2024 Post AEP Insight Series: Report 2 📊

Exploring Payor Leadership and State Dynamics in the Medicare Advantage Landscape

March 21, 2024 Market Research

Table of Contents

Understanding the dynamics of payor leadership and state-level trends is paramount for stakeholders to learn about the present situation in the Medicare Advantage (MA) market. This comprehensive analysis delves into the forefront of the MA market, shedding light on the key payors, their membership, the state-based dynamics, and the penetration rate that is shaping the industry. From examining enrollment figures to dissecting net enrollment contributions, this exploration aims to provide insights into the evolving landscape of MA market leadership. In this article, we have focused exclusively on Individual Non-SNP plans by utilizing the data sets like Landscape, Crosswalk, and Enrollment files released by CMS.

For state-level enrollment, net enrollment, and net contribution percentages, please refer to Article 1 for detailed information. Let’s explore the enrollment and net enrollment details at the payor level.

Who is leading the market?

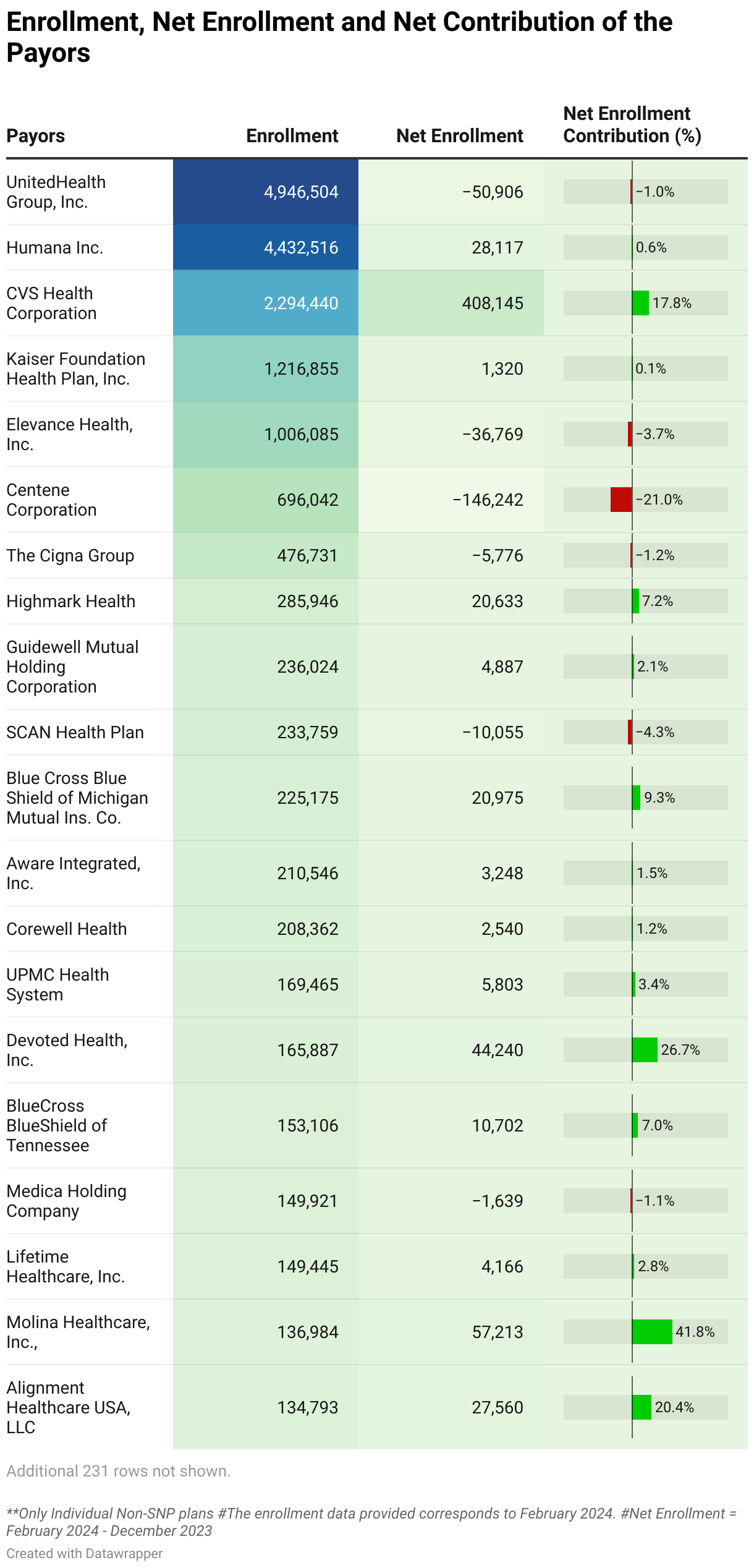

The highest enrollment was observed in the United Health Group, with approximately 4.95 million enrollees registered in their Individual Non-SNP plans. However, despite the high enrollment numbers, the net enrollment showed a loss. Following United Health Group, Humana captured a significant 21% market share. Meanwhile, CVS Health Corporation experienced a remarkable 23% year-over-year (YoY) growth in the membership. Together, these three primary players, along with Kaiser Foundation Health Plan and Elevance Health, accounted for approximately 66% of the Individual Non-SNP enrollments, highlighting their dominance in the market.

In terms of absolute net enrollment, CVS Health Corporation takes the lead, showcasing substantial growth this year and contributing 17.8% of the net gain. Following closely behind are Molina Healthcare and Devoted Health, with net gains in membership of 57K and 44K, respectively. Conversely, Centene Corporation experienced the highest loss in net enrollment.

Payors leading in State based on membership:

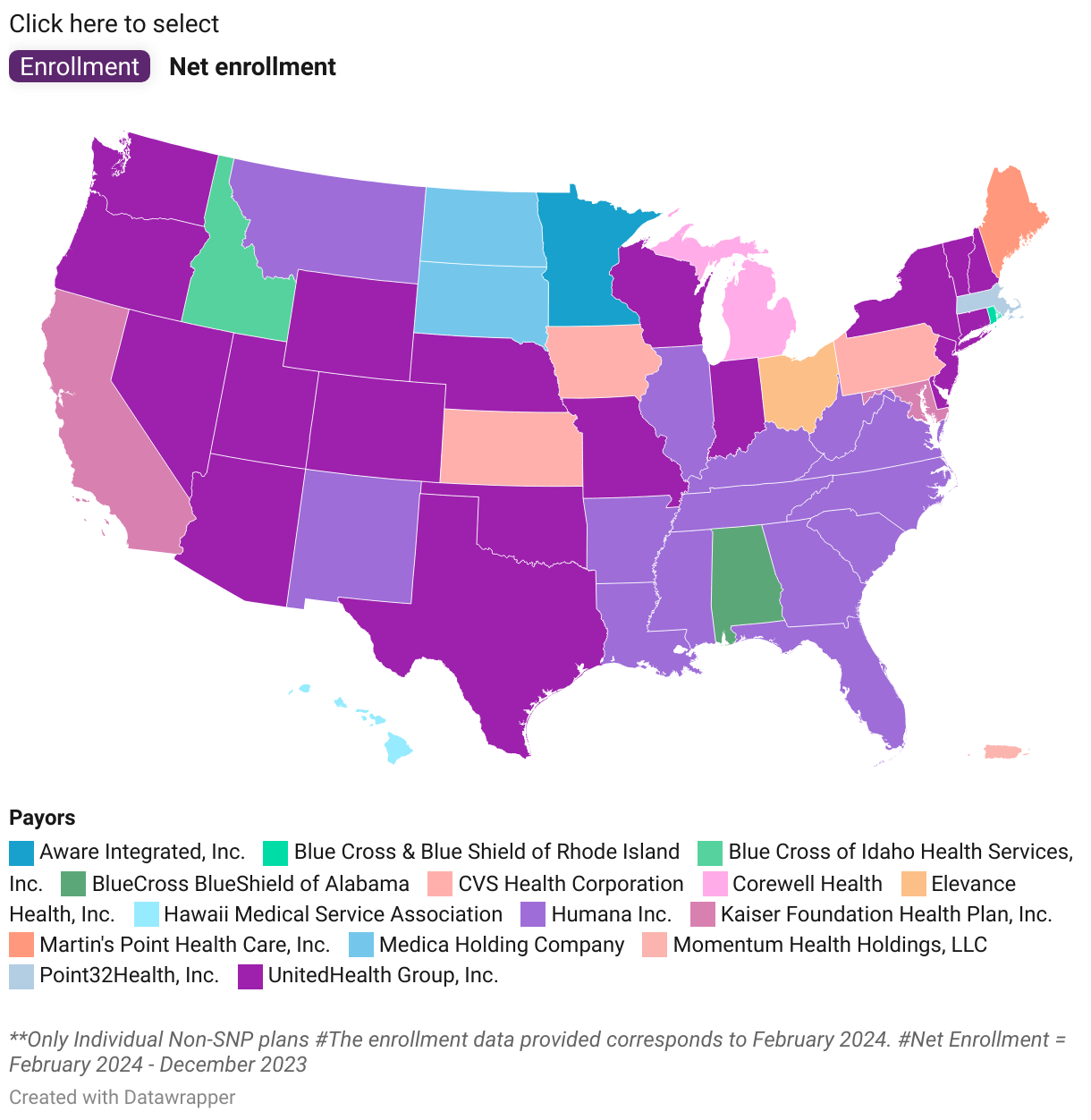

In this section, we will explore the states where Payors have the highest enrollment and net enrollment values. National Payors such as United Health Group and Humana are prominent leaders in enrollment in many states, with United Health Group leading in 19 states and Humana in 14. CVS Health Corporation emerges as the top player in States like Iowa, Kansas, and Pennsylvania. Notably, California stands out as the leading State in the MA market, with Kaiser Foundation Health Plan contributing approximately 40% of the total enrollment in the State.

Interestingly, the landscape shifts when considering the net enrollment value. CVS Health Corporation emerges as the dominant payor, covering 55% of states in the US. Specifically, CVS has experienced a net gain and ranks as the top payor in 28 states in 2024. Humana, Elevance Health, and Blue Cross Blue Shield of Michigan Mutual Corporation each lead in three states. Additionally, United Health Group leads in Oklahoma and Wyoming, while Devoted Health leads in Colorado and Hawaii. Notably, among the leading payors, Molina Healthcare has the highest net enrollment in California.

Relationship between eligibles and enrollment across the states:

If we consider that there is a linear relationship between eligibility and enrollment, it holds true in certain instances, such as California, Florida, and Texas, where high eligibility corresponds to high enrollment figures. However, this linear relationship does not apply universally across all states.

