2025 AEP Insight: General Overview of Cost factors📊

2025 Medicare Advantage Trends: Navigating Rising Deductibles and Strategic Premium Shifts

November 7, 2024 Market Research

Table of Contents

General Overview of Cost factors:

2025: Rising deductibles, stable MOOP, and strategic premium shifts shape the healthcare landscape

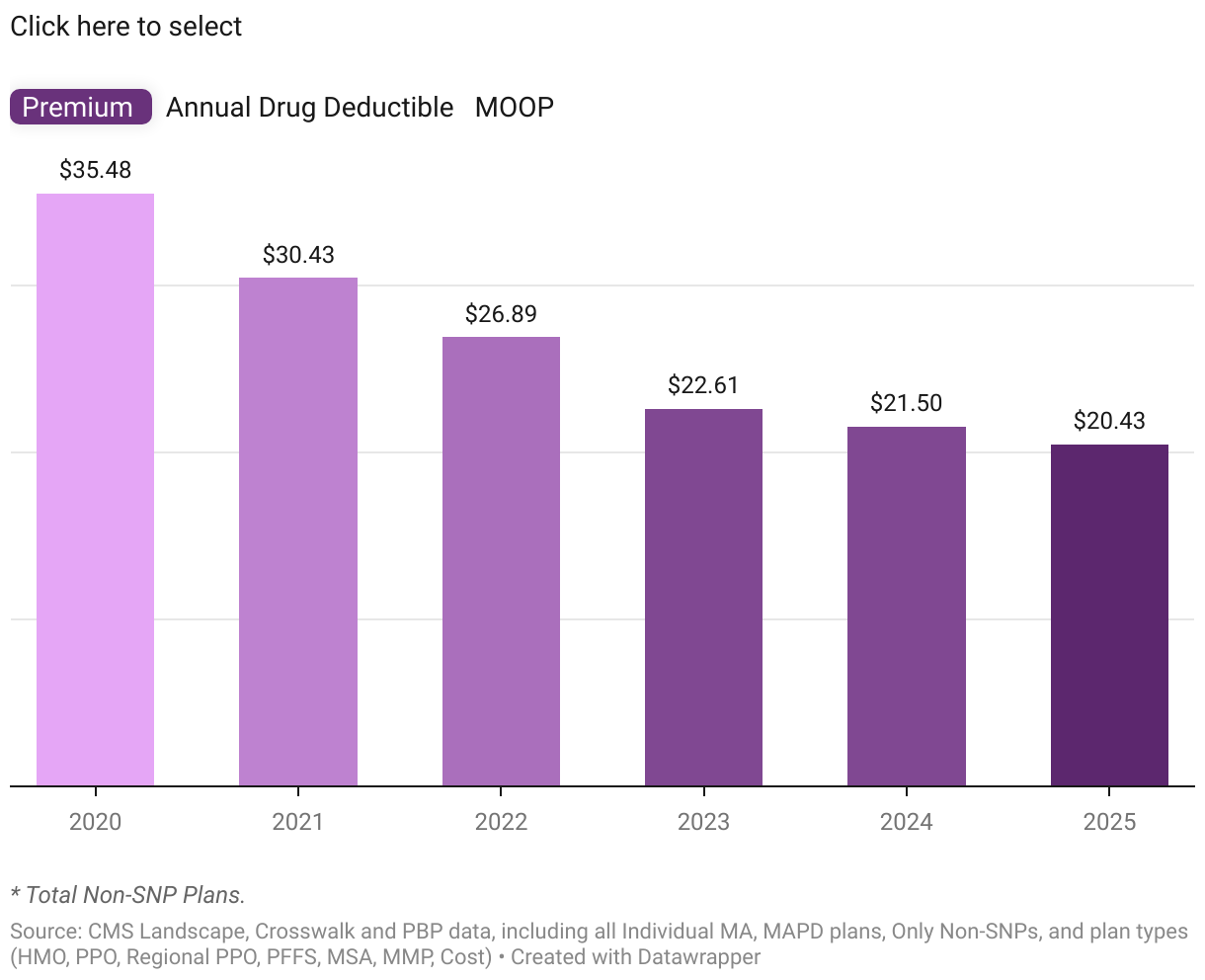

In 2025, the average monthly consolidated premium further decreased to $20.43, marking a steady, though reduced, rate of decline at 5% Year-over-Year (YoY), while the maximum premium rose from $327 to $353. Despite consistent decreases in prior years, the average annual drug deductible saw a dramatic increase, soaring to $248, reflecting a 152.3% YoY rise. This increase was accompanied by a significant jump in the maximum annual drug deductible, reaching $590, the largest annual increase of $45 since 2020.

