2024 AEP Insight Series: Report 6 📊

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits

November 03, 2023 Market Research

Premium cost is a critical factor for beneficiaries when selecting a Medicare Advantage (MA) plan, as it directly impacts their expenses and benefits. In this article, we will deep dive into the various premium segments, categorizing them based on premium ranges such as $0, >$0 to <=$20, >$20 to <=$40, and so on. From zero-premium to higher premium tiers, we aim to provide insights into how these premiums relate to the inclusion of Supplemental and Enhanced benefits and provide insights into the various patterns across these categories. Our analysis is based on data released from CMS, specifically the Landscape, Crosswalk, and PBP files, and is exclusively centered only on total Non-SNP plans.

Supplemental Benefits:

Note: The below sections include benefits with more than 30% inclusion in 2024. Psychiatry, Skilled Nursing Facility (SNF), Chiropractor, and Cardiac benefits are excluded.

Zero-Premium Segment

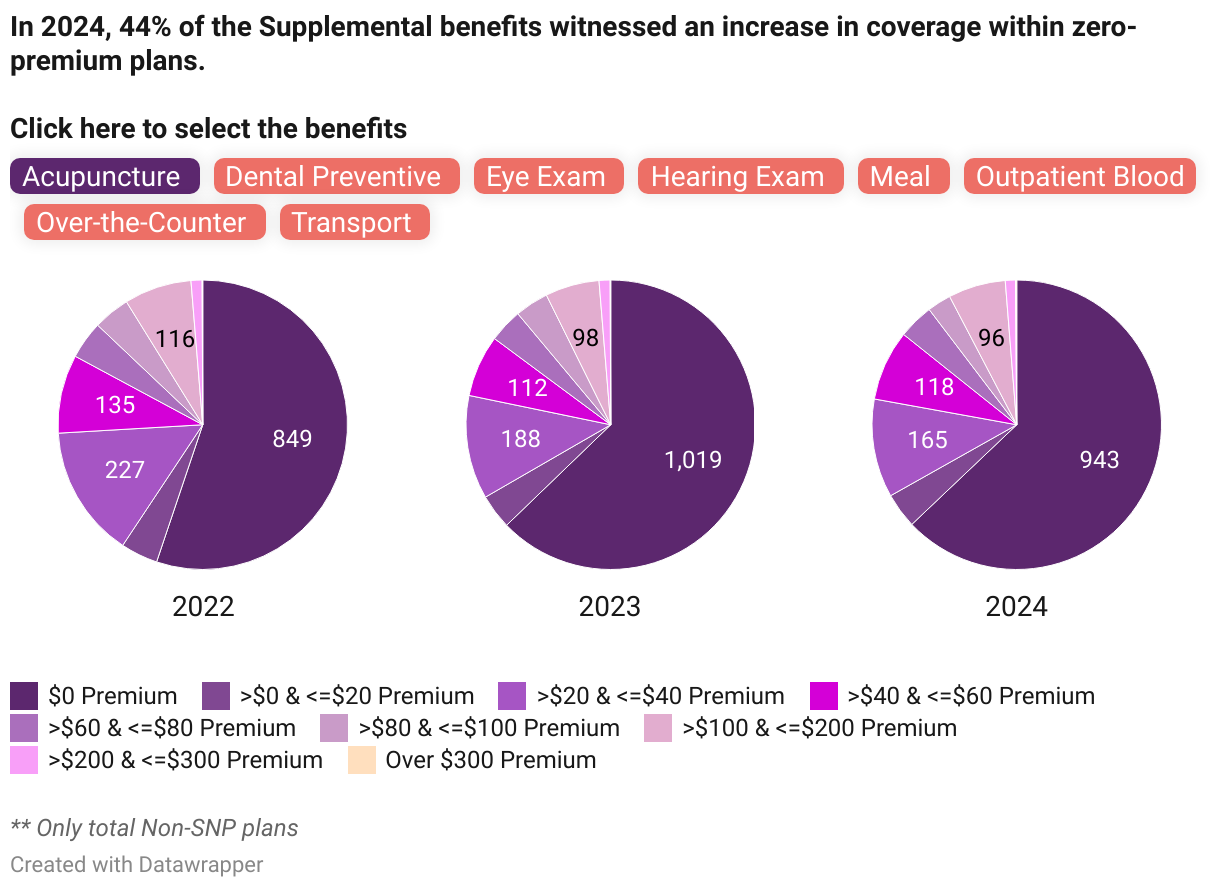

More than 95% of the 2,961 zero-premium plans in the market provide Supplemental benefits like Eye Exam, Emergency, Dental Preventive, Hearing Exams, Eye Wear, Hearing Aids, and Outpatient Blood. While the percentage of plans providing Supplemental benefits has steadily increased over time, it began to fall in 2024 for 56% of the benefits, most notably for Transportation, which saw a drop from 45% to 38%.

