2024 Post AEP Insight Series: Report 1 📊

🔄Shifting Landscape in MA: Growth & Market Saturation Trends Revealed!

Prepping Your 2025 Medicare Advantage Bid? Don't Miss These 2024 Trends!

March 19, 2024 Market Research

Table of Contents

The Medicare Advantage (MA) market witnessed nuanced shifts in February 2024, with the overall membership reaching 33 million, up from 31 million, encapsulating both Group and Individual categories. This period saw the introduction of the fewest “new” plans in recent years, highlighting a trend towards market consolidation and selective growth. This article provides a detailed examination of the evolving landscape in the MA ecosystem, highlighting the present status and identifying emerging trends shaping its future through enrollment and plan breakdown insights. By utilizing an array of data sources, including landscape, crosswalk, and enrollment files released by the Centers for Medicare & Medicaid Services (CMS), we aim to uncover the underlying factors driving these changes.

National Overview:

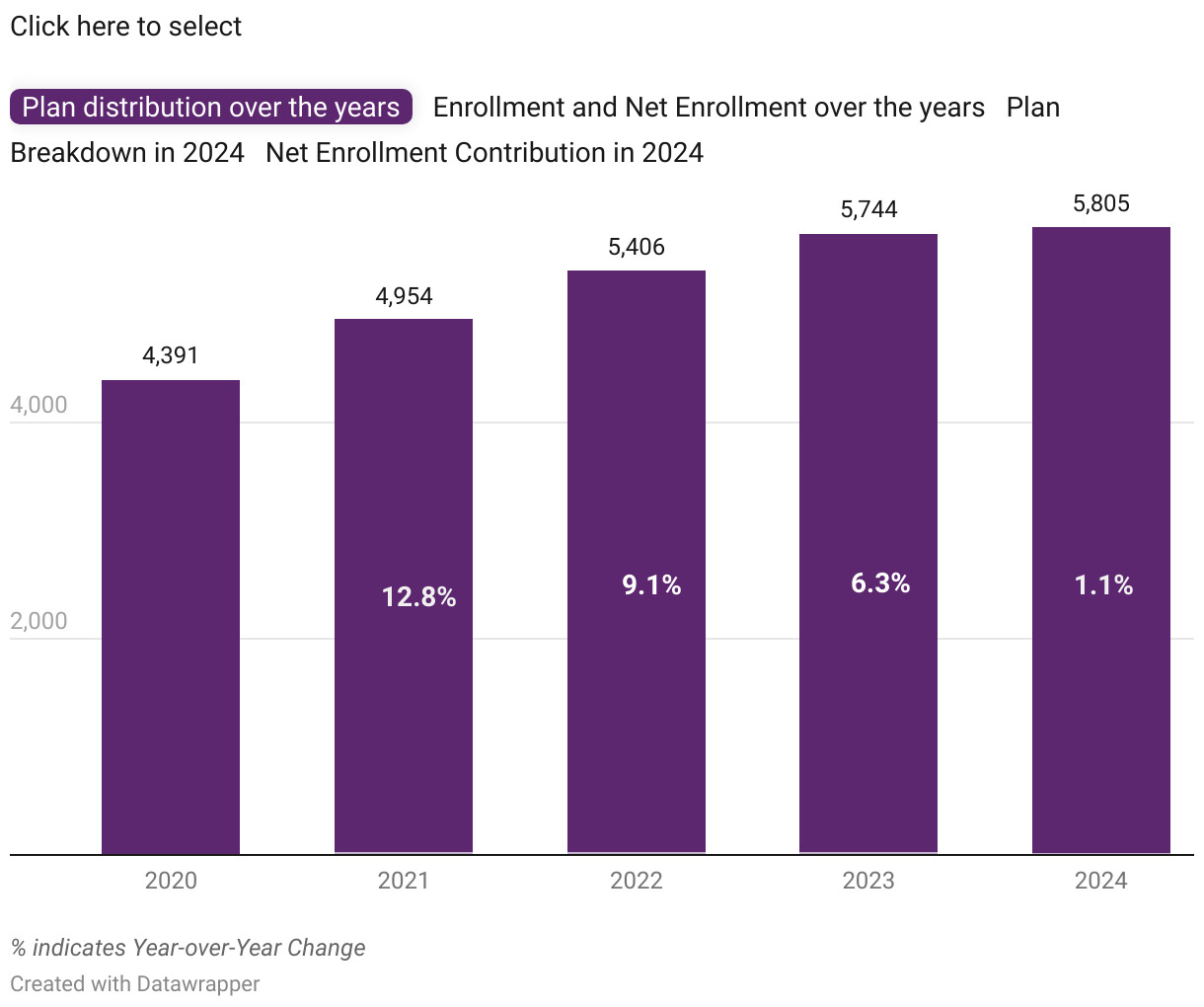

Only 61 plans have been added to the MA market currently, marking the lowest inclusion of plans seen in any prior years. This accounts for a total of 5,805 plans, reflecting a modest growth of 1.1% year-over-year (YoY).

By February 2024, the market had seen a steady annual growth rate of 7.3%, reaching a total membership of 27.5 million individuals. Nevertheless, the net enrollment trend has decreased since 2022, marking the third consecutive decline with 0.72 million in 2024. Group plans exhibited growth at the rate of 5.4% YoY increase with 5.7 million enrollees, and the net enrollment saw a slight increase from 258K to 267K.

