2024 AEP Insight Series: Report 8 📊

Navigating the (MA) Stars: Trends of the 2024 Ratings

November 30, 2023 Market Research

Medicare Advantage plans in the United States are subject to star ratings ranging from 1 to 5 stars assigned by the Centers for Medicare & Medicaid Services (CMS), reflecting the plan’s quality and performance. These ratings, evaluating factors such as customer satisfaction and preventive services, facilitate informed healthcare decisions for consumers. Higher star ratings signify superior quality, empowering patients, and their families to make well-informed choices about their healthcare coverage.

Our exploration delves into the overall landscape, examining both Non-Special Needs Plan type (SNP) and SNP plans (including Dual Eligible Special Needs Plan, Chronic Special Needs Plan, and Institutional Special Needs Plan types) with a specific focus on Non-SNP HMO and PPO plans, utilizing data released by CMS in October 2023, including the Landscape, Crosswalk, and Star rating data sets.

National Overview of Stars:

At the national level, approximately 55% of all plans hold a star rating of 4 or above, with a distribution of 28% at 4★, 20% at 4.5★, and 7% at 5★. While the number of plans with a 4★ rating increased from the previous year, those with a 4.5★ rating remained consistent, and the count of 5★ rated plans decreased.

For SNP plans, the number of 4★ rated plans remained consistent with the previous year, adding two more plans in 2024. Meanwhile, there was an increase in 5★ from 135 to 165 plans, mainly attributed to the Chronic Special Needs Plan type. However, a minimal rise was observed in 3.5★ ratings, increasing from 11.5% to 16.5%. In contrast, 4.5★ saw a dip from 17% to 13%.