Furthermore, Acupuncture, Podiatry, and Over-The-Counter (OTC) also noticed a decreasing trend in terms of plan count by 76, 73, and 42 plans, respectively. Conversely, some benefits did see an uptick, such as Physical Exams (+73), Eye Wear (+65), and Hearing Aids (+56), but their growth remained modest, with each showing an increase of less than 4% Year-over-Year (YoY), underscoring a cautious approach by Payors. Despite being an essential benefit, Dental Comprehensive has remained unchanged.

Low-Premium Segment

Segments with premiums falling within the ranges of >$0 & <=$20 and >$20 & <=$40 are categorized as low-premium segments. Interestingly, an erratic trend was observed in the >$0 to <=$20 segment, with an increase in offering all Supplemental benefits except for Acupuncture in 2023, followed by a reverse trend in 2024, resulting in a decline. In contrast to the >$0 to <=$20 segment, the >$20 & <=$40 exhibited a decrease in coverage in 2023 and increased in 2024, apart from Transport, which lost 24 plans.

While the market saw a substantial downfall in the percentage of Transportation benefits offered in both segments, Meals noticed a decline from 78% to 73% in the >$0 & <=$20 segment and witnessed a slight increase of less than one percent in the >$20 & <=$40 segment.

The >$0 & <=$20 segment showed a distinct pattern as there was a decline in many Supplemental benefits offered in 2022, but in 2023, they made a strong comeback, only to face another substantial decline in 2024. Specifically, OTC and Outpatient blood saw reductions in offerings, losing 26 and 37 plans, respectively, in 2022, followed by additions of 38 and 33 plans in 2023, each again declining at the rate of 24% YoY in the next year.

Mid-Premium Segment

Mid-premium segments encompass premium ranges from >$40 to <=$60, >$60 to <=$80, and >$80 to <=$100. In these categories, a trend is observed that as the premiums increase, the number of plans providing Supplemental benefits decreases.

Within the >$40 to <=$60 category, there was a decline in the number of plans offering Supplemental benefits except for Transport and Podiatry in 2023. However, in 2024, these plans made a significant comeback, especially in Hearing Care, which saw a remarkable recovery by adding 29 plans, marking a 13% YoY increase. This was followed by Eye Wear, which increased from 224 to 249 plans, and Emergency benefits, which grew in coverage at the rate of 10% annually.

Conversely, both the >$60 to <=$80 and >$80 to <=$100 categories witnessed a reduction in plans offering all Supplemental benefits, majorly in Dental Comprehensive by 17 and 42 plans, respectively. Under the >$60 to <=$80 segment, the rate of decline varies, ranging from 9% YoY in Meal to 1.5% YoY in Eye Exams, with the remaining benefits falling within this range. However, in the >$80 to <=$100 segment, coverage of Emergency, Eye Exam, Physical Exam, Hearing Exam, and Outpatient Blood benefits have seen an equal loss of 36 plans each.

High-Premium Segment

Premium ranges >$100 to <=$200, >$200 to <=$300, and over $300 are included in this section. The >$100 to <=$200 segment comprises a higher number of plans in comparison to >$60 to <=$100 segment, while >$200 premium segments have the lowest plan count offering various Supplemental benefits.

Under the >$100 to <=$200 segment, there was a decline in the number of plans that offered Supplemental benefits over the years. However, a different pattern emerged for the Meal benefit, consistently increasing until 2022. Notably, in 2023, there was a significant decline of 15% YoY, but in 2024, there was a recovery by adding 14 plans. On the other hand, OTC offerings increased over the years but experienced a decrease for the first time in 2024, with a reduction of one plan.

In the >$200 & <=$300 premium category, there was a minor decrease in the number of plans offering benefits such as Hearing Exam, Physical Exam, Acupuncture, Transportation, Eye Wear, and Dental Care. However, the remaining benefits saw an increase of two to three plans. Meanwhile, in the premium category exceeding $300, most plans offering Supplemental benefits remained consistent.

