2025 AEP Insight📊

Exploring 2025 Medicare Advantage Plan Trends: Cost Structures and Benefit Changes

November 7, 2024 Market Research

Table of Contents

With Medicare Advantage plans continuing to grow in popularity, beneficiaries face complex landscape of cost and benefit options. Cost factors such as premiums, deductibles, and Maximum Out-of-Pocket (MOOP) limits play a significant role in plan selection, impacting overall affordability and accessibility. This analysis explores the distribution of Medicare Advantage plans across key premium, deductible, and MOOP categories, examining trends in plan structures and providing insights into how these segments have evolved. Additionally, the report investigates shifts in Supplemental, Enhanced, and Special Supplemental Benefits for the Chronically Ill (SSBCI), delving into the evolving priorities of insurers and beneficiary demand.

Based on the Centers for Medicare & Medicaid Services (CMS) landscape and crosswalk data, this analysis focuses exclusively on Non-Special Needs Plans (Non-SNPs) to deliver a detailed snapshot of the current Medicare Advantage market based on cost factors and benefit offerings and its 2025 trajectory.

The Medicare Advantage landscape in 2025 reveals strategic adjustments to costs and benefits driven by financial pressures and the impact of the Inflation Reduction Act. Premium trends show a shift toward affordability, with a 5% YoY decline in average premiums to $20.43, though the maximum premium rose. While low- or zero-premium plans remain common, mid-tier options have declined, and high-end premiums are growing, reflecting an emphasis on affordability with selective high-tier expansions. Deductibles surged, particularly for drug coverage, with high-deductible plans seeing a major increase, and MOOP limits saw incremental rises, particularly in higher tiers.

Significant increases in drug cost-sharing and a strategic reduction in supplemental benefits like Over-the-Counter, Meal, and Transport offerings declined align with payors’ focus on maintaining financial margins, while Vision, Hearing, and Emergency benefits remain prevalent. Enhanced benefits, including Fitness and Remote Access Technologies remain leading, though Remote Access offerings have declined significantly. SSBCI benefits also adjusted, with General Supports for Living and Non-Medical Transportation increasing, reflecting insurers’ realignment to meet consumer needs amid evolving costs. These shifts emphasize the growing focus on affordability, strategic coverage differentiation, adapting to economic and regulatory changes.

General Overview of Cost factors:

2025: Rising deductibles, stable MOOP, and strategic premium shifts shape the healthcare landscape

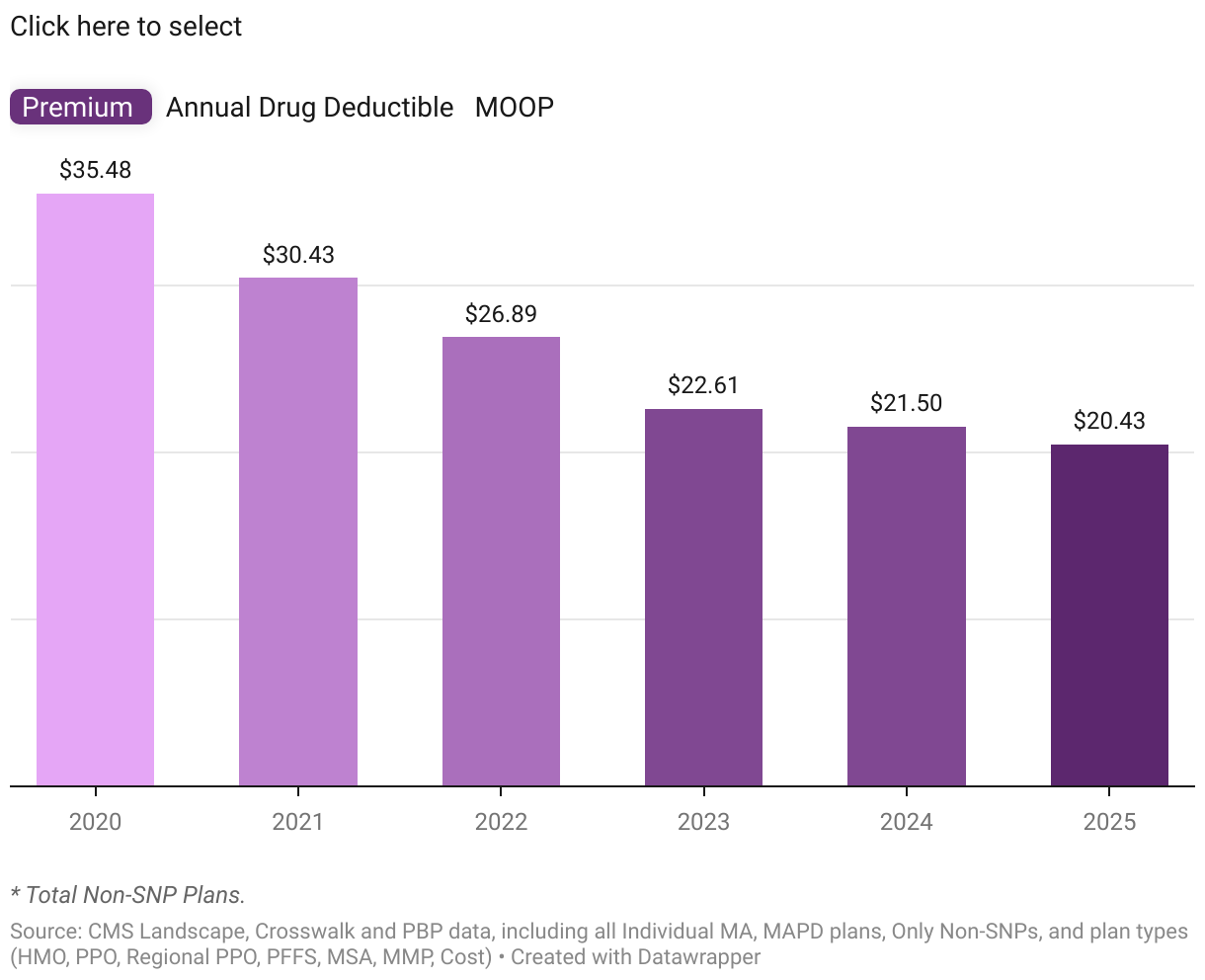

In 2025, the average monthly consolidated premium further decreased to $20.43, marking a steady, though reduced, rate of decline at 5% Year-over-Year (YoY), while the maximum premium rose from $327 to $353. Despite consistent decreases in prior years, the average annual drug deductible saw a dramatic increase, soaring to $248, reflecting a 152.3% YoY rise. This increase was accompanied by a significant jump in the maximum annual drug deductible, reaching $590, the largest annual increase of $45 since 2020.

