A new era for Medicare Advantage: Consolidation and strategic shifts in 2025

October 21, 2024

Market Research

Table of Contents

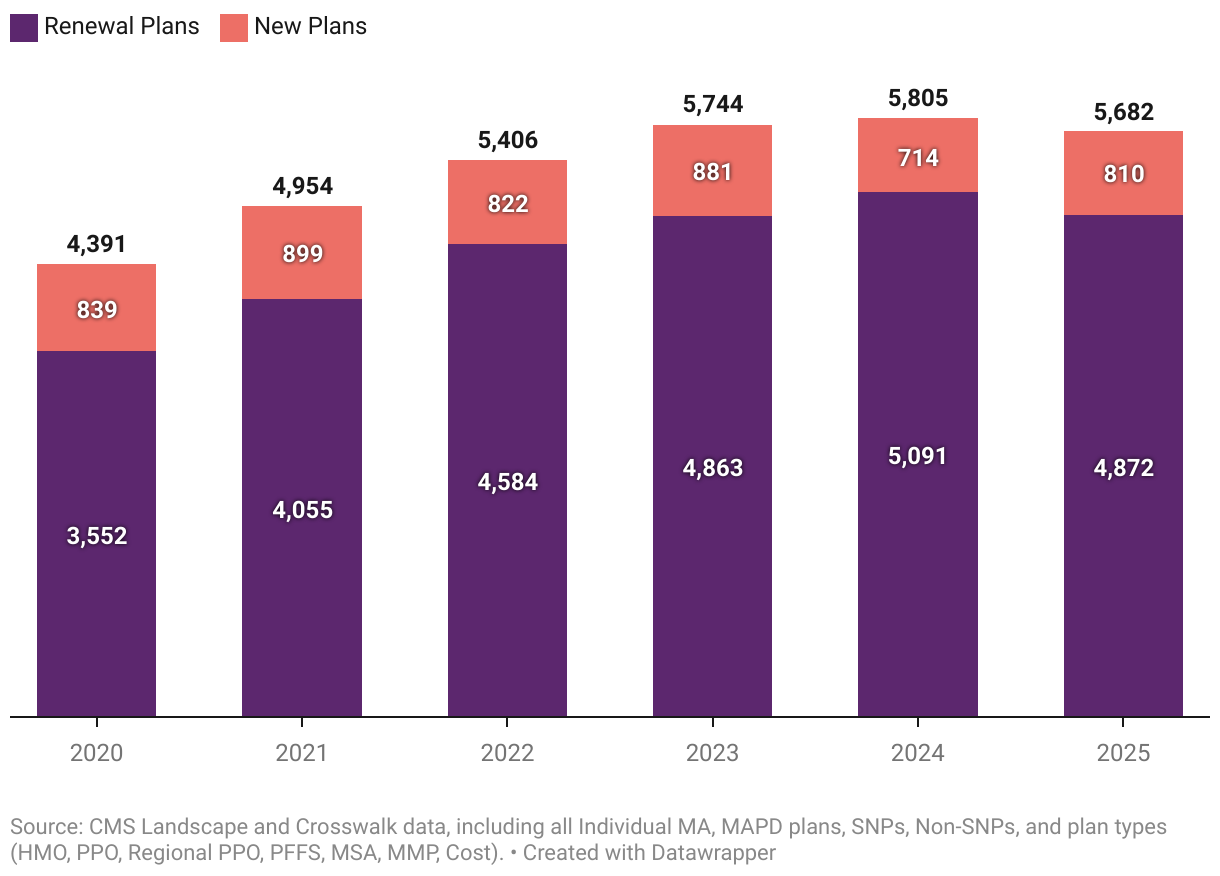

First-ever shift: Medicare Advantage plan count reduces from 5,805 to 5,682 in 2025

The past trend from 2019 reveals a clear deceleration in the growth of plans, shifting from a period of rapid expansion to a slight contraction. Growth rate over the years peaked at 17.1% in 2019, but progressively slowed—15.0% in 2020, 12.8% in 2021, 9.1% in 2022, and 6.3% in 2023. By 2024, growth was minimal at 1.1% Year-over-Year (YoY), indicating market saturation.

In 2025, the market contracted by -2.1% YoY, the first decline in Medicare industry. This suggests a period of consolidation, from growth to a slight decrease may reflect changing market dynamics, where innovation has plateaued, or there has been a refocus on enhancing existing plans.