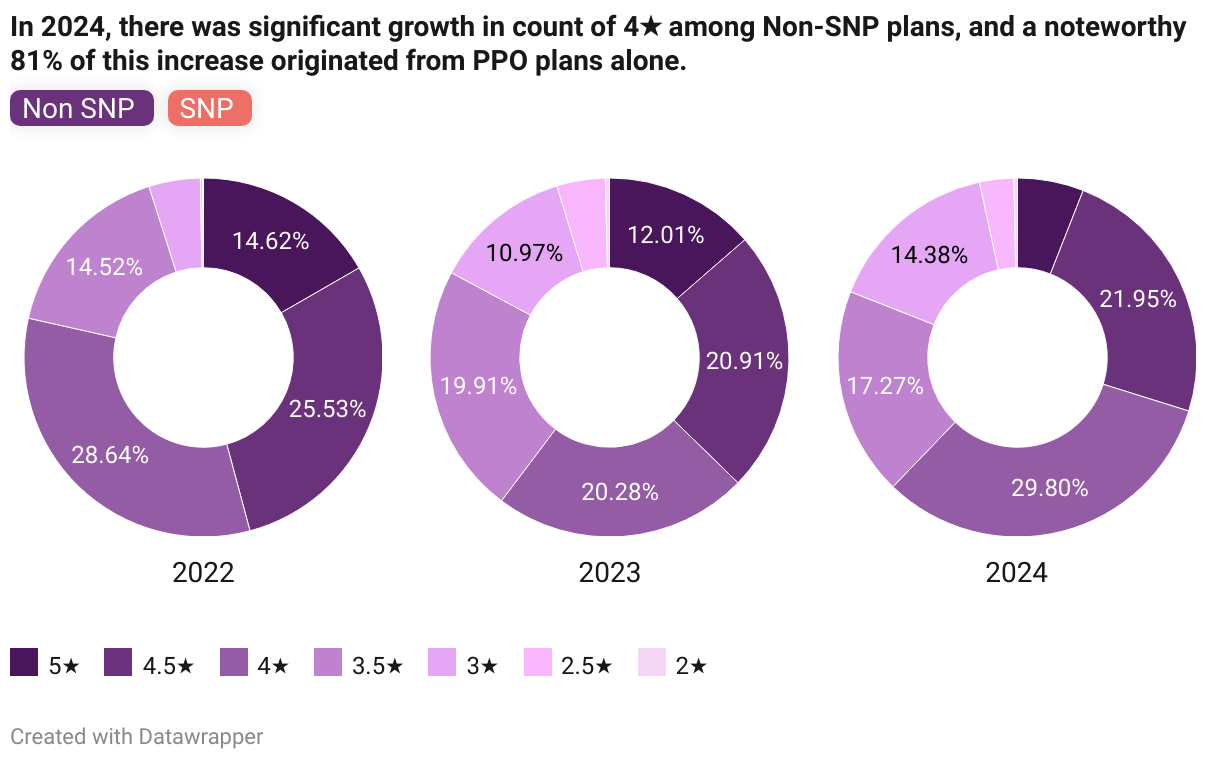

Turning the focus to Non-SNP plans, there was an uptick in 4★, rising from 898 to an impressive 1,320 plans, and a moderate increase in 4.5★, growing from 926 to 972 plans. Conversely, the prevalence of 5★ experienced a decline, dropping from 12% in 2023 to 5.5% the next year.

Exploring Non-SNP HMO plans has shown an upward trend in all the star categories, except for 2.5 and 5★ ratings. Notably, the highest number of HMO plans achieved a 4★ rating, increasing from 588 now to 657 in 2024. On the other hand, under the 4★ rating for PPO plans, the count declined from 543 in 2022 to 261, only to rebound in 2024 at the rate of 131% Year-over-Year (YoY), representing 33% of all PPO plans. However, 5★ rated PPO plans experienced a substantial drop, falling to 23 plans in 2024 from 119.

In a massive shift, CVS Health Corporation has seen a dramatic rebound in ratings. After having 71% of their plans rated 4★ or higher in 2022, this percentage dropped to an astonishing 25% in 2023. However, there was a significant, nearly equal recovery in 2024, with 70% of CVS Health Corporation’s plans once again achieving a 4★ or higher.

Alternatively, UnitedHealth Group, Inc. and Humana Inc. saw a decrease in the number of plans with bonus eligible ratings (4 or more stars), with 67% and 92% of their plans, respectively. Despite being a prominent Payor, only 1.24% of plans offered by Centene Corporation qualify, the lowest among its peers. In contrast, every plan provided by Highmark Health received a 4★ or higher rating in 2024. Lastly, although all plans from Kaiser Foundation Health Plan, Inc. were bonus-eligible in 2022 and 2023, the percentage dropped to 55% in 2024.

Also Read – Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans

Sustainability and Variations of Stars:

The sustainability of stars, denoting consistent star ratings from one year to the next, is key in evaluating plan performance. Variations observed may be that plans have improved from smaller ratings to higher or vice-versa is discussed in detail in this section through various segments.

In 2024, approximately 58% of plans that held a 4★ rating in 2023 either maintained the same rating or achieved a higher status, which is down from 68% observed in the previous year. Similarly, 92% of 4.5★ plans and 97% of 5★ plans successfully retained a star rating of 4★ and beyond in 2024.

4-star

A yearly analysis at the national level shows that 48% of plans holding a 4★ in 2023 maintained the same rating in 2024, with an additional 10% experiencing an increase beyond 4★. In comparison to this, 44% of plans sustained their ratings from 2022 to 2023, while 24% saw an improvement from a 4★ to 4.5★ in 2023.

In the case of Non-SNP plans, the retention percentages align with the national trend as discussed in the above paragraph, whereas SNP plans retained approximately 55% of 4★ plans from 2023 to the next year, showing a slight increase from the previous year’s 51%. Notably, the number of plans dropping below 4★ amounted to 425 in 2024, compared to 404 plans in 2023.

In 2024, nearly 47% of 4★ plans among Non-SNP HMOs will witness a downgrade, with sustained plans making up only 44%, a decline from the 57% seen in 2023. Conversely, in PPOs, the retained percentage of plans was higher in 2024 (44%) compared to 2023 (27%). While there was a notable decrease in the transition of 4★ rated plans, with 46% being upgraded in 2023, this figure dropped to 15% in 2024.