Enhanced Benefits:

Note: Evaluated Enhanced benefits with coverage exceeding or around 20% in total Non-SNP plans. The mainly discussed benefits are Fitness, Remote Access Technologies, Nutritional and Dietary benefits, Additional Sessions of Smoking and Tobacco Cessation Counselling, Bathroom Safety Devices, Personal Emergency Response System (PERS), and Health Education.

Zero-Premium Segment

In 2024, among total zero-premium plans, 97.8% include Fitness, and 73.9% offer Remote Access Technology benefits, although this is slightly less than in 2023. However, the number of plans has increased slightly in both benefits. On the other hand, Additional Sessions of Smoking and Tobacco Cessation Counselling, Nutritional/Dietary Benefits, and PERS have seen a reduction in both benefit coverage percentage and the number of plans, with YoY declines of 2.6%, 1.5%, and 11.2%, respectively.

On the contrary, Health Education covers 40% of total zero-premium plans, with an additional 69 plans totaling 1,193. Bathroom Safety Device benefits have grown significantly, offered by 305 plans in 2023 and increasing to 676 plans in 2024.

Low-Premium Segment

In the realm of premium levels, there was a decline in plan count within the >$0 to <=$20 premium segment except in the Health Education (+24) and Bathroom Safety device (+19) benefits, whereas the opposite trend occurred in the >$20 to <=$40 segment, apart from the PERS benefit declined at 4.8% YoY. The number of plans falling into the >$20 to <=$40 segment exceeded those in the >$0 to <=$20 premium segment.

Looking at plan count, Fitness, Remote Access Technology, Additional Sessions of Smoking and Tobacco Cessation Counselling, and Nutritional/Dietary Benefits witnessed an increase in plan offerings under the >$20 to <=$40 segment, with 40, 57, 46, and 43 plans added, respectively. Concurrently, there was a decrease in the >$0 to <=$20 premium segment, with a loss of 41, 33, 18, and 19 plans for the same benefits.

Mid-Premium Segment

In the context of premium segments, the number of plans offered in the low-premium segment is more than those in the mid-premium segment. However, several benefits, such as Additional Sessions of Smoking and Tobacco Cessation Counselling, Nutritional/Dietary Benefits, Remote Access Technology, and Health Education, have witnessed a yearly decline in coverage across all mid-premium segments, with rates of 22%, 20%, 9%, and 12% YoY, respectively.

The Fitness benefit shows an interesting pattern as it has increased the availability of plans in the >$40 & <=$60 segment, going from 233 to 251, while experiencing a collective drop in the other two segments, decreasing from 266 to 215 plans. Notably, Bathroom Safety Devices have seen an increase in the >$40 & <=$60 segment (+36 plans in 2024) and the >$80 & <=$100 segments (+3 plans), while the >$60 & <=$80 premium segment has the same number of plans as in 2023.

On the other hand, PERS benefits exhibit varying patterns among mid-premium segments. The >$40 & <=$60 segment has added a single plan, the >$60 & <=$80 segment remains unchanged, and the >$80 & <=$100 segment has noticed a modest decline.

High-Premium Segment

Within the plans offering the above-discussed benefits in the market, the >$100 & <=$200 premium segment constitutes more plans offering these benefits than the >$200 & <=$300 segment. Notably, Nutritional/Dietary Benefits, Bathroom Safety Devices, and PERS benefits have no plans offered in the over $300 premium segment, with other benefits having one or two plans in this segment. Fitness, Additional Sessions of Smoking and Tobacco Cessation Counselling, and Health Education benefits under the >$100 & <=$300 segments observed a minimal decline.

Remote Access Technologies have seen a decrease in the percentage offering the benefit in the >$100 & <=$200 segment by losing 12 plans, while the >$200 & <=$300 segment currently has 47 plans, which has been constant since 2022. Bathroom Safety Devices and Nutritional/Dietary Benefits follow similar patterns in offering the plans with a small rise in the >$100 & <=$200 segment and down by unit plan in the >$200 & <=$300 segment.

Conclusion:

In summary, this analysis has shed light on the relationship between premium categories and the availability of Supplemental and Enhanced benefits within Medicare Advantage plans. The zero-premium segment stands out for its diverse range of Supplemental benefits, while the mid-premium and high-premium segments offer more limited selections. Additionally, Enhanced benefits vary across different premium categories, with some benefits seeing growth and others experiencing declines. Understanding these patterns can help beneficiaries make informed decisions when choosing their Medicare Advantage plans, ensuring they align with their healthcare needs and financial considerations.

Stay tuned for more 2024 AEP Insights from HealthWorksAI!

Read More about AEP Insights

-

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research -

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research -

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research -

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research -

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research