The average MOOP amount experienced a modest rise to $5,377.30, a 6.4% YoY increase over 2024, indicating that while MOOP remains stable compared to prior years. The maximum MOOP, however, continued its upward trajectory, reaching $9,350, with incremental annual increases since 2020.

Segmentation of Cost factors:

a. Premium

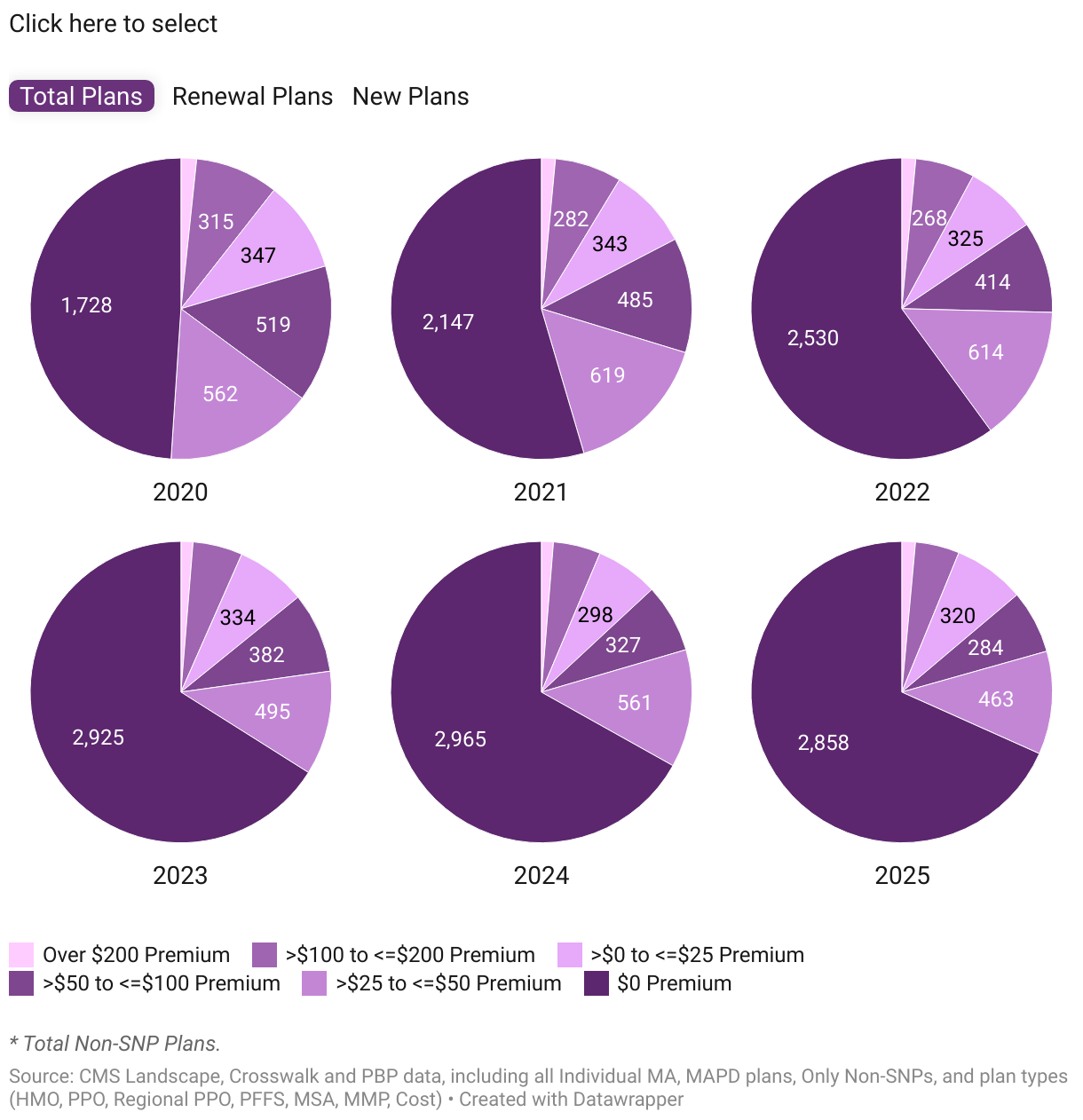

The number of plans in the $0 premium is fewer by 107 in 2025, while the non-zero premium plans are less by 142 plans compared to 2024.

The data reveals a concentrated shift in plan premium structures, particularly across new, renewal, and total plan segments. Dominating the market at around 68% of total Non-SNPs, $0 premium plans saw a slight overall decline of 3.6% YoY (from 2,965 to 2,858), mainly due to a 4.9% decrease in renewals, though new $0 premium plans increased by 6.1% YoY. Meanwhile, plans in the >$0 to <=$25 segment gained renewed traction, with total and renewal categories rising by 7.4% and 9.1% YoY, respectively, highlighting payors’ emphasis on affordability to drive both retention and acquisition.

Mid-tier premium plans (>$25 to <=$100), which make up about 11% in the $25-$50 range and 7% in the $50-$100 range, experienced declines across renewals and slight rise in new plans. Renewal plans dropped significantly from 808 to 660, and new plans increased from 80 to 87, signalling a possible strategic shift away from mid-premium options in favour of low- or high-premium alternatives. At the high end, plans exceeding $200 grew by 7% YoY in 2025, with renewal plans reducing by eight but new plans adding twelve, as compared to none in 2024, suggesting targeted demand for higher-tier coverage offerings.