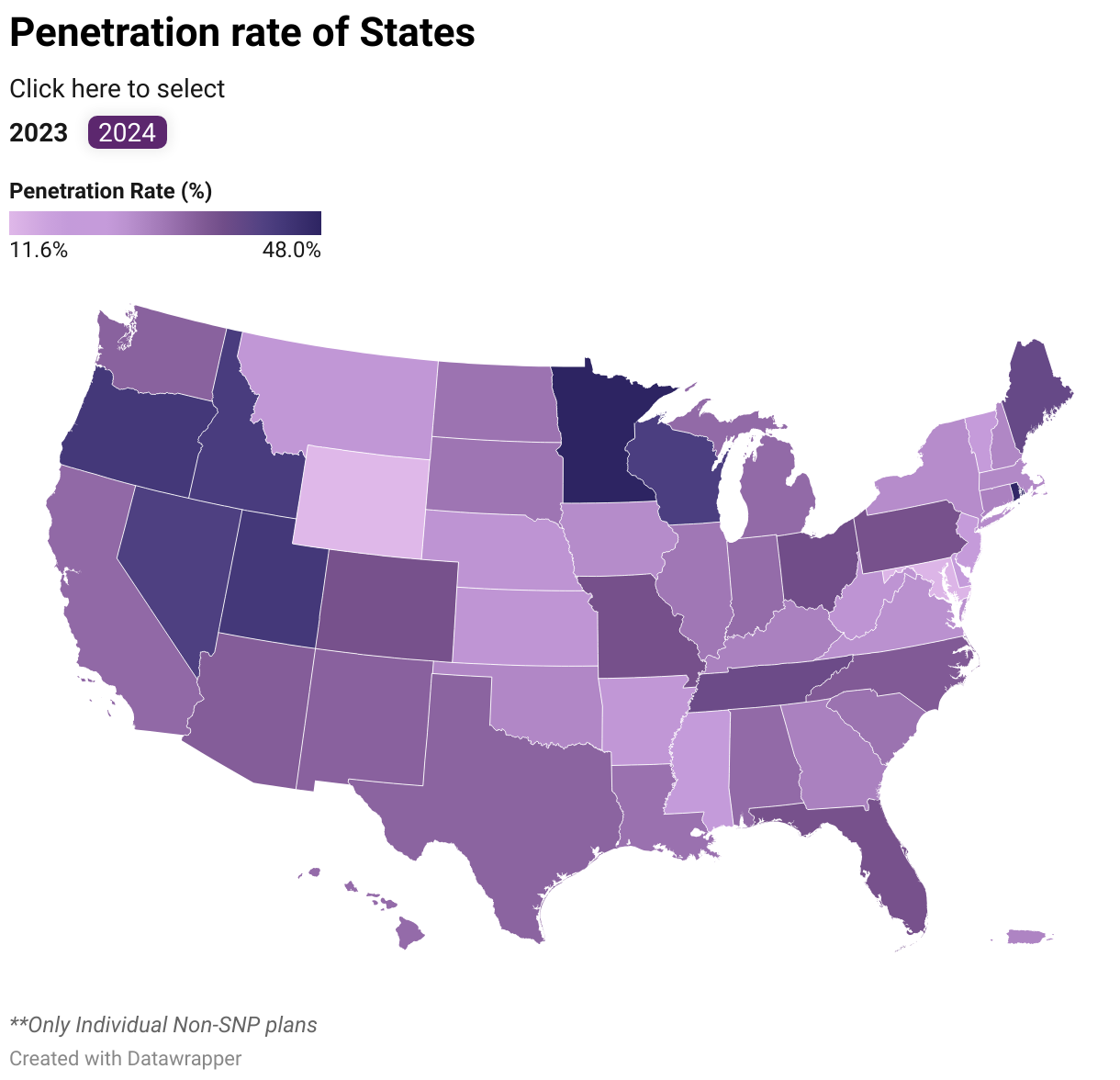

At the national level, the penetration rate for Individual Non-SNP plans has increased marginally from 31% to 31.6% in 2024. Currently, Minnesota has the highest penetration rate, standing at approximately 48%. Interestingly, Rhode Island held the top position in 2023 with a penetration rate of 46.5%, but in 2024, it secured the second-highest position with 47.3%. Conversely, Wyoming exhibits the lowest penetration rate at around 11.6%; however, it experienced the highest increase in penetration compared to the previous year, jumping from 7.9%. On average, the penetration rate of the top five states with the highest number of eligibles and enrollment is approximately 32.3%.

To learn more about these findings and to dig deeper into your local market, please reach out to the HealthWorksAI team. We can show you how to gain easy access to market and competitor data to help plan your growth strategies.

Conclusion:

As the Medicare Advantage landscape continues to evolve, the insights gleaned from this analysis offer valuable guidance for stakeholders navigating the complexities of the market. By understanding the leading payors, their enrollment strategies, and the state-level dynamics, stakeholders can adapt their approaches to better serve beneficiaries and thrive in the ever-changing MA landscape. As we look towards the future of Medicare Advantage, these insights serve as a compass, guiding stakeholders towards informed decisions and strategic initiatives for success.

Defining terms:

** Net Enrollment is the difference between enrollment from February 2024 to December 2023.

** The net enrollment contribution is determined by dividing the net enrollment from February 2024 to December 2023 by the total net enrollment. It is represented as a percentage.

** The penetration rate is the percentage that divides the total enrollment by the total number of eligibles.

Read More about Post AEP Insights

Read More about AEP Insights

-

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research -

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research -

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research -

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research -

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research -

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research