The plan breakdown observed a slight increase compared to 2023 in Renewal Plans, Consolidated Plans, and Renewal Plans with Service Area Reduction (SAR) reaching 65.3%, 5.4%, and 3.7% respectively, however, the absolute net enrollment contribution is seen to be at a loss.

Unsurprisingly, the combination of New Plans and Initial Contracts accounted for 714 plans, down from 881, contributing approximately 12.3% of the total. Notably, New Plans alone contributed a higher net enrollment, reaching around 64%, exceeding levels seen in previous years. Apart from New Plans, all the remaining plan categories noticed a decrease in the share of membership in comparison with 2023, majorly in Renewal Plans with SAE from 404K to 314K enrollees, and Initial Contracts dropped from around 6% to less than a percent explaining the stagnation of market.

There are fluctuations in net enrollment numbers across different plan categories over the years. However, Renewal Plans experienced significant variations in terms of enrollment, with a substantial decline in the previous year and noticed a rise in 2024, similarly, Renewal Plans with Service Area Expansion (SAE) peaked in 2021 but declined thereafter, and Consolidated Renewal Plans are dropped in 2024. Conversely, New Plans exhibited a more stable trend, with enrollments fluctuating but showing a moderate increase overall. These fluctuations in membership numbers underscore the dynamic nature of the healthcare market, influenced by factors such as plan offerings, consumer preferences, and regulatory changes.

Individual Plans:

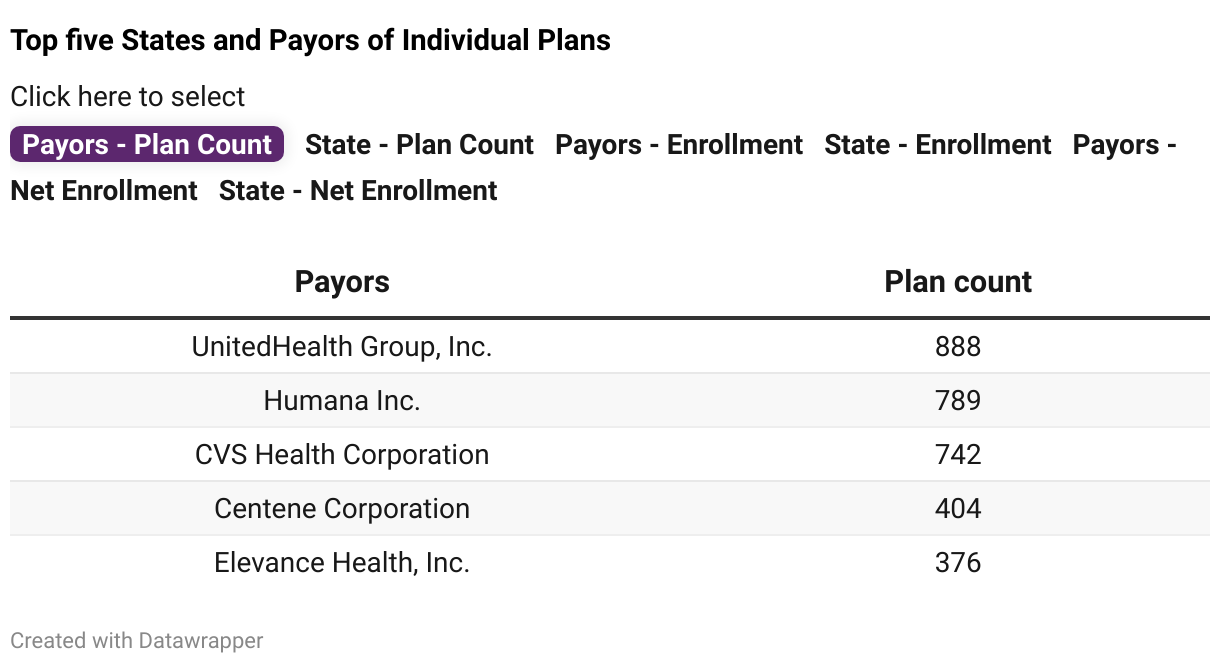

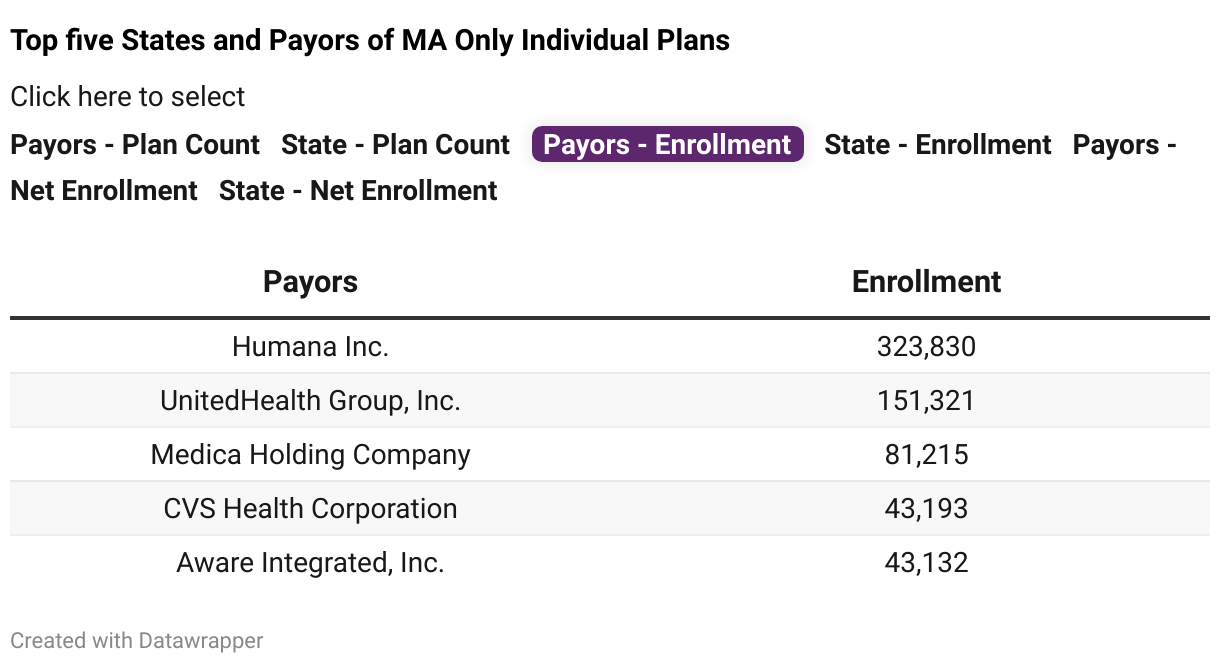

While the top five states boast the highest enrollment numbers, their net contribution percentages range from a modest two percent to no more than five percent. Interestingly, Kaiser Foundation Health Plan offers approximately 86, fewer than the top five payors, yet its enrollment ranks fifth among other payors. Wyoming steals the spotlight with the highest net enrollment contribution, injecting an intriguing element into the distribution of contributions across states. Moreover, it’s worth noting that smaller payors, with enrollments