The average MOOP amount experienced a modest rise to $5,377.30, a 6.4% YoY increase over 2024, indicating that while MOOP remains stable compared to prior years. The maximum MOOP, however, continued its upward trajectory, reaching $9,350, with incremental annual increases since 2020.

Segmentation of Cost factors:

a. Premium

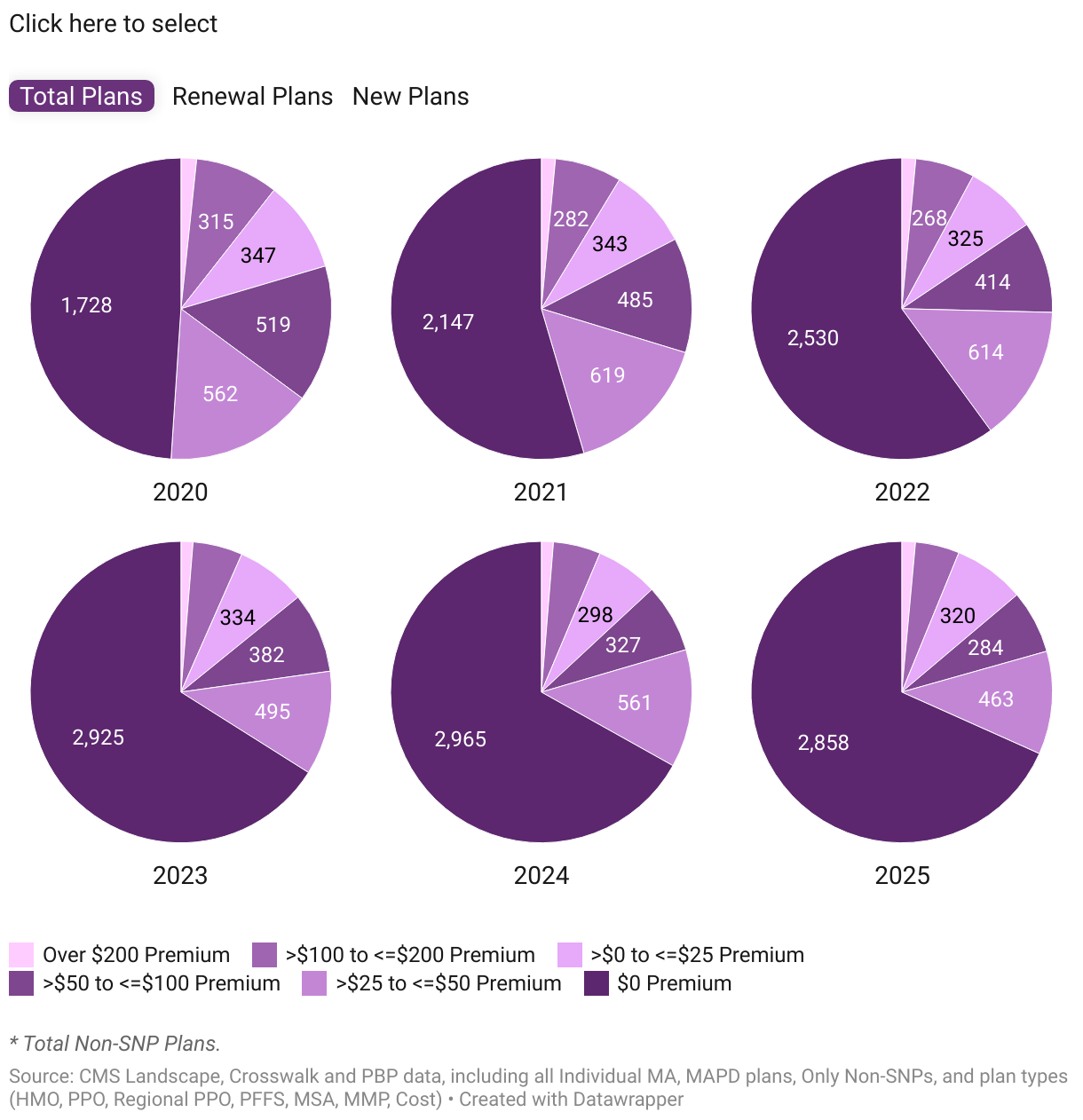

The number of plans in the $0 premium is fewer by 107 in 2025, while the non-zero premium plans are less by 142 plans compared to 2024.

The data reveals a concentrated shift in plan premium structures, particularly across new, renewal, and total plan segments. Dominating the market at around 68% of total Non-SNPs, $0 premium plans saw a slight overall decline of 3.6% YoY (from 2,965 to 2,858), mainly due to a 4.9% decrease in renewals, though new $0 premium plans increased by 6.1% YoY. Meanwhile, plans in the >$0 to <=$25 segment gained renewed traction, with total and renewal categories rising by 7.4% and 9.1% YoY, respectively, highlighting payors’ emphasis on affordability to drive both retention and acquisition.