b. HMO and PPO Deep Dive

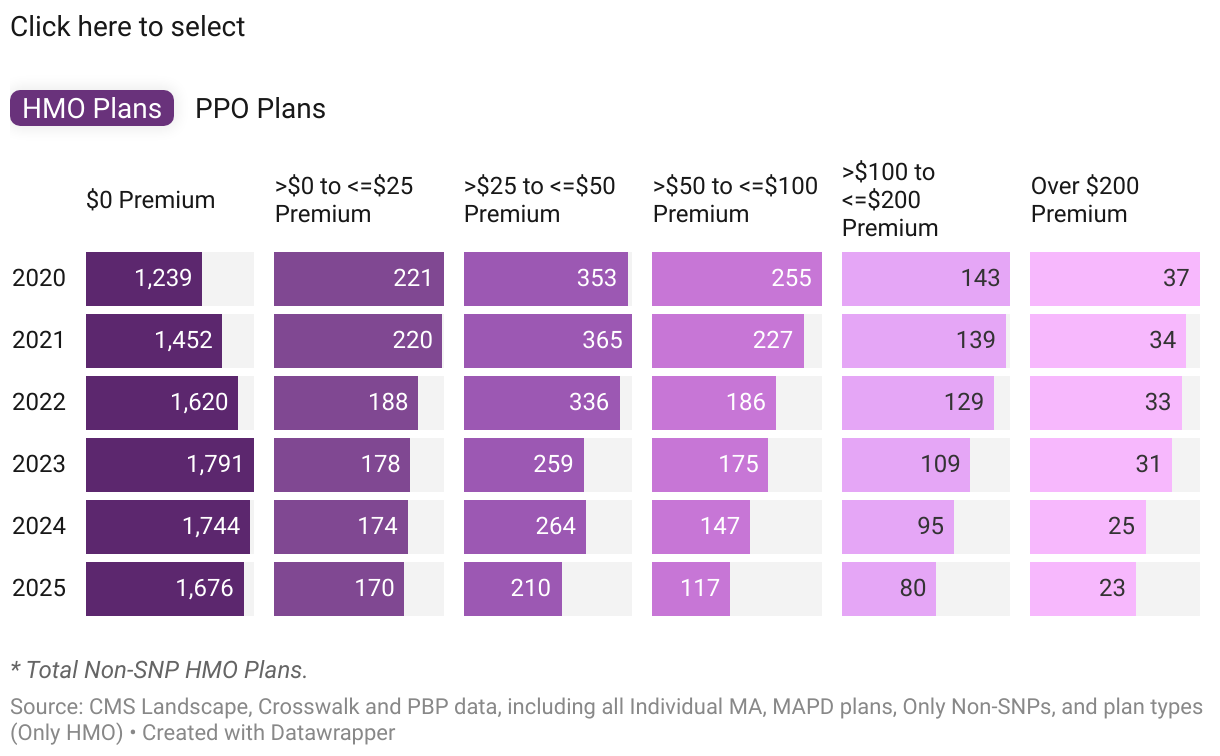

Both HMO and PPO plans saw a decline across all segments, apart from growth in >$0 & <=$25 and >$200 premium categories only in PPO.

The comparison between HMO and PPO plan trends reveals contrasting movements in their premium categories. Zero-premium plans constituted approximately 74% of HMO plans and 64% of PPO plans. For HMO plans, those in the >$0 to <=$25 range experienced a slight reduction of 4 plans, indicating a consistent downward trend. In contrast, PPO plans in this category increased from 121 to 144 plans. The >$25 to <=$50 premium category saw a significant decline, with HMO plans marking a 20.5% YoY drop compared to a 14.2% YoY decline in PPO plans, suggesting a retreat from mid-tier offerings.

Plans in the >$50 to <=$100 premium range showed a reduction of 30 plans in HMO and one plan in PPO compared to 2024. The >$100 to <=$200 segment fell to 80 plans in HMO, representing a 16% YoY decrease, while PPO plans in this category decreased to 86 plans, reflecting a 7% YoY drop. Plans exceeding $200 experienced a minor reduction in HMO, decreasing to 23 plans, while PPO plans saw a slight increase of one plan. Overall, PPO plans highlight a shift towards affordability, particularly in lower premium categories, while HMO plans exhibit a declining trend across various premium ranges, especially in mid-tier options.