of less than 25,000, demonstrate higher contributions. However, among national payors, Devoted Health stands out this year, boasting a remarkable 30% gain in contribution. Though UnitedHealth Group tops the enrollment table, the net enrollment from February 2024 to December 2023 has fallen.

Group plans:

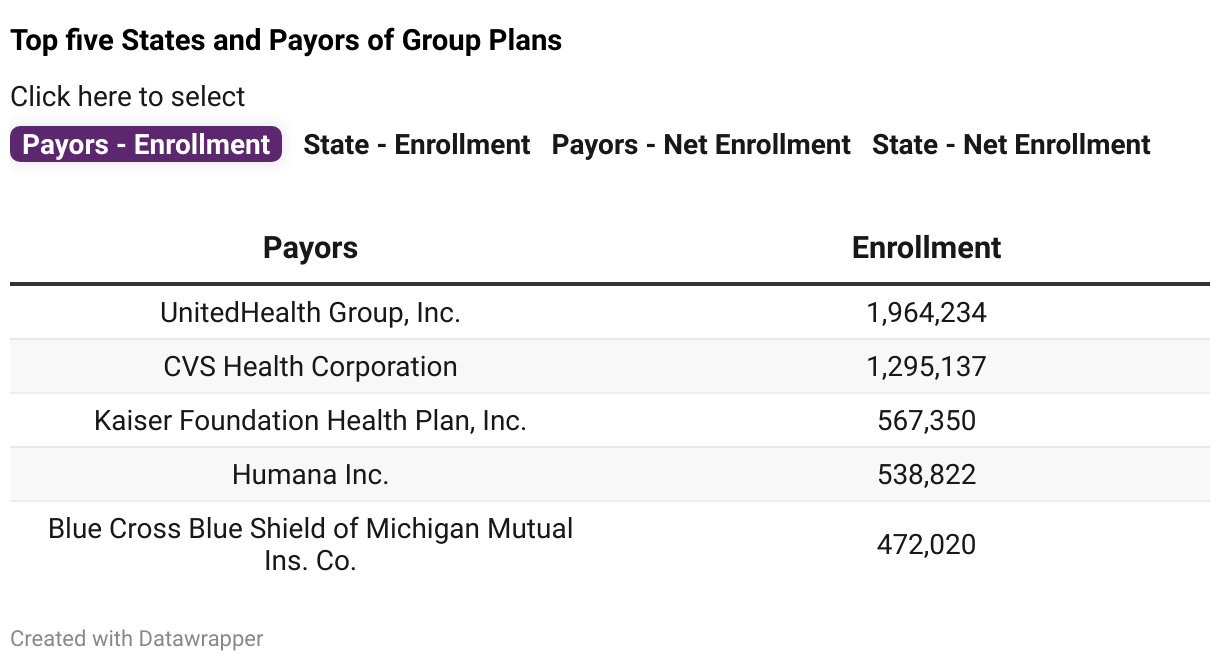

The highest net contribution was seen in Health Care Service Corporation (HCSC), followed by Cigna Group with 20.5%. Unlike in Individual plans, the net enrollment of UnitedHealth Group and Humana has grown with net gain percentages of 6.1% and 7.8%, respectively.