From the individual Payor perspective, CVS Health Corporation has seen a remarkable rise of 330 plans in the number of 4★ plans, constituting 61% of their overall plans. Following closely are Humana and Kaiser Foundation Health, each offering around 41% of 4★ plans in their total offerings. In contrast, UnitedHealth Group, Inc., and Elevance Health, Inc. experienced decreases in their 4★ plans, with declines of 46 and 25 plans, respectively.

4.5-star

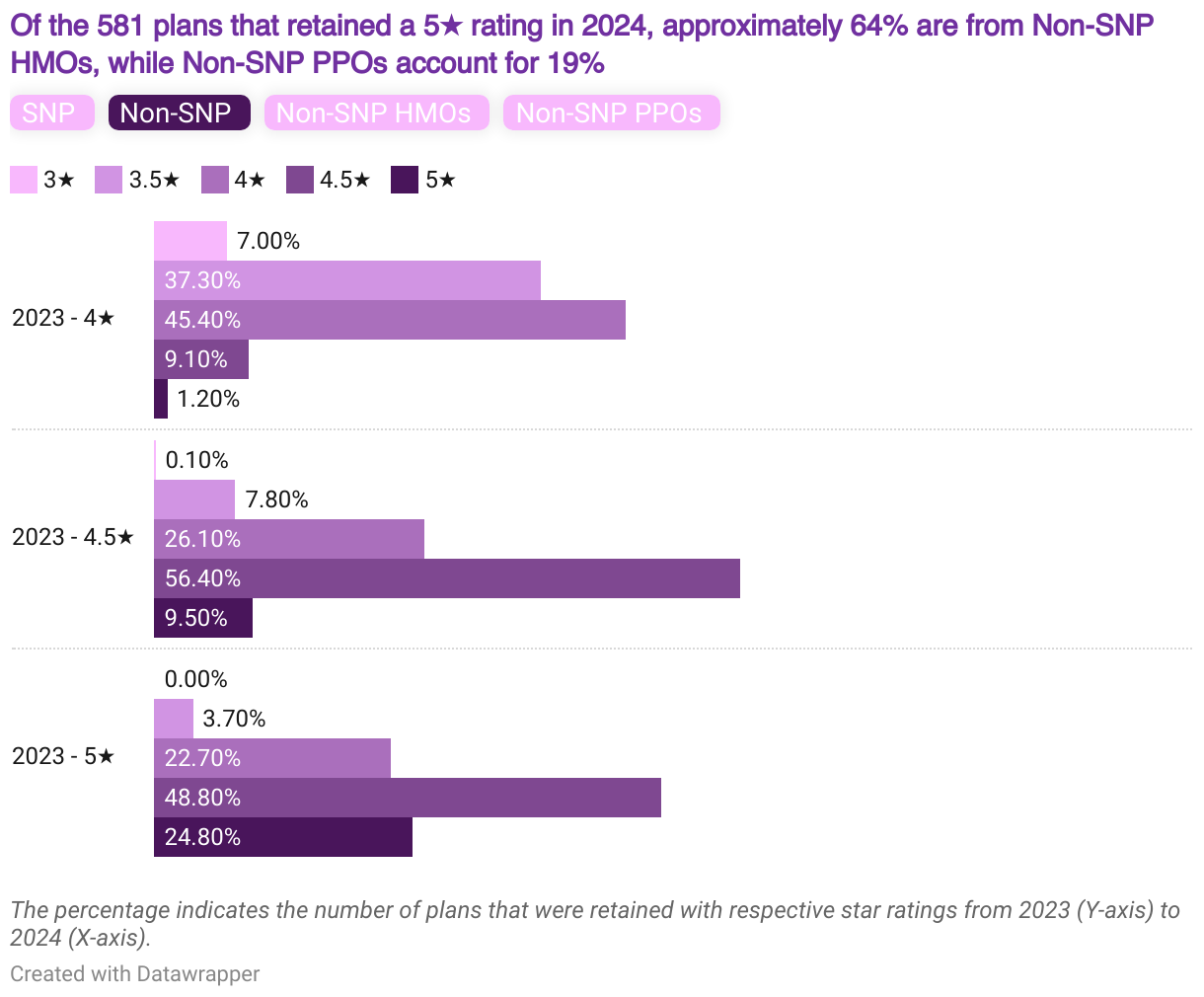

Out of 940 plans that retained a 4★ rating or higher in 2024 previously had 4.5★, among which 554 plans maintained a 4.5★. Of those, 119 (21%) also held the same rating in 2023. Additionally, 13% of 4.5★ plans saw an improvement to 5★ in 2024.

Interestingly, of 4.5★ plans in 2023, around 249 were dropped to 4★ plans in 2024, compared to 297 in 2023. Additionally, plans experiencing a drop from 4.5★ to 3 or 3.5 stars accounted for 8% in 2024, whereas it was 36% in 2023.

On the other hand, Non-SNP plans exhibited an improvement in 2024, with only 8% of 4.5★ plans losing bonus eligibility, a significant drop from the 28% observed in 2023. In SNP, 114 plans have been retained from 2022, while it was 86 plans in 2024. The improvement continued with Non-SNP PPOs, boasting a remarkable 77% sustained rate in 2024, a substantial leap from the mere 17% seen in 2023. Meanwhile, HMOs maintained their 4.5★ in 192 plans during 2024.

Humana Inc. continues to provide a substantial proportion of 4.5★ plans, although there has been a decline of 102 plans in this category. Conversely, UnitedHealth Group, Inc. (218) and CVS Health Corporation (72) have experienced a notable surge in the availability of 4.5★ plans, whereas Centene Corporation has no plans with a 4.5★. Notably, Highmark, which had no plans in 2023, now offers 48 plans, while SCAN Health Plan, which previously had 41 plans rated at 4.5★, now has none.

5-star