Mid-tier premium plans (>$25 to <=$100), which make up about 11% in the $25-$50 range and 7% in the $50-$100 range, experienced declines across renewals and slight rise in new plans. Renewal plans dropped significantly from 808 to 660, and new plans increased from 80 to 87, signalling a possible strategic shift away from mid-premium options in favour of low- or high-premium alternatives. At the high end, plans exceeding $200 grew by 7% YoY in 2025, with renewal plans reducing by eight but new plans adding twelve, as compared to none in 2024, suggesting targeted demand for higher-tier coverage offerings.

b. HMO and PPO Deep Dive

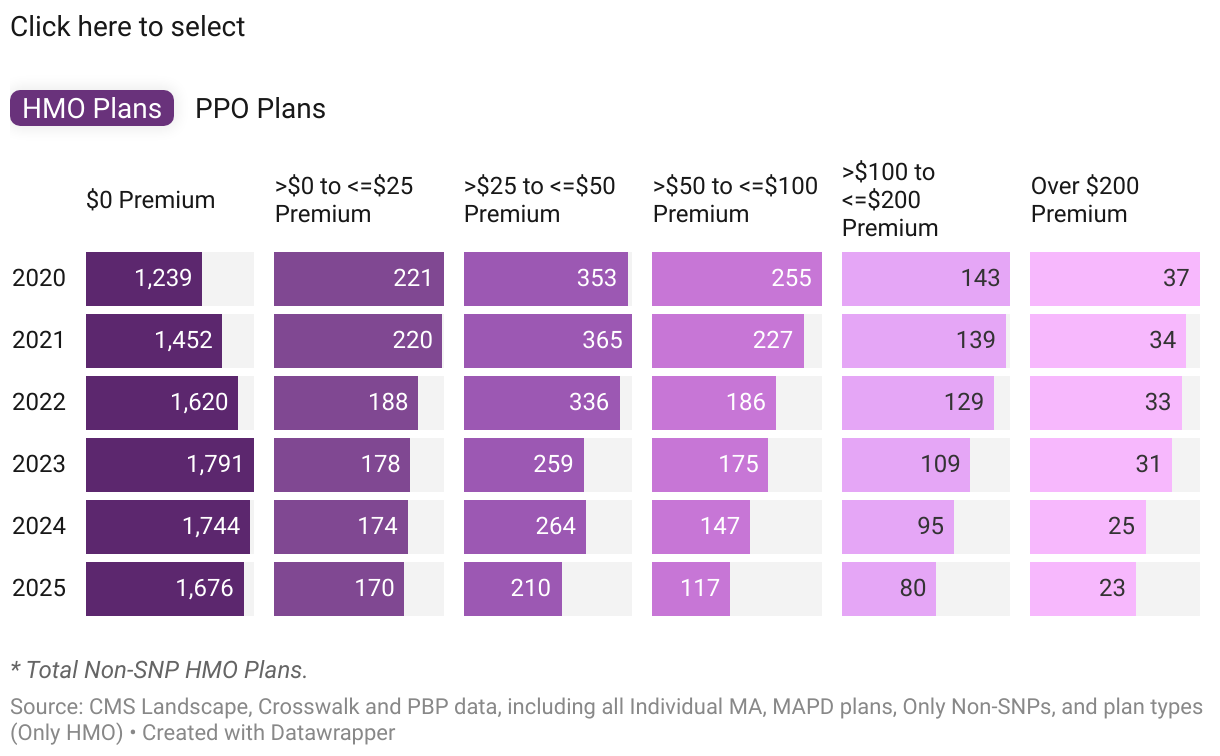

Both HMO and PPO plans saw a decline across all segments, apart from growth in >$0 & <=$25 and >$200 premium categories only in PPO.

The comparison between HMO and PPO plan trends reveals contrasting movements in their premium categories. Zero-premium plans constituted approximately 74% of HMO plans and 64% of PPO plans. For HMO plans, those in the >$0 to <=$25 range experienced a slight reduction of 4 plans, indicating a consistent downward trend. In contrast, PPO plans in this category increased from 121 to 144 plans. The >$25 to <=$50 premium category saw a significant decline, with HMO plans marking a 20.5% YoY drop compared to a 14.2% YoY decline in PPO plans, suggesting a retreat from mid-tier offerings.

Plans in the >$50 to <=$100 premium range showed a reduction of 30 plans in HMO and one plan in PPO compared to 2024. The >$100 to <=$200 segment fell to 80 plans in HMO, representing a 16% YoY decrease, while PPO plans in this category decreased to 86 plans, reflecting a 7% YoY drop. Plans exceeding $200 experienced a minor reduction in HMO, decreasing to 23 plans, while PPO plans saw a slight increase of one plan. Overall, PPO plans highlight a shift towards affordability, particularly in lower premium categories, while HMO plans exhibit a declining trend across various premium ranges, especially in mid-tier options.