Note:

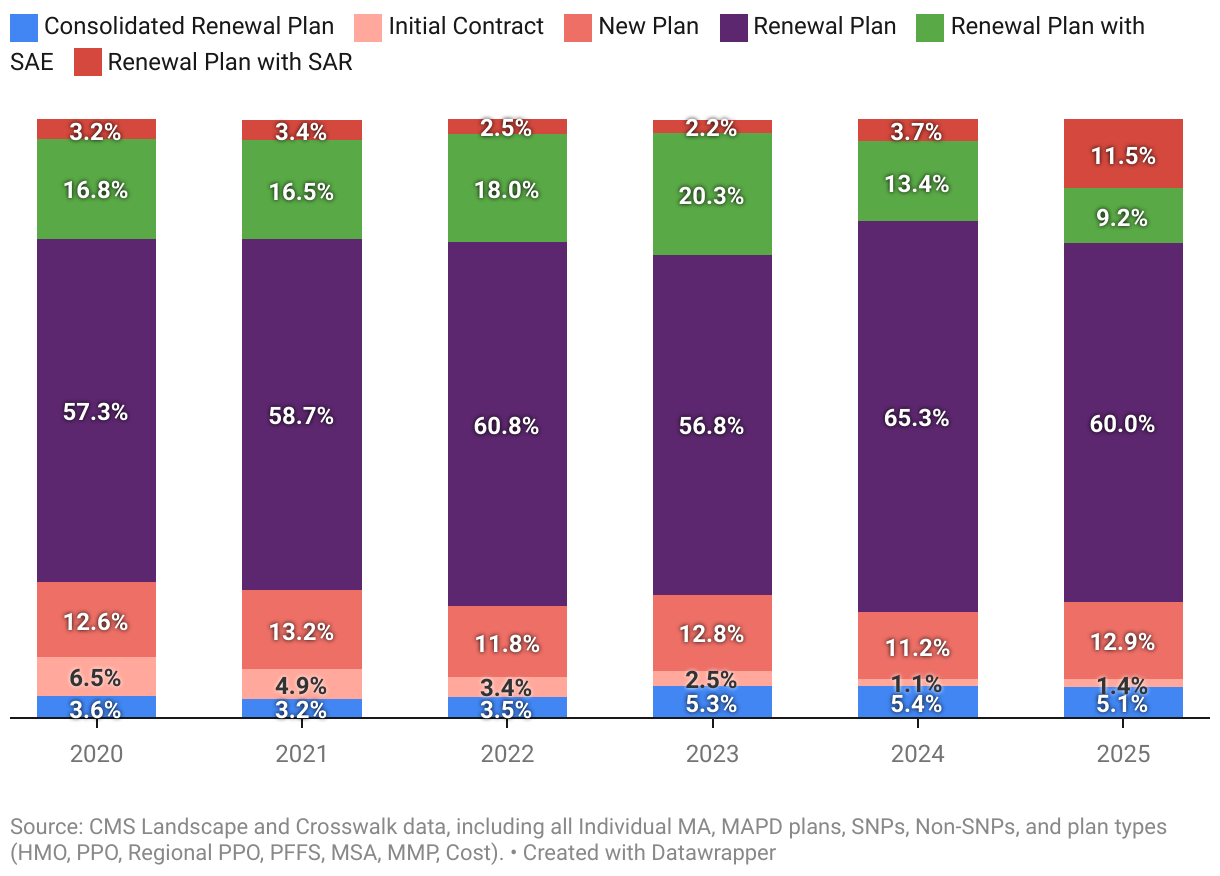

The total number of plans is divided into several categories, which include Renewal Plans, Consolidated Renewal Plans, Renewal Plans with Service Area Expansion (SAE), Renewal Plans with Service Area Reduction (SAR), Initial Contracts, and New Plans.

Categories of plans will be represented in italics (e.g.: Consolidated Renewal Plans, New Plans).

New Plans (without italics or capitalization) indicate both New Plans and Initial Contracts. Renewal Plans is combination of Renewal Plans, Consolidated Renewal Plans, Renewal Plans with SAR and Renewal Plans with SAE.

The surge in Renewal Plans with SAR catalyzed industry contraction, with the plan count tripling in 2025 compared to 2024.

In 2025, the Medicare landscape saw a significant shift, with Renewal Plans with SAR tripling their count to 651 from just 214 in 2024 impacting around 1.9 million lives. This sharp rise stands out to be one of the reasons for industry-wide contraction, where the remaining renewal plan categories saw a reduction. Notably, the total number of new plans increased from 714 to 810, marking a 13% YoY rise, a reversal after the previous year’ 19% decline. At the same time, renewal plans fell from 5,091 to 4,872, underscoring the reshaping of the Medicare market. While new plans made a modest comeback, the SAR category’s explosive growth stands out against an overall industry slowdown.

Breaking down the plan categories for 2025, Renewal Plans continue to dominate with around 60% of the total share, though this is a slight decline from 2024’s 65%. Historically, Renewal Plans with SAE held the second-largest share, but in 2025, New Plans have taken this spot, comprising approximately 13% of the total. Following closely behind are Renewal Plans with SAR, which surged to 11.5%, a significant rise from just 3.7% in 2024. Meanwhile, Renewal Plans with SAE have been steadily decreasing—dropping from 20% in 2023 to 13% in 2024, and now only accounting for 9% in 2025.

Let us show you how HealthWorksAI can optimize your Medicare Advantage product design efforts at every stage through actionable insights by leveraging public and private healthcare data.