MA/MAPD Overview

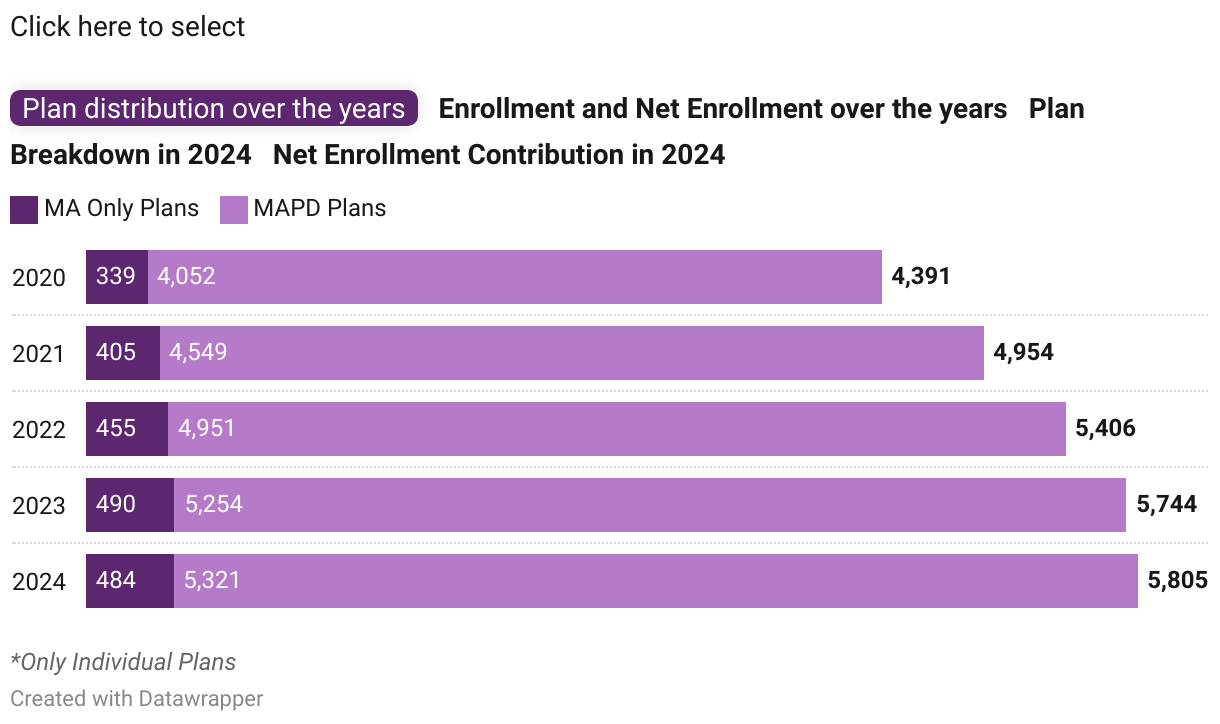

For the first time, MA Only plans have declined in 2024 by six plans, while the MAPD plans saw a minimal rise of only 1.3% YoY, consisting of 5,321 plans in total. New Plans and Initial Contracts collectively account for 7.9% in the MA Only category, whereas in the MAPD category, they represent 12.7% of all plans. The highest plan share is observed in Renewal Plans comprising around 65% in both MA Only and MAPD plans.

Of total individual enrollment, about 97% is from MAPD plans have increased from 24.9 million to 26.7 million, while the MA Only plans have reached 815K enrollees at the rate of 6.3% YoY growth. The sharp declines in the percentage growth of net membership for MA Only in 2024 (-61.50%) and a decrease in MAPD growth (-10.30%) might indicate market saturation.

The net gain in MAPD plans predominantly stems from New Plans (63.4%) and Renewal Plans with SAE (20%), accounting for a substantial portion of 83.4%. Similarly, in the MA Only category, SAE Renewal plans (41.5%) have higher share, with both SAE Renewal and New Plan categories together contributing to 70.4% of the growth.