c. Drug Deductible

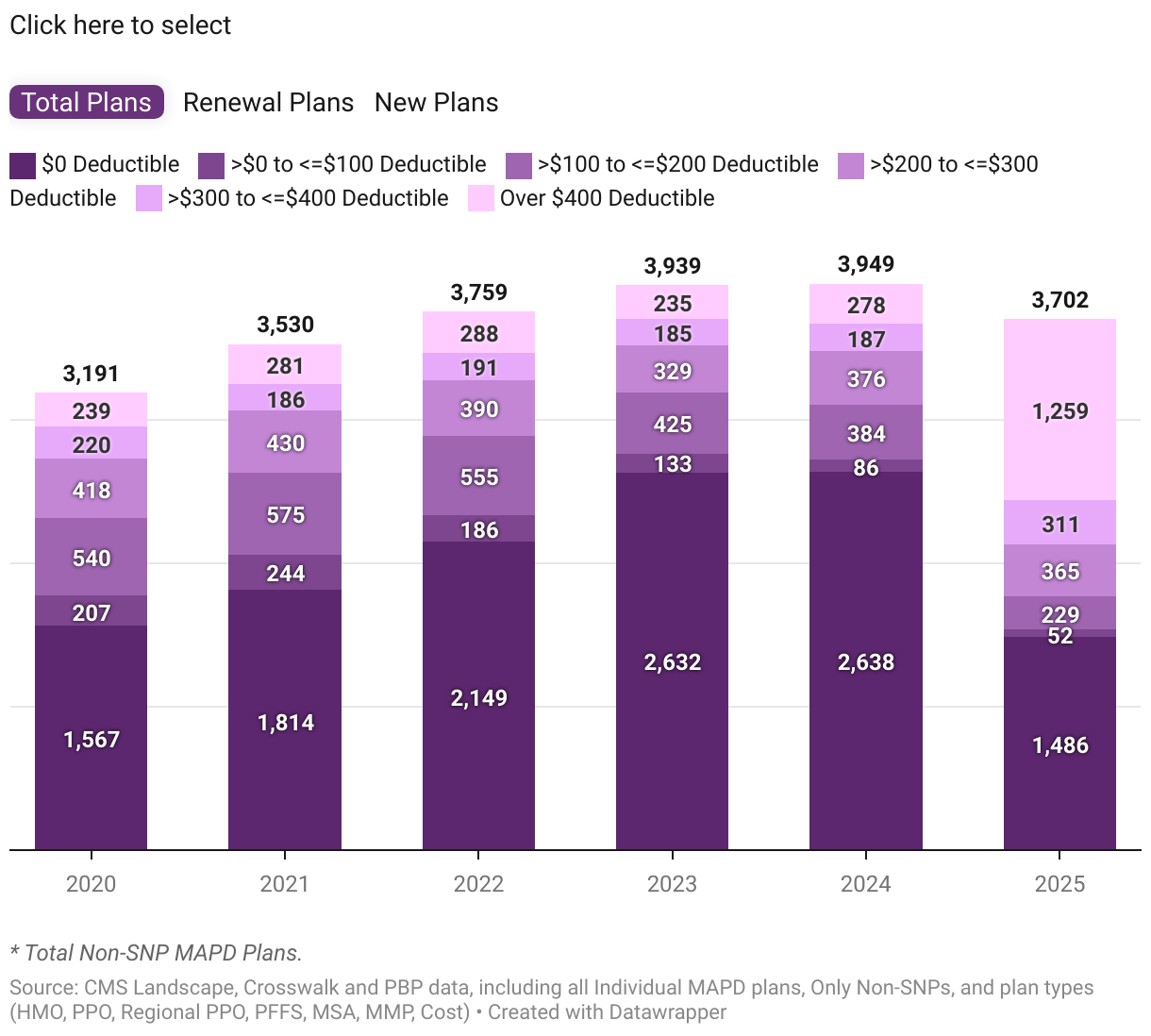

A decline in zero-drug deductible plans (40%) amidst a surge in high deductible plans (34%)

The deductible segmentation data for 2024 and 2025 highlights a significant transformation in plan availability and market percentages. Notably, zero-drug deductible plans have plummeted from 66.8% to 40.1% of total MAPD Non-SNP plans available in 2025. Similarly, the >$0 to <=$100 deductible category decreased from 2.2% to 1.4%, while the >$100 to <=$200 deductible category saw a decline from 384 to 229 plans, resulting in a percentage drop from 9.7% to 6.2%. In contrast, the >$300 to <=$400 deductible category increased its market share from 4.7% to 8.4%, and the Over $400 deductible category saw an extraordinary shift in market share, rising from 7% to 34%.

The trend is stark, with the total number of plans from $0 to $300 drug deductible declining in 2025, while plans over $300 surged dramatically from 465 to 1,570. In the new plans segment, most categories showed a decline, except for the >$400 deductible segment, which increased from 80 to 269, and the >$100 to <=$200 segment, which added three new plans for a total of 20 in 2025. The overall number of $0 deductible plans has dropped significantly from 2,638 in 2024 to 1,486 in 2025, marking a 43.7% YoY decrease. This trend is echoed by a significant reduction in renewal plans, which fell from 2,369 to 1,351, and new plans from 269 to 135. This indicates a shrinking availability of low-deductible options, although insurers are trying to maintain a baseline of offerings in this category.

Conversely, high-deductible plans are witnessing a substantial resurgence. The total plans in the Over $400 deductible category skyrocketed from 278 to 1,259, reflecting a staggering 352.9% YoY increase, with new plans increasing from 37 to 246. Renewal plans in this category also rose significantly from 241 to 1,013, underscoring a shift in both the introduction and retention of high-deductible plans.

