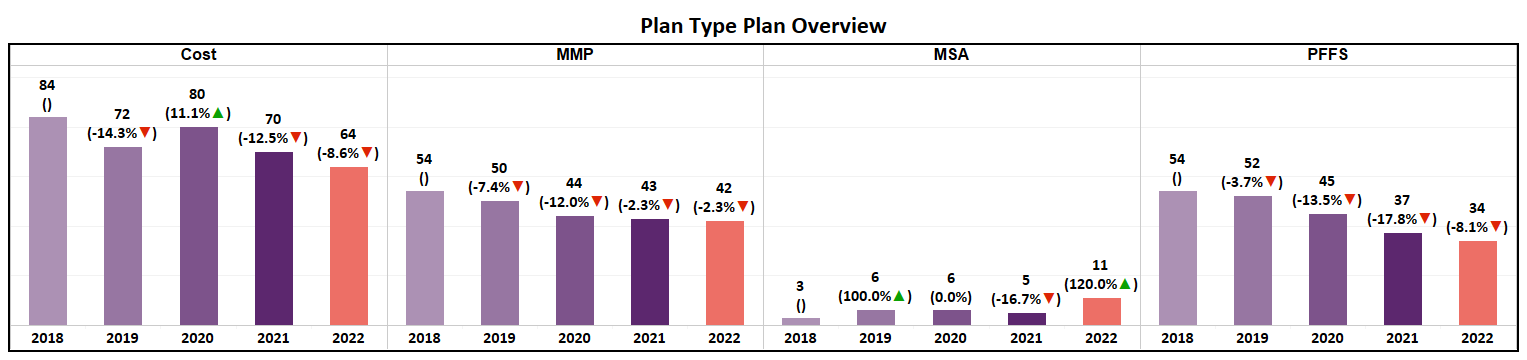

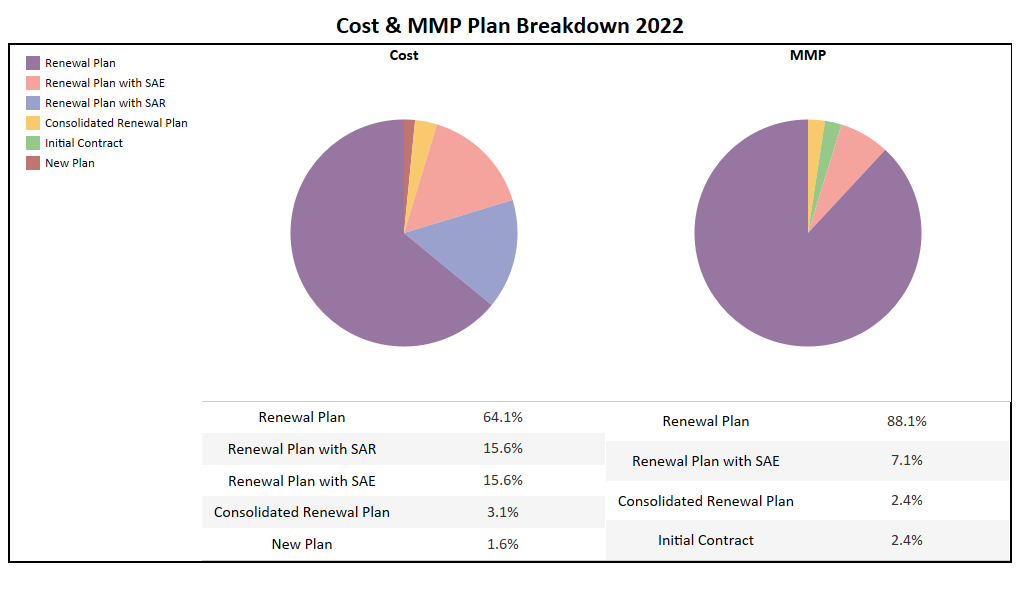

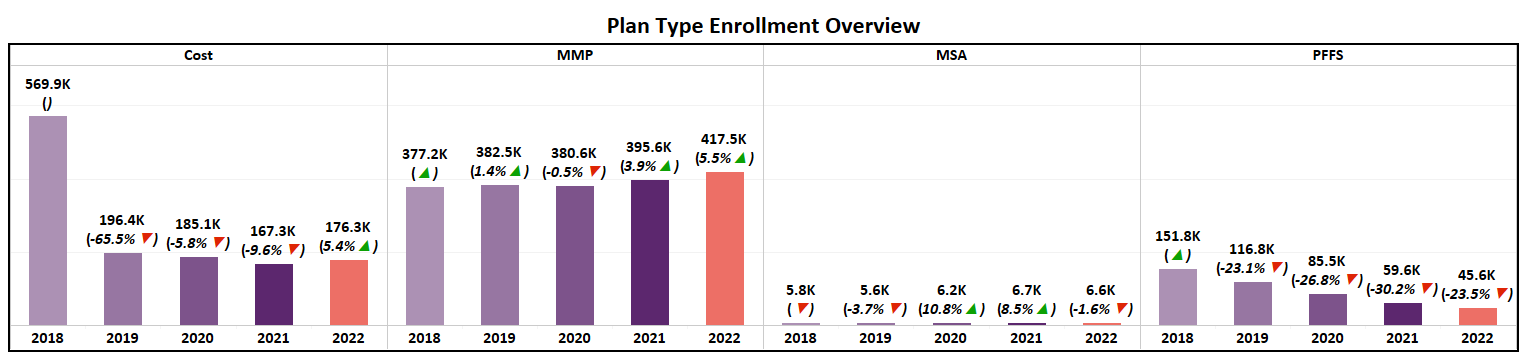

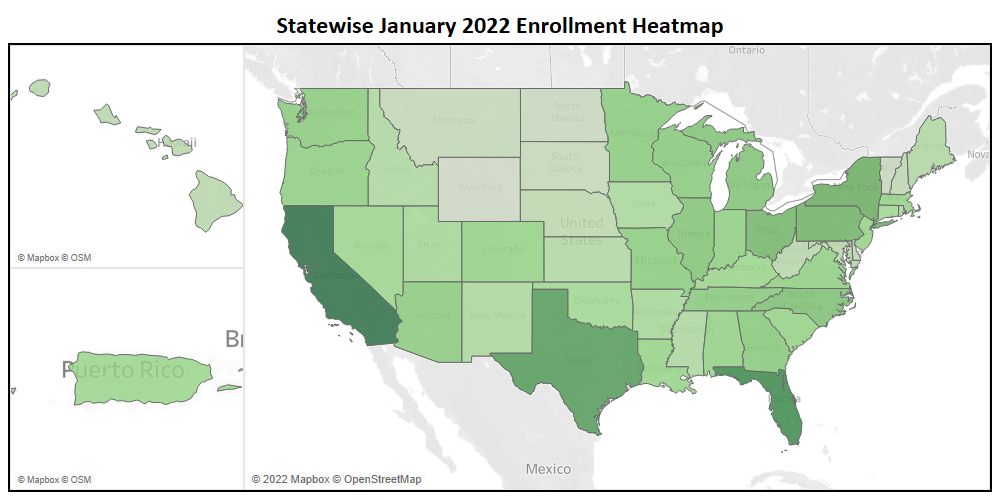

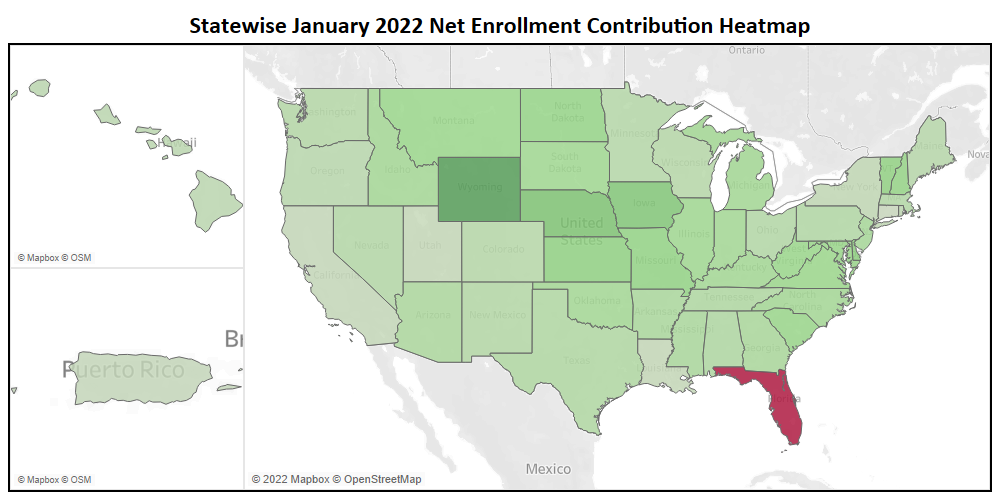

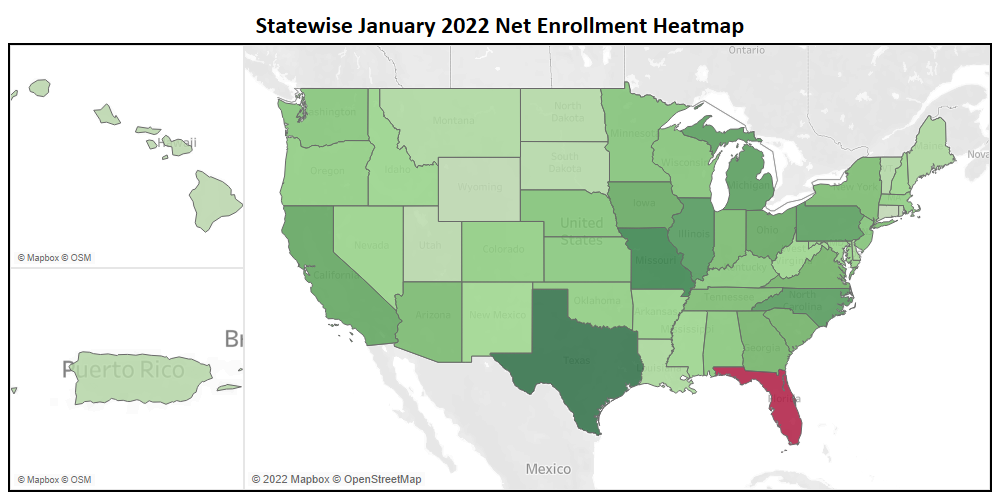

With a vast range of Medicare Advantage offerings designed to cater to the masses, developing the right mix of design features and costs is a daunting task for each participating organization. As of January 2022, enrollment in Medicare Advantage plans has reached 23.5 million, a 9.8% increase over the 21.4 million last year. To meet the needs of the market, the 2022 Annual Enrollment Period (AEP) saw an addition of 452 net plans in total, a rise of 9.1%. While slightly lower than the 12.8% increase seen last AEP, a significant increase none the less. This report was developed to highlight the major enrollment changes in plan type and various cost buckets within the Medicare Advantage market as well as demonstrate how the market has evolved over the past 5 years.