In 2023, the sustainability rate for 5★ plans was notably higher compared to 4★ and 4.5★ plans, with 66% of 5★ plans being retained from 2022. However, in 2024, the sustainability rate decreased to 32%, marking lower retention compared to higher star ratings. Plans that transitioned from 5★ to 4.5★ in 2024 amounted to 255, whereas in 2023, it was 168 plans. Furthermore, plans that downgraded from 5★ in 2024 accounted for 23% (4★) and 3% (3.5★).

Around 72% of the 5★ rated Non-SNP plans experienced 4★ or 4.5★ in 2024, while it was 34% in 2023. Under SNP plans, the retention rate was stable at around 63% in both years. Meanwhile, the number of retained plans with 5★ is substantially less in 2024 compared to 2023 in both HMO and PPO plans, currently accounting for 101 and 20, respectively.

In 2024, UnitedHealth Group, Inc., Humana Inc., Elevance Health, Inc., Devoted Health, Inc., and Highmark Health collectively provide 71% of 5★ rated plans. Notably, CVS Health Corporation and Centene, despite being significant Payors, have not had any 5★ plans since 2023. Interestingly, Kaiser Foundation Health (74 plans), which had a high percentage of 5★ plans in 2023, and Cigna Group, with 52 plans, did not retain any 5★ rated plans in 2024.

Conclusion:

This comprehensive analysis reveals intriguing trends in star ratings across different plan types and Payors. The national overview showcases a nuanced distribution of star ratings. The sustainability of star ratings demonstrates variations across different categories, with 4.5★ plans showing remarkable consistency and 4★ plans witnessing a notable surge in 2024. Several factors, such as geographical nuances and strategic shifts among Payors, contribute to this dynamic landscape. In conclusion, the nuanced journey of star ratings in Medicare Advantage plans reflects a complex interplay of quality, performance, and evolving healthcare system.

Stay tuned for more 2024 AEP Insights from HealthWorksAI!

Read More about AEP Insights

-

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research -

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research -

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research -

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research -

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research