Medicare Advantage 2019

October 25, 2018 Report

Ocotber 25, 2018

Report

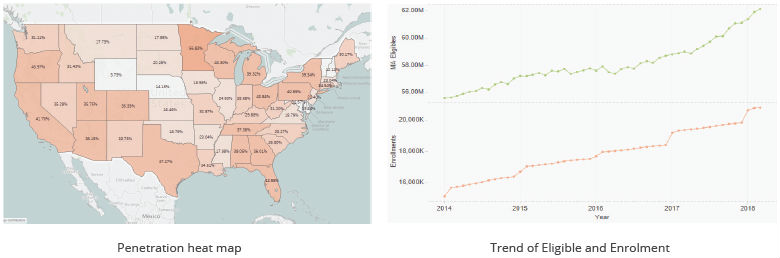

Landscape files revealed the MA plans along with stand-alone PDPs (Prescription Drug Plans) that become available for nearly 60 million beneficiaries to choose plans that best fit their needs. Medicare Payor Organizations struggle to analyze their competitive position in their market based on massive amount of Plan and Benefits data to be released by CMS in the first week of October. This first glimpse at the Medicare Advantage plans available for 2019 analyzes the Landscape files to review the plans offered during the Annual Enrollment Period (AEP). It describes the MA plan choices and availability, and how these compare to last year. Findings include:

Premiums Spread:

CMS officially announced a 6% decrease in Medicare Advantage premiums in 2019, from $29.81 in 2018 to $28.00, to improve health plan affordability for beneficiaries. 83% of MA enrollees are expected to have either the same or a lower premium in 2019. CMS estimates that 46% of MA beneficiaries in their current plan will have a $0 premium.

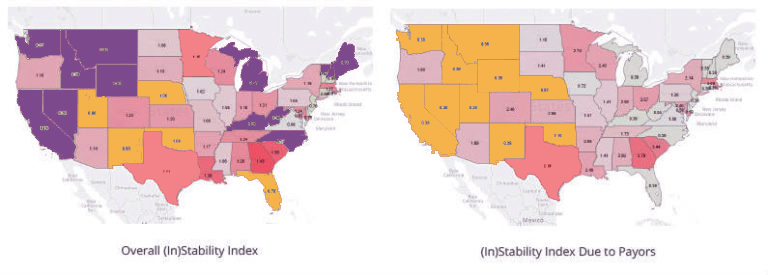

Market Stability:

Market stability across the years is an important component in estimating plan performance in a market by including effects of changes in market dynamics. If costs and deductibles have changed significantly across years, there may be higher prediction uncertainty. HealthWorksAI StabilityIndex™ compares whether markets have significantly changed across 6 parameters: (a) The number of new plans that have been launched in the county (b) Age analysis of plan mix (c) Change in plan types HMO/PPO/SNP etc. (d) Change in premium (e) Changes in drug costs (f) Changes in number of parent organizations.

Texas and Georgia rank highest on the instability index, because of greater changes in the competitive landscape, while Idaho and Indiana are relatively stable markets.

Plans Availability:

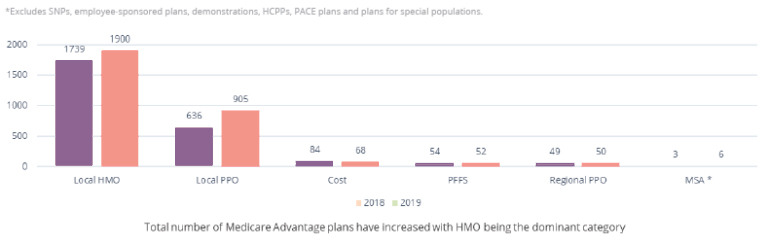

A total of 2,981 MA-PD* plans are offered this year, up from 2,565 – a 16% increase from last year. The increase in number of plans is predominantly among HMOs and Local PPOs. Local PPOs have seen a higher growth (26%) than Local HMOs (9%). Growth rate of Local PPOs is observed to be higher among the big players (53% growth) as compared to the others. HMOs continue to be the majority of plans available and account for about two-thirds (68%) of all plans offered in 2018. In addition, 706 Special Need Plans (SNPs) plans are offered, up from 640 last year. Over 900 Standalone Prescription Drug Plans are also available for the beneficiaries to choose from.