Apart from New Plans, the other plan categories experienced either a decline or minimal growth in net enrollment compared to the previous year. On the contrary, MA Only plans witnessed a decrease in net membership gain from new plans and an increase in enrollment change across all renewal plans except for Consolidated Renewal Plans.

MA Individual Plans:

MAPD Individual Plans:

State Overview:

A well-known fact is that California, Florida, Texas, New York, and Pennsylvania consistently rank among the top five states in terms of enrollments in the Medicare Advantage market over the years, contributing to approximately 38% together out of total individual enrollments.

From December 2023 to February 2024, Florida experienced the highest membership growth of 48K individuals, surpassing Texas, which led to enrollment growth in 2023 with 74K individuals. North Carolina, which had a net enrollment decrease of -881 in the previous year, notably added 40K+ enrollees during this period, securing its position among the top five states with the highest net gain in membership.

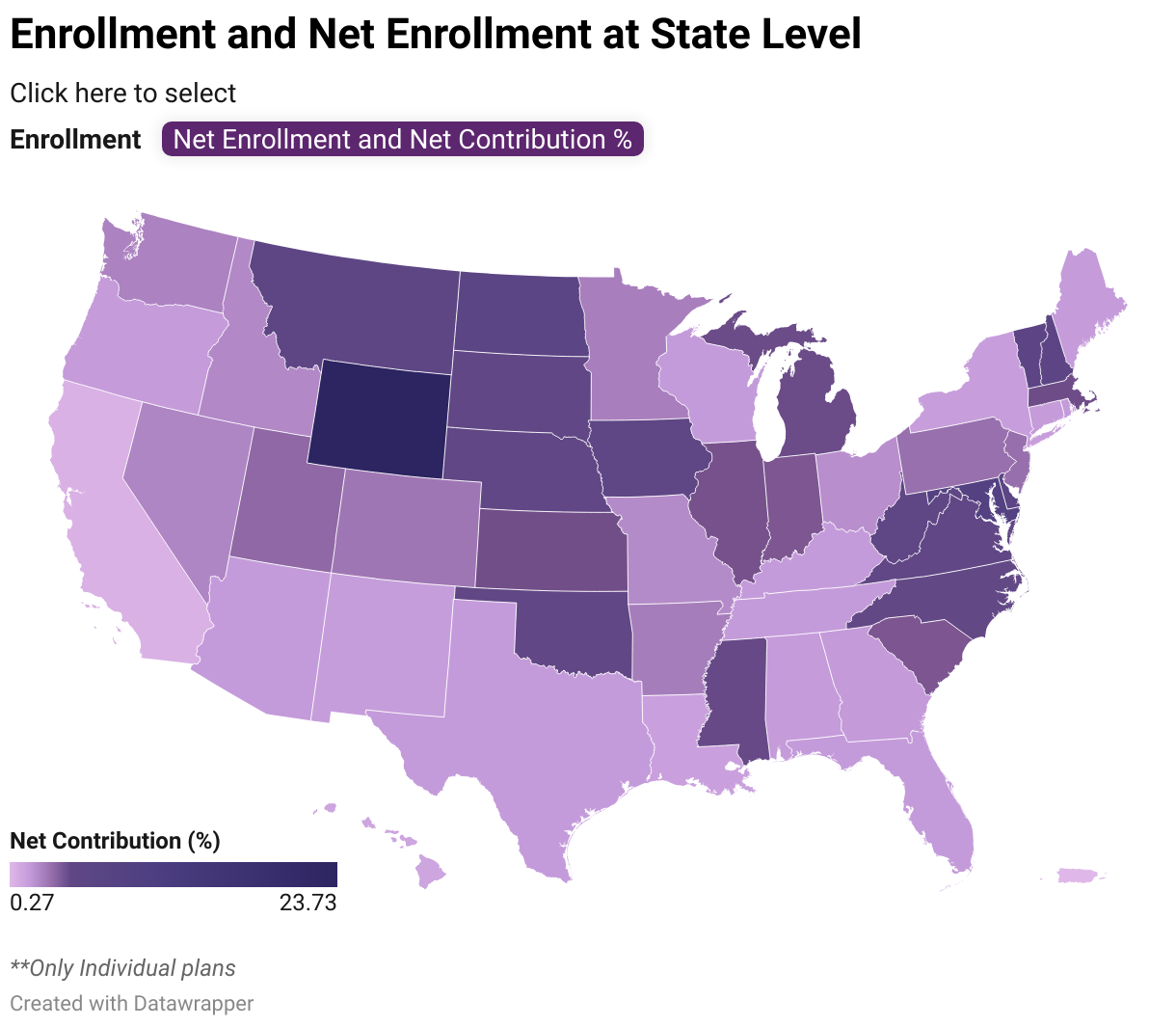

While Wyoming boasts the lowest current enrollment figures among states, it experienced the most substantial percentage of enrollment growth from December 2023 to February 2024, accounting for approximately 24%, followed by Maryland at around 9% and Delaware at about 6%. Conversely, states like Texas, Florida, and California, with enrollee numbers ranging from 2 to 2.6 million, exhibited lower net enrollment contributions in 2024, with figures of 2.1%, 1.9%, and 0.6%, respectively, depicting that higher enrollment figures corresponded to lower net contributions in these regions.

Aside from Florida, California, and Texas, which consistently rank among the top states for newly introduced plans, Indiana and Virginia emerge as notable competitors, securing the third and fourth positions, respectively. Indiana has 53K enrollees, while Virginia followed closely with 40K enrollees, solidifying their places in the top five for plan enrollment.

Conclusion:

In conclusion, the 2024 Medicare Advantage market reflects a complex interplay of factors, driving both growth and consolidation within the industry. While the overall enrollment continues to rise, the addition of new plans remains subdued, signaling a shift towards a more focused approach to expansion. Despite challenges such as market saturation and fluctuating enrollment trends, states like Florida, Texas, and California maintain their prominence while other states carve out their place in the top ranks. As the healthcare landscape continues to evolve, understanding these trends is essential for stakeholders to adapt and thrive in an ever-changing market environment.