c. Drug Deductible

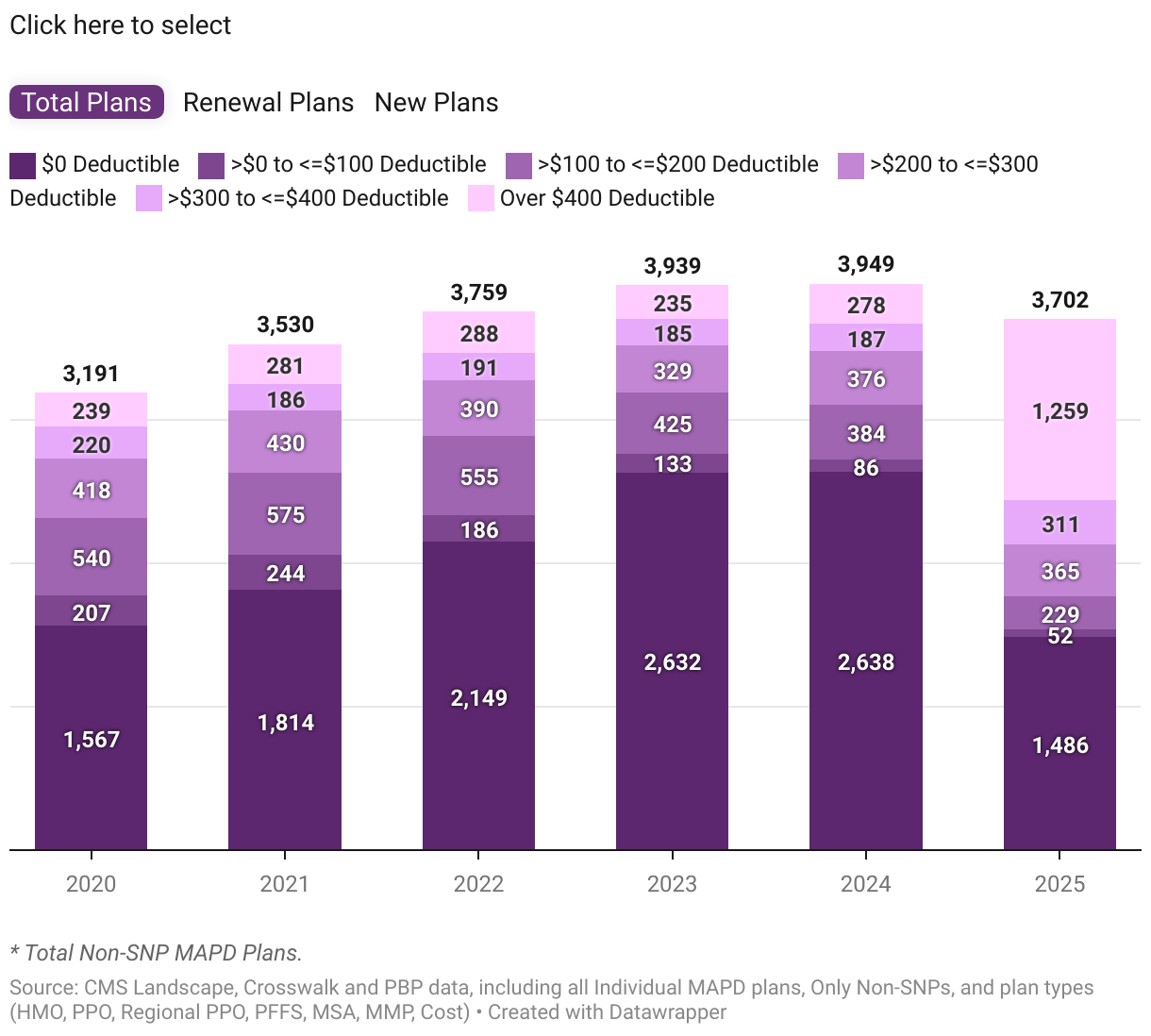

A decline in zero-drug deductible plans (40%) amidst a surge in high deductible plans (34%)

The deductible segmentation data for 2024 and 2025 highlights a significant transformation in plan availability and market percentages. Notably, zero-drug deductible plans have plummeted from 66.8% to 40.1% of total MAPD Non-SNP plans available in 2025. Similarly, the >$0 to <=$100 deductible category decreased from 2.2% to 1.4%, while the >$100 to <=$200 deductible category saw a decline from 384 to 229 plans, resulting in a percentage drop from 9.7% to 6.2%. In contrast, the >$300 to <=$400 deductible category increased its market share from 4.7% to 8.4%, and the Over $400 deductible category saw an extraordinary shift in market share, rising from 7% to 34%.

The trend is stark, with the total number of plans from $0 to $300 drug deductible declining in 2025, while plans over $300 surged dramatically from 465 to 1,570. In the new plans segment, most categories showed a decline, except for the >$400 deductible segment, which increased from 80 to 269, and the >$100 to <=$200 segment, which added three new plans for a total of 20 in 2025. The overall number of $0 deductible plans has dropped significantly from 2,638 in 2024 to 1,486 in 2025, marking a 43.7% YoY decrease. This trend is echoed by a significant reduction in renewal plans, which fell from 2,369 to 1,351, and new plans from 269 to 135. This indicates a shrinking availability of low-deductible options, although insurers are trying to maintain a baseline of offerings in this category.

Conversely, high-deductible plans are witnessing a substantial resurgence. The total plans in the Over $400 deductible category skyrocketed from 278 to 1,259, reflecting a staggering 352.9% YoY increase, with new plans increasing from 37 to 246. Renewal plans in this category also rose significantly from 241 to 1,013, underscoring a shift in both the introduction and retention of high-deductible plans.