Plan Accessibility

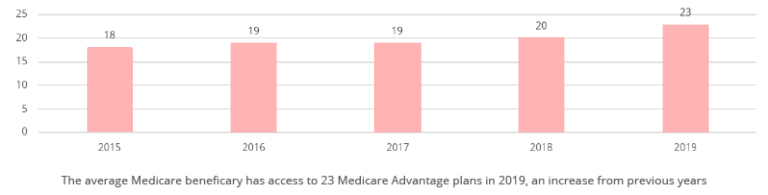

The average Medicare beneficiary will have access to 23 MA plans in 2019 compared to 20 last year. Between 2013 and 2017, the average number of plans available to Medicare beneficiaries was relatively stable. At a county level, the average number of plans available has increased from 12 to 13 plans. However, the number of plans available varies widely across the country. Additionally, beneficiaries have more plans to choose from in metropolitan as compared to non-metropolitan areas.

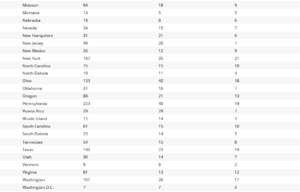

Variation in number of Plans

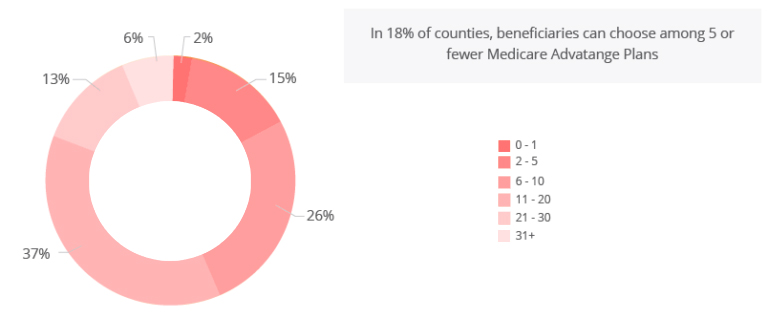

On an average, 14 Medicare Advantage Plans are available per county in 2019, an increase from 12 plans in 2018, but this varies greatly across the country.

- In 13% of counties, beneficiaries can choose from 21 to 30 plans and more than 31 plans in 6% of counties. Most of these counties are in key Medicare states with high eligible population like New York, California, Florida, Ohio, Michigan and Minnesota. Some of the counties like Medina, Mahoning (Ohio), Bucks and Dauphin (Pennsylvania) have up to 50 plan options.

- 11 counties in Florida and 32 counties in New York average 37 plan options for beneficiaries. In contrast, 43% of counties’ (1,352) beneficiaries choose fewer than 10 plans. This, however, decreased from 55% in 2018.

- Compared to last year, 27% more counties have plan choices for 11 and more plans implying an increase in plan options for beneficiaries. However, there are still 72 counties constituting to 0.4% of Medicare beneficiaries that offer one or no plan options.

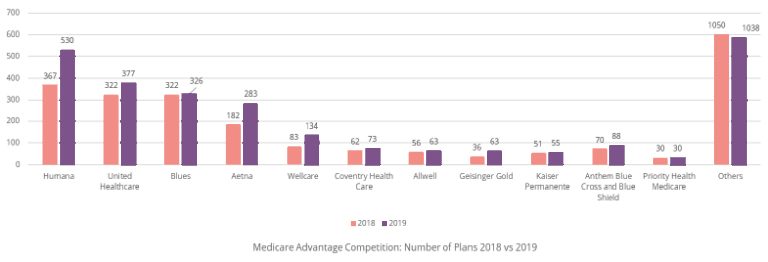

Market competition

The 2019 Medicare Advantage market is comprised of national health plans, Blue Cross Blue Shield organizations, prominent regional health plans and specialized Medicare companies. Based on the 2019 CMS Landscape reports, Humana competes with more MA plans nationwide than any other. UnitedHealth continued to increase its MA plan offerings for the 2019 calendar year with 377 distinct plans identified, up 33 plans from last year. Blue Cross Blue Shield group, that has 36 subsidiaries, is third most competitive plan density followed by Aetna (including Coventry and other affiliates). Geisinger has seen the maximum growth in number of plans from last year (75%) followed by Wellcare (61%) and Aetna (55%).