Defining terms:

** Net Enrollment is the difference between enrollment from February 2024 to December 2023.

** The absolute net enrollment contribution percentage (or net enrollment contribution) is determined by dividing the absolute net enrollment from February 2024 to December 2023 by the total absolute net enrollment across all plan descriptions, encompassing New Plans, Initial Contracts, Renewal Plans, Consolidated Renewal Plans, Renewal Plans with SAE (Service Area Expansion), and Renewal Plans with SAR (Service Area Reduction).

** New Plans, Initial Contracts – new plans.

** Renewal Plans, Consolidated Renewal Plans, Renewal Plans with SAE, and Renewal Plans with SAR – renewal plans.

Coming Soon: Wait to dive into next article - “Who is the leader in MA market?” along with glimpses of State penetration rates.

Read More about Post AEP Insights

Read More about AEP Insights

-

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research

Research Report: Decoding the 2024 Medicare Advantage Landscape04 Oct 2023 Market Research -

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research

Research Report: Diving Deeper - Analysing Medicare Advantage Plan Diversity in 202406 Oct 2023 Market Research -

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research

Research Report: Medicare Advantage in 2024 - A Look at Premiums, Deductibles, and MOOP Offerings13 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of the Non-SNP Market19 Oct 2023 Market Research -

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research

Supplemental and Enhanced Benefits Medicare Advantage Plans: Trends and Transformations of Dual-Eligible Special Needs Plans25 Oct 2023 Market Research -

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research

Medicare Advantage Premium Tiers: Impact on Supplemental and Enhanced Benefits03 Nov 2023 Market Research -

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research

Analyzing SSBCI Trends: A Comprehensive Analysis of Medicare Advantage Plans16 Nov 2023 Market Research -

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research

Navigating the (MA) Stars: Trends of the 2024 Ratings30 Nov 2023 Market Research