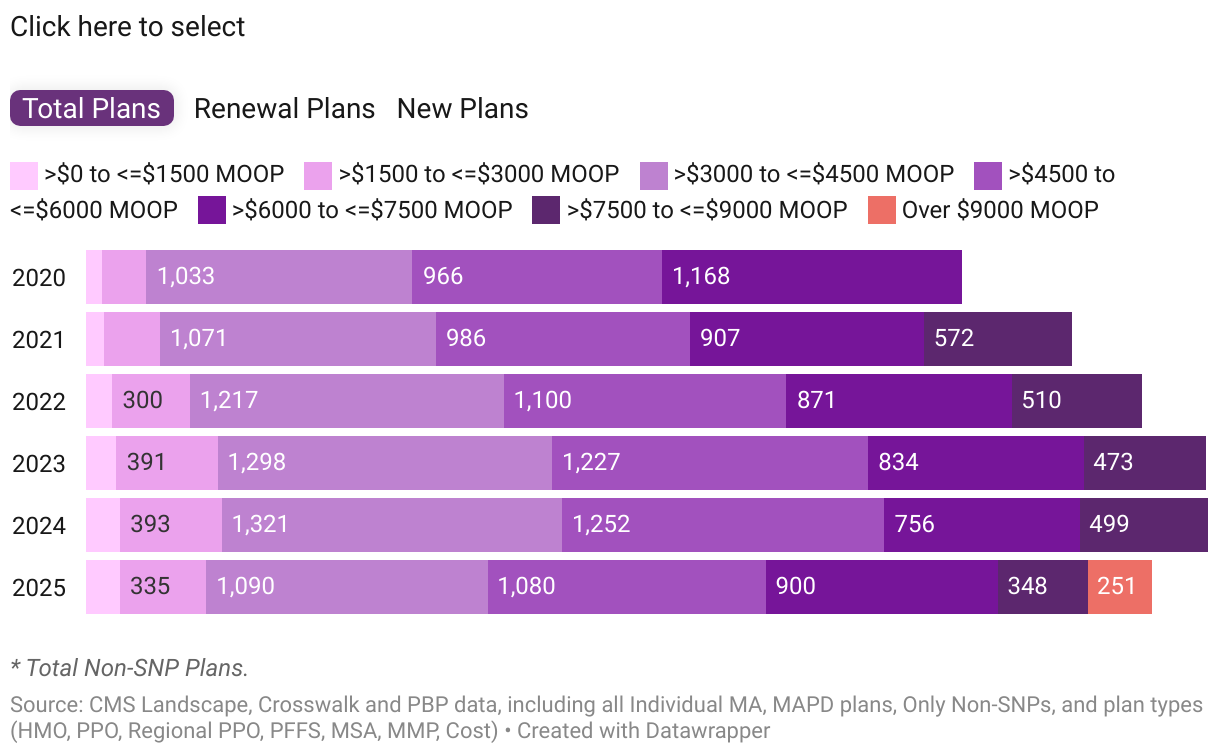

d. MOOP

For the first time in recent years, 251 plans (6% of total Non-SNPs) now have a MOOP exceeding $9,000.

The 2025 MOOP data for Non-SNP plans shows a shift towards higher out-of-pocket limits, with approximately 74% of plans now in the $3,000 to $7,500 range and around 14.5% exceeding $7,500. Plan counts fell across all the segments compared to 2024, except in the >$6000 to <=$7500 category. The lowest MOOP segment (>$0 to <=$1500) saw slight declines in total and renewal plans by 0.7% and 2.7% YoY, respectively, while new plans grew modestly by 8.3% YoY, indicating limited growth for low-MOOP options.

In the mid-range, particularly in the >$1500 to <=$3000 bucket, total and renewal plans grew until 2024 but dropped from 393 to 335 total plans in 2025, with volatility in new plans that otherwise maintained a steady presence. The >$3000 to <=$4500 category, once growing robustly, saw notable drops in 2025, with total plans down by 17.5% YoY, renewal plans by 192, and new plans by 39, marking a pullback from mid-MOOP offerings.

Higher MOOP categories show a contrasting trend, particularly the >$6000 to <=$7500 range reversed its earlier downward trend with total plans rising 19% YoY and an increase of 108 renewal plans compared to the previous year. New plans in this category also grew significantly, jumping from 83 to 119. The >$7500 to <=$9000 MOOP segment, however, experienced significant declines in 2025, with total plans down by 30.3% YoY, reflecting a declining market interest in this specific high-MOOP range, while new plans, though fewer, showed a slight increase.

Overall, the data reflects a shifting trend away from lower and mid-range MOOP plans in favour of high-MOOP options, particularly above $6000, where growth is seen both in total, renewal, and new plans. This could indicate changing consumer preferences or insurers offering fewer low-MOOP options while strengthening higher-MOOP plan offerings, especially for new plans.

