2024 AEP Insight Series: Report 3 📊

Medicare Advantage in 2024: A Look at Premiums, Deductibles, and MOOP Offerings

October 13, 2023 Market Research

As with any purchasing decision, cost factors are a major component in the decision-making process of beneficiaries when choosing a plan. Our analysis explores the distribution of Medicare Advantage plans across various premium categories, revealing trends that have unfolded over the years. Notably, it conducts a detailed exploration of HMO and PPO plans, in addition to an analysis of drug deductible and In-Network Maximum Out-of-Pocket (MOOP) segments, shedding light on their changes.

Ultimately, this article serves as a valuable resource for understanding the complex cost elements at the highest level and their impact on the Medicare Advantage (MA) market in 2024, drawing from CMS landscape and crosswalk data, with a focus on Non-Special Needs Plans (Non-SNP) only.

General Overview of Cost factors:

The average monthly consolidated premiums showed a consistent decrease over the years; however, the average premium for the next year resembles the current year at $23, further supporting the conclusion that the market has shifted focus toward stability and conservative growth in 2024.

After observing a continuous decline since 2020 and a significant drop in 2023 ($150 to $132), the average drug deductible rose to $146 in 2024, a 10.3% increase year-over-year (YoY), with regulatory changes, including the Inflation Reduction Act, clearly having an impact on the market. Maximum annual drug deductibles also increased steadily, with the highest absolute rise of $40 from $505 in 2023 to $545 in 2024.

After the highest average MOOP value recorded in 2021 ($5,622), there was a declining pattern for the next two consecutive years, while 2024 saw a minimal increase of $18, resulting in an average of $5,478.

The average trend of MOOP indicates that the Payors refuse to use MOOP as an acquisition tool, evident from the change that was relatively stable over the years, ranging from $5,400 to $5,600, while other cost factors saw increased variability. The maximum MOOP has risen consistently since 2020, with MOOP reaching $8,850 at the rate of ~7% YoY.

Also Read – Research Report: Diving Deeper – Analysing Medicare Advantage Plan Diversity in 2024

Segmentation of cost factors:

a. Premium

Of the total Non-SNP plans offered in 2024, the zero-premium segment accounts for about 67%, followed by the >$25 to <=$50 segment with 13%, covering the majority of the MA market. While the number of plans in the zero-premium segment has been consistently increasing, with the addition of a few hundred plans each year, 2024 saw a rise of only 36 plans, resulting in a total of 2,961. Contrastingly, there is a substantial drop of 35% YoY in new plans for the first time, totaling only 341, the lowest compared to any previous year, further supporting the conservative trend in the market.

After the zero-premium, the only other segment that saw an increase in 2024, surpassing a decline since 2022, is the >$25 to <=$50, with 13% YoY. This segment also saw a similar pattern in new plans, with the addition of only 19 plans into the market.

The >$0 to <=$25 premium segment noticed a slight growth last year while dipping to 298 total plans currently, while higher premium segments (>$50) have constantly declined over the years. With respect to new plans, the >$0 & <=$25 segment has the same number of plans as of 2023, while >$50 & <=$100 saw a decline of 64% YoY (from 22 to 8 plans) and over $100 segment has slightly increased from 8 to 12.

HMO and PPO Deep dive

The zero-premium segment, which has historically demonstrated a continuous ~5% YoY growth relative to total plans, increased to 71% of total HMO plans and 64% of total PPO plans, up only 0.7% and 1% YoY respectively. In the >$0 to <=$25 premium segment, the number of HMO plans has slightly gone up while PPO plan counts have decreased.

Additionally, the >$25 to <=$50 segment, which has seen recent reductions, will see an increase in the percentage of both HMO (11%) and PPO (15%) plans in 2024. On the other hand, the >$50 to <=$100 premium segment has seen a decrease in the percentage of HMO and PPO plans over time, which continues into next year. Conversely, the >$100 premium segment has witnessed a decrease to 4.9% in the proportion of HMO plans and an increase to 6.3% in PPO plans.

In 2024, all HMO premium segments, except for the >$25 to <=$50 segment, experienced a decrease in the number of total plans. Interestingly, the zero-premium segment (1,740) also saw a reduction of 51 plans for the first time in 2024 at 3% YoY.

The premium segments of >$0 to <=$25, >$25 to <=$50, and >$50 to <=$100 in PPO plans exhibit analogous trends to their counterparts in HMO plans. Specifically, the >$0 to <=$25 and >$50 to <=$100 segments demonstrate a decline, with 29 and 22 plans, respectively, while the >$25 to <=$50 segment shows a notable increase, with an additional 62 plans. However, it’s worth noting that in PPO plans, both the $0 and >$100 premium segments displayed an increase in plan count at 8% YoY and 9%, respectively, which contrasts with the corresponding segments in HMO plans.