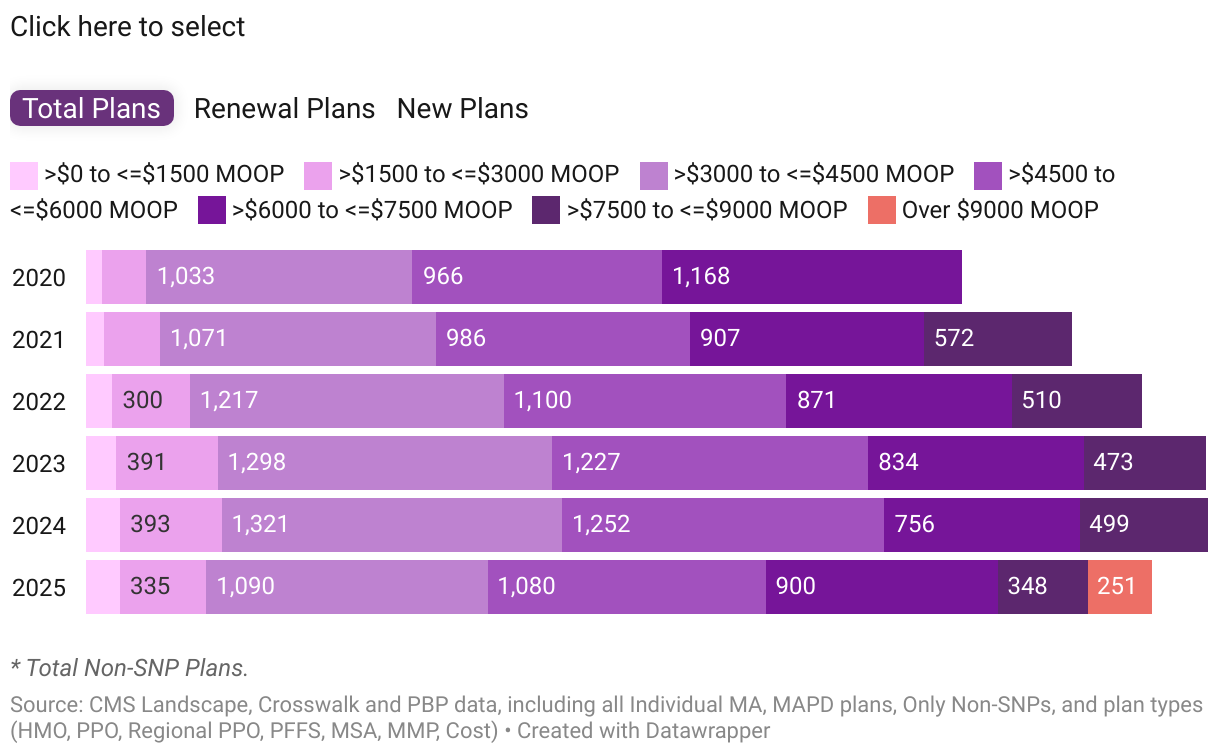

d. MOOP

For the first time in recent years, 251 plans (6% of total Non-SNPs) now have a MOOP exceeding $9,000.

The 2025 MOOP data for Non-SNP plans shows a shift towards higher out-of-pocket limits, with approximately 74% of plans now in the $3,000 to $7,500 range and around 14.5% exceeding $7,500. Plan counts fell across all the segments compared to 2024, except in the >$6000 to <=$7500 category. The lowest MOOP segment (>$0 to <=$1500) saw slight declines in total and renewal plans by 0.7% and 2.7% YoY, respectively, while new plans grew modestly by 8.3% YoY, indicating limited growth for low-MOOP options.

In the mid-range, particularly in the >$1500 to <=$3000 bucket, total and renewal plans grew until 2024 but dropped from 393 to 335 total plans in 2025, with volatility in new plans that otherwise maintained a steady presence. The >$3000 to <=$4500 category, once growing robustly, saw notable drops in 2025, with total plans down by 17.5% YoY, renewal plans by 192, and new plans by 39, marking a pullback from mid-MOOP offerings.

Higher MOOP categories show a contrasting trend, particularly the >$6000 to <=$7500 range reversed its earlier downward trend with total plans rising 19% YoY and an increase of 108 renewal plans compared to the previous year. New plans in this category also grew significantly, jumping from 83 to 119. The >$7500 to <=$9000 MOOP segment, however, experienced significant declines in 2025, with total plans down by 30.3% YoY, reflecting a declining market interest in this specific high-MOOP range, while new plans, though fewer, showed a slight increase.

Overall, the data reflects a shifting trend away from lower and mid-range MOOP plans in favour of high-MOOP options, particularly above $6000, where growth is seen both in total, renewal, and new plans. This could indicate changing consumer preferences or insurers offering fewer low-MOOP options while strengthening higher-MOOP plan offerings, especially for new plans.