Benefits Overview

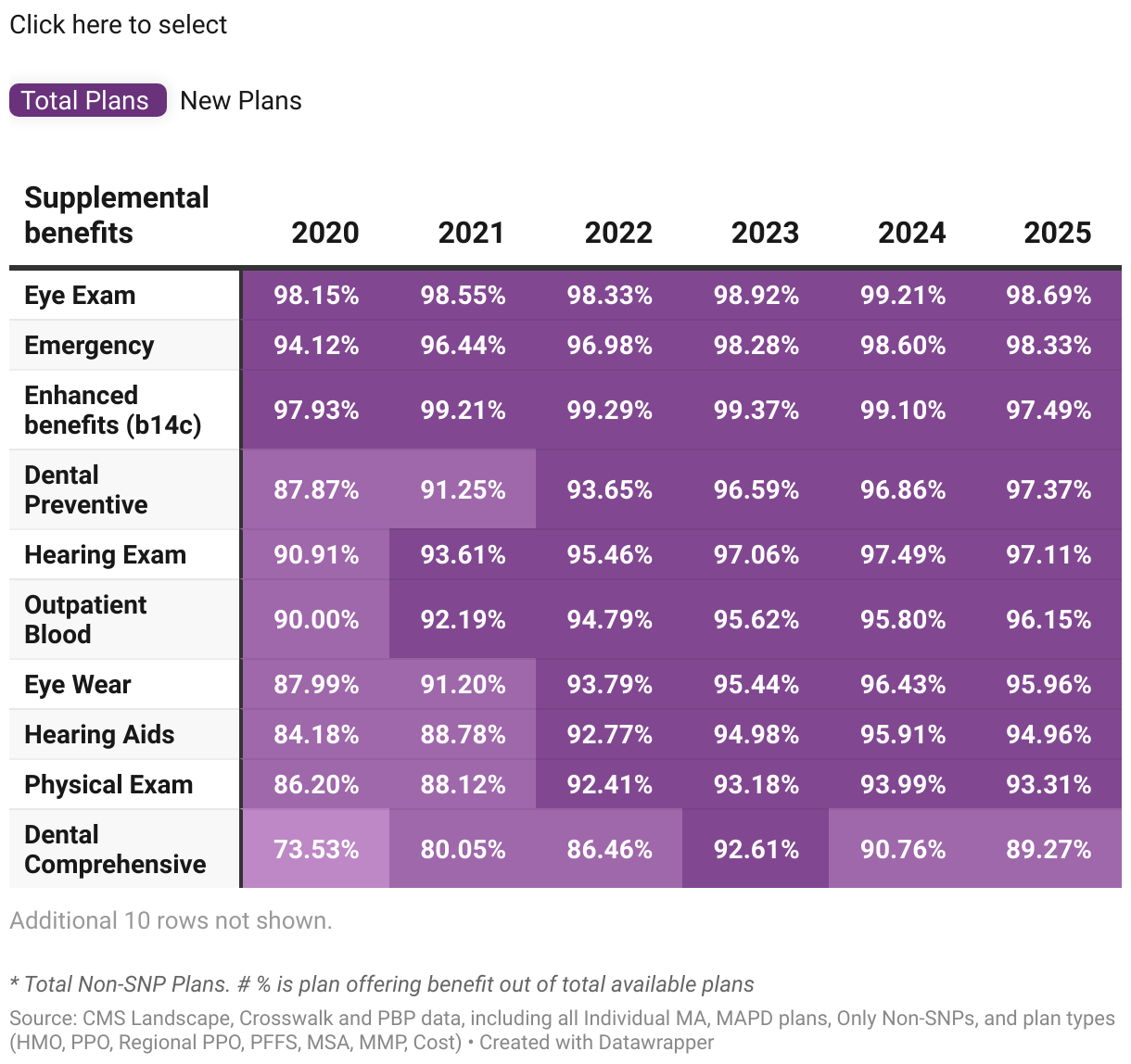

a. Supplemental Benefits Overview:

The inclusion of Over-the-Counter (OTC) benefits in plans has seen a sharp decline, with Meal and Transport benefits also experiencing significant reductions.

As the plan count decreased at the national level, the number of plans offering various supplemental benefits also declined across all categories compared to 2024. High-prevalence benefits like Eye Exam, Enhanced Benefits, and Emergency consistently show high adoption rates, with around 98-99% of plans including these benefits. Despite this, there is a slight decline in the number of plans offering these benefits in 2025, with YoY changes showing declines of -6.0%, -7.1%, and -5.8%, respectively. On similar lines, Hearing Exam and Dental Preventive also maintain high inclusion percentages of about 97%, though they saw saw reductions in count: Hearing Exam plans dropped from 4,317 to 4,062, while Dental Preventive decreased from 4,289 to 4,073.

Mid-level benefits such as Hearing Aids, Eye Wear, Physical Exam, and Outpatient Blood continue to show higher offering rates. Hearing Aids maintain a 95% inclusion rate, despite 275 fewer plans than in 2024. Eye Wear, included in 96% of plans, saw a 6% YoY decline. Physical Exam benefits, now included in 93% of plans, decreased from 4,162 to 3,903, while Outpatient Blood, with a 96% inclusion rate, experienced a 5% YoY drop. Dental Comprehensive have fewer plans reaching 3,734 in 2025 from 4,019 accounting to 7% YoY drop.

The most significant drop in benefit offerings was observed in Over-the-Counter (OTC), which declined by 738 plans, resulting in a decrease in its inclusion rate from 85% to 72.4%. This was followed by Meal benefits, which saw a reduction of 441 plans, and Transport benefits, which decreased by 344 plans. These reductions reflect a notable shift in the availability of these supplemental benefits. Transport and Acupuncture benefits, which had experienced significant growth in prior years, saw notable drops in 2025, with Transport plan inclusion rates decreasing from 36.7% to 30.6% and Acupuncture from 33.9% to 31.8%. Chiropractor benefits down by -20.5% YoY and Psychiatry by -13.4% YoY.

The smallest prevalence is observed in Cardiac and Skilled Nursing Facilities (SNF), which have consistently low shares of total plans. SNF benefits experienced a YoY decline of 2.8%, while the number of Cardiac plans dropped significantly from 44 to just 19 in 2025.

In 2025, new plan additions reveal notable trends in benefit inclusion: Emergency and Eye Exam benefits lead with approximately 513 and 509 offerings, respectively, showcasing strong demand and high prioritization. Benefits such as OTC, Meal, Transport, Chiropractor, and Podiatry show lower inclusion rates in newly added plans compared to 2024 levels, while Cardiac and SNF lack any new plans for the second year in a row. Conversely, OTC in new plans offered in 503 plans (+49 from 2024), marking the highest increase. Inpatient Hospital follows closely with 462 new plans (+46), and Physical Exam benefits reach 494 plans, adding 40 more plans compared to the previous year.

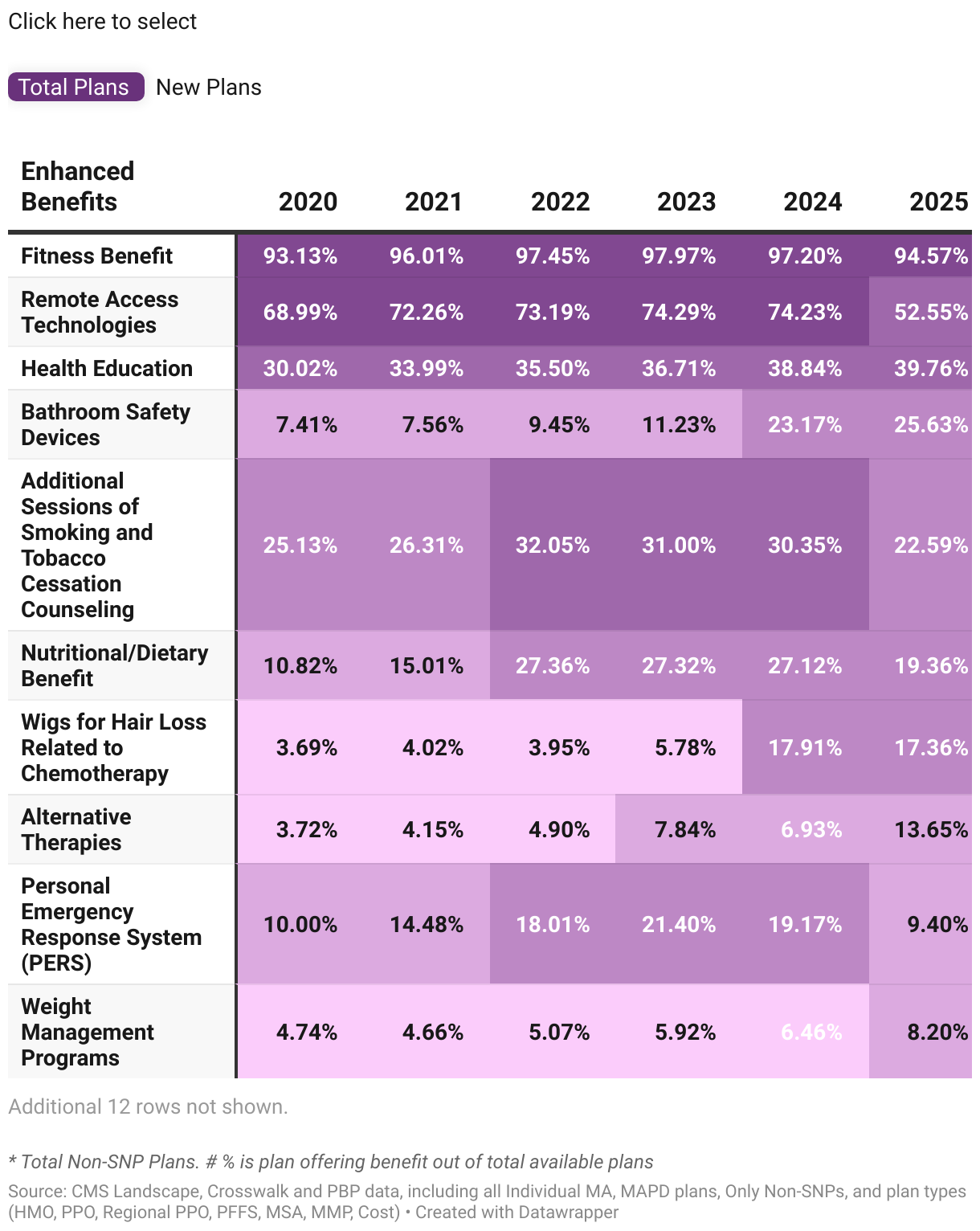

b. Enhanced Benefits Overview:

Fitness and Remote Access Technologies Lead Enhanced Benefits: Fitness at 94.6% and Remote Access at 53%, with all other benefits under 40% inclusion.

Among 22 different Enhanced benefits, only three experienced an increase in plan count: Alternative Therapies (+264), Weight Management Programs (+57), and Bathroom Safety Devices (+46). Conversely, all other benefits saw a decline. Despite a slight drop in prevalence, the Fitness Benefit remains one of the most widely offered Enhanced benefits, with its inclusion rate decreasing from 97.2% in 2024 to 94.6% in 2025, reflecting an 8.1% YoY decline of 348 plans. Remote Access Technologies experienced a substantial decrease in availability, dropping from 3,287 to 2,198, marking a significant 33.1% YoY decline. This trend may indicate a shift away from telehealth as pandemic-related demands stabilize. Health Education continued to grow modestly, with a slight increase in offerings to 39.8%, although its growth rate has slowed.

The highest reduction in offerings was observed in Remote Access Technologies, which declined from 74.2% to 52.5%. This was followed by the Personal Emergency Response System (PERS), which dropped from 19.2% to 9.4%. Medical Nutrition Therapy (MNT) also saw a significant decline, decreasing from 564 plans to 152. Additionally, the Smoking and Tobacco Cessation Counseling benefit experienced a notable YoY reduction of 29.7%, falling from 30.4% to 22.6%. While the Nutritional/Dietary benefit maintained a reasonable presence, it experienced a significant YoY decline of 32.6%, decreasing from 27.1% to 19.4%.

Adult Day Health Services already rare in previous years, has now become virtually non-existent, with only 1 plan offering it in 2025, while Re-admission Prevention, Counselling Services and Post-discharge In-Home Medication Reconciliation benefits saw declining inclusion rates, reflecting less focus.

Despite the introduction of new plans, offerings for the PERS have significantly decreased from 99 plans to 36. MNT also saw a reduction of 85 plans, dropping from 102 in 2024, while Remote Access Technologies experienced a decline of 80 plans, reaching a total of 281. In contrast, the highest increases in new plan offerings were observed in Alternative Therapies (from 30 to 124 plans), Weight Management Programs (from 33 to 101 plans), and Bathroom Safety Devices (from 120 to 176 plans). Overall, Fitness remains the leading benefit with 495 new plans in 2025.

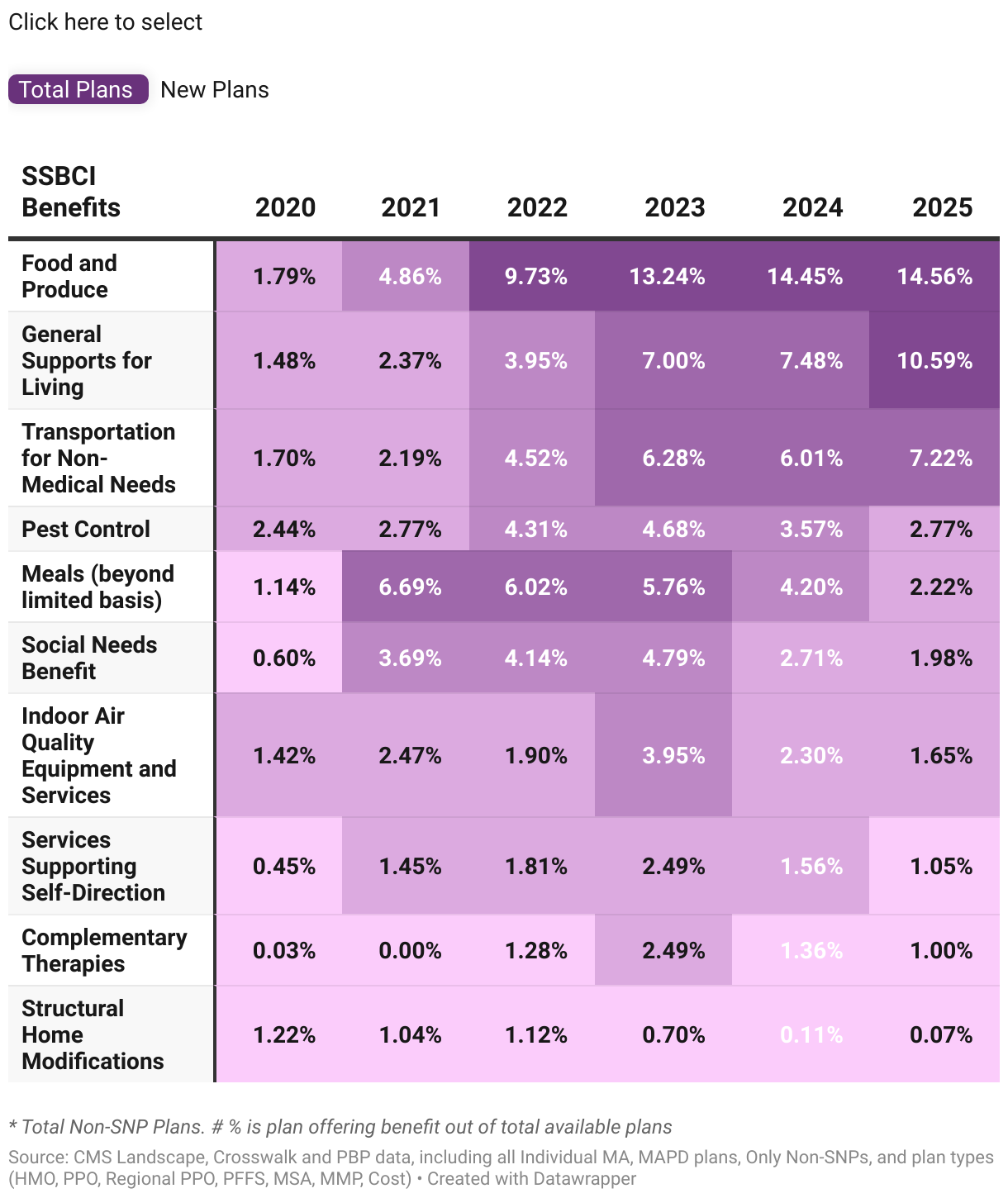

c. SSBCI Overview:

General Supports for Living is included in 116 new plans (+68), marking the highest absolute increase among SSBCI benefits at approximately 26%.

Compared to Supplemental and Enhanced benefits, SSBCI offerings have seen moderate declines overall, with exceptions like General Supports for Living and Transportation for Non-Medical Needs, which have risen in availability. Food and Produce remains the most offered benefit among SSBCI, though it slightly declined to 609 offerings in 2025 (640 in 2024), making up 14.6% of the total. General Supports for Living saw a significant increase, reaching 443 offerings (10.6% of the total), up from 310 in 2023, signaling a stronger focus on essential support services. Transportation for Non-Medical Needs also shows growth, increasing from 6% to 7.2% of the total, reflecting a sustained commitment to enhancing accessibility.

In contrast, several moderate-prevalence benefits have experienced continued declines. For instance, Meals (Beyond Limited Basis) has dropped for a second consecutive year, decreasing from 255 plans in 2023 to 186 in 2024, and further down to 93 offerings in 2025—a notable 50% YOY decrease, raising concerns about its prioritization. Similarly, Pest Control and Social Needs Benefit have declined to 116 (2.8%) and 83 (2.0%) offerings, respectively, signaling a reduction in focus on these services. Indoor Air Quality Equipment and Services has also seen a substantial decrease, dropping from 102 to 69 plan offerings.

At the lower end of the spectrum, Services Supporting Self-Direction has dropped to 44 offerings (1.1%) from 69 in 2024, while Complementary Therapies fell to 42 (1.0%) after previous growth, suggesting a need for strategic reassessment of these offerings. Structural Home Modifications has plummeted to just 3 offerings (0.1%), underscoring a potential gap in addressing critical home-related needs.

General Supports for Living benefit offering experienced a spike in new plans from 10.1% to 22.5%, that added 68 more plans in 2025. Followed by Food and Produce increased from 110 to 141 plans and Transportation for Non-Medical Needs also increased from 7.3% to 11% in new plans.

Conclusion

In 2025, the Medicare Advantage market reflects significant adjustments in both cost and benefit structures, highlighting insurers’ strategies to balance affordability with comprehensive coverage. While premium categories reveal a shift towards affordable options with notable declines in mid-range premiums, deductibles have trended higher, particularly among new plans. MOOP limits have seen incremental increases, particularly at higher thresholds, indicating a possible shift towards cost-sharing.

Supplemental and Enhanced benefits, including commonly prioritized services like vision, hearing, and emergency benefits, maintain strong inclusion rates, although offerings such as OTC benefits and Remote Access Technologies show notable declines. As these shifts signal evolving priorities and cost considerations, beneficiaries may need to carefully evaluate their options to maximize value. Insurers could also benefit from reassessing low-prevalence offerings to better align with emerging consumer demands and ensure sustainability in the dynamic Medicare Advantage landscape.