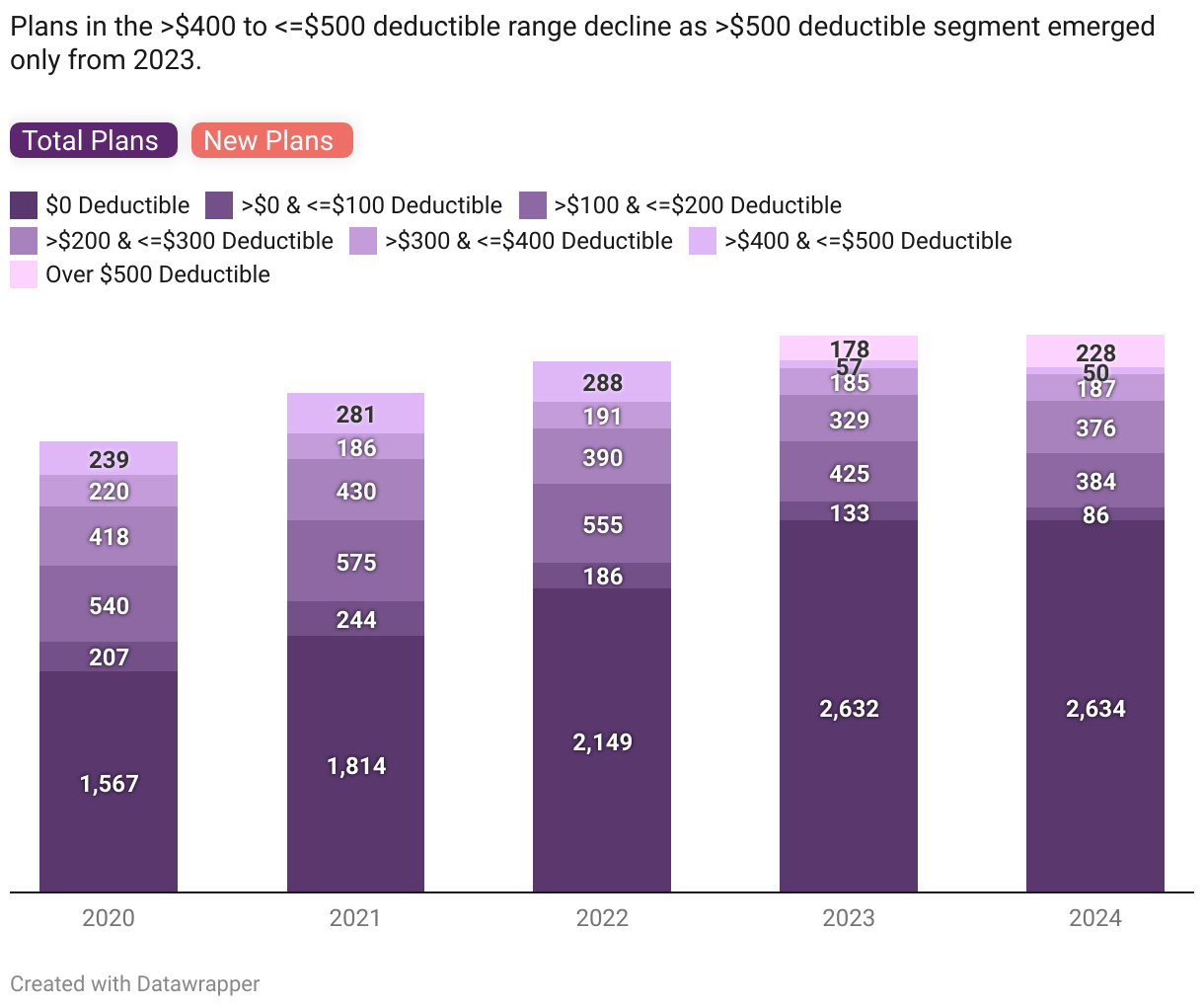

b. Drug deductible

The percentage of plans having a zero deductible is 67% of all plans and 61% of new plans, consistent with what we’ve seen in the previous year. The second largest segment is the mid-range deductibles (>$100 to <=$300), constituting 19% of total plans, while the >$200 & <=$300 deductible segment has ~16% of new plans. Moving up, the proportion of the higher deductible segment (>$500) accounts for 6% and 8% in total and new plans, respectively.

Only two plans were added to the zero deductible segment, which saw a decline in new plans by 29% YoY and a significant dip compared to any previous years. Plans with deductibles >$0 to <=$200, along with >$400 to <=$500 segments also noticed a decline.

There are fewer plans in >$0 & <=$100 (86 total and 5 new plans) and >$400 & <=$500 (50 total plans and 1 new plan) segments in comparison with others. Interestingly, the >$500 deductible segment, which was only initially offered starting in 2023, saw the highest net increase of 50 plans in total, experiencing 28% YoY growth, but declined in new plans by 25% YoY with only 36 added.

c. MOOP

In 2024, the distribution of plans across the >$3000 & <=$4500, >$4500 & =<$6000, and >$6000 MOOP segments was remarkably balanced, each approximately accounting for 29% of the total plans. The remaining 9% of plans fall within the >$1500 & <=$3000 segment, while 3% are in the $0 &<=$1500 segment.

All MOOP segments saw a slight increase in plan count except for the >$6000 segment, which experienced a 4% YoY decrease compared to the previous year. The new plans have a similar distribution across segments to the existing total plans. Every segment, apart from the $0 &<=$1500 segment, has seen a reduction in the number of new plans; notably, the >$6000 segment is experiencing a significant 41% YoY drop, followed by >$3000 & <=$4500 and >$4500 & =<$6000 segment which has a decline of new plan count by 42 and 41, respectively.

Conclusion:

As seen above, the cost factor trends for 2024 also align with our previous analysis, indicating a highly conservative year for Medicare Advantage Payors, focusing more on stability than market expansion.

The insights reveal the changing dynamics in premium costs, drug deductibles, and MOOP during the analyzed period, with fluctuations and occasional rebounds in certain years. The zero-premium segment continues to dominate the market offerings but experienced only a marginal increase in 2024, while drug deductibles have displayed an erratic trend at the national level. Meanwhile, MOOP values have remained relatively stable, except for the >$6000 segment, which has witnessed a noticeable decline.

Stay tuned for more 2024 AEP Insights from HealthWorksAI!

Read More about AEP Insights

-

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research -

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research -

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